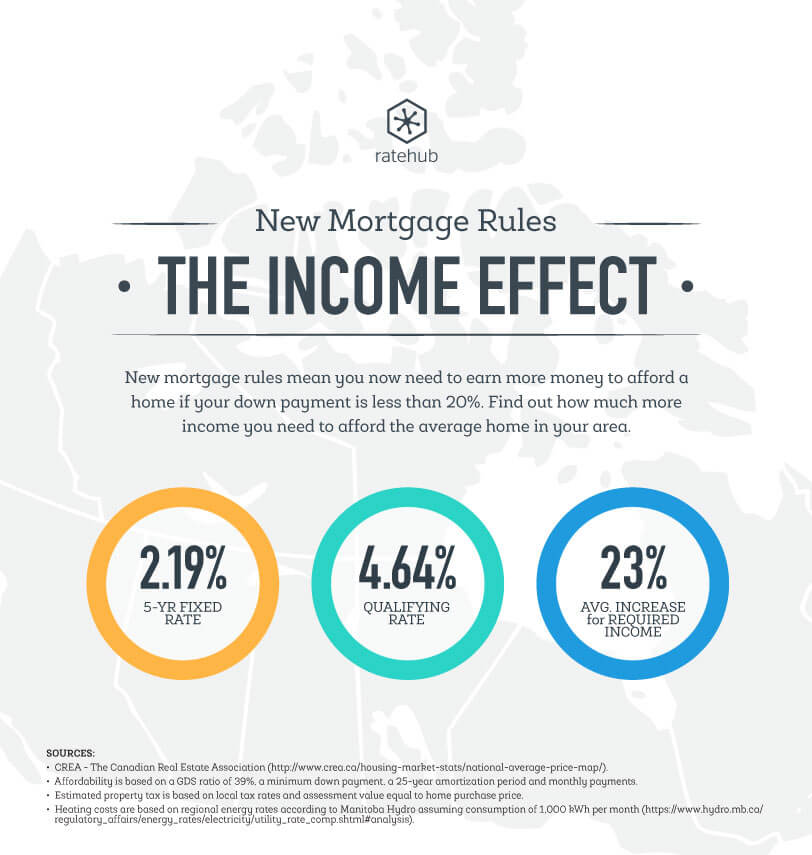

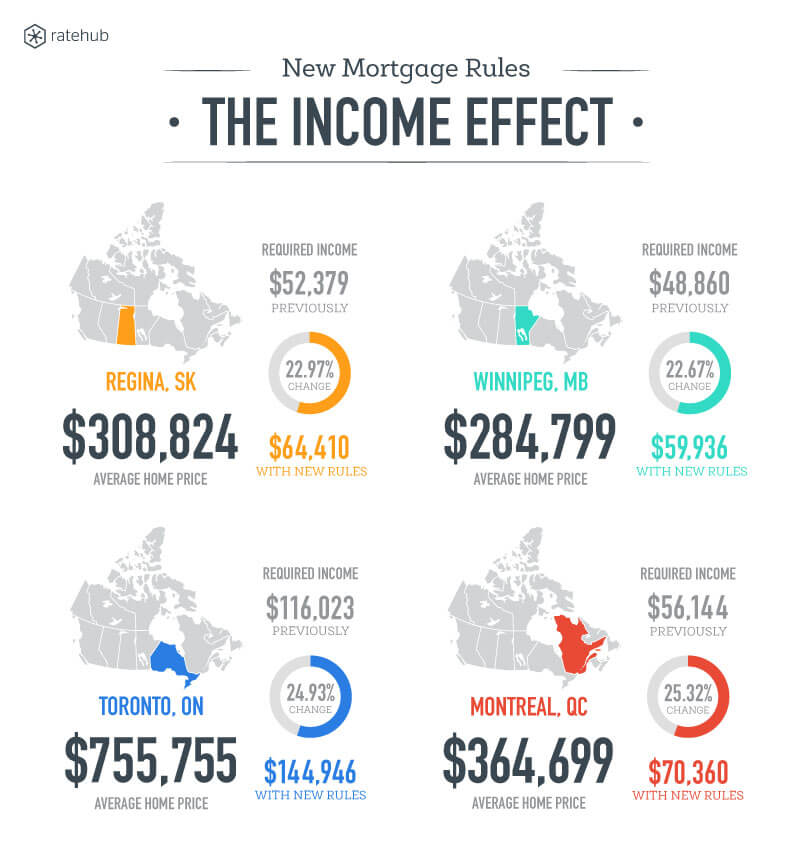

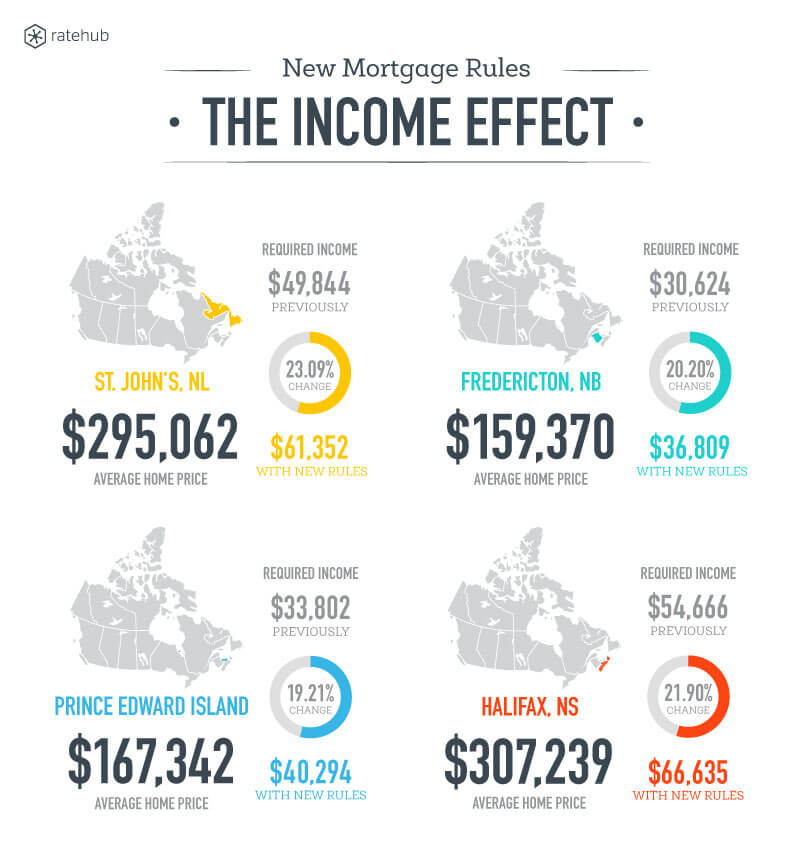

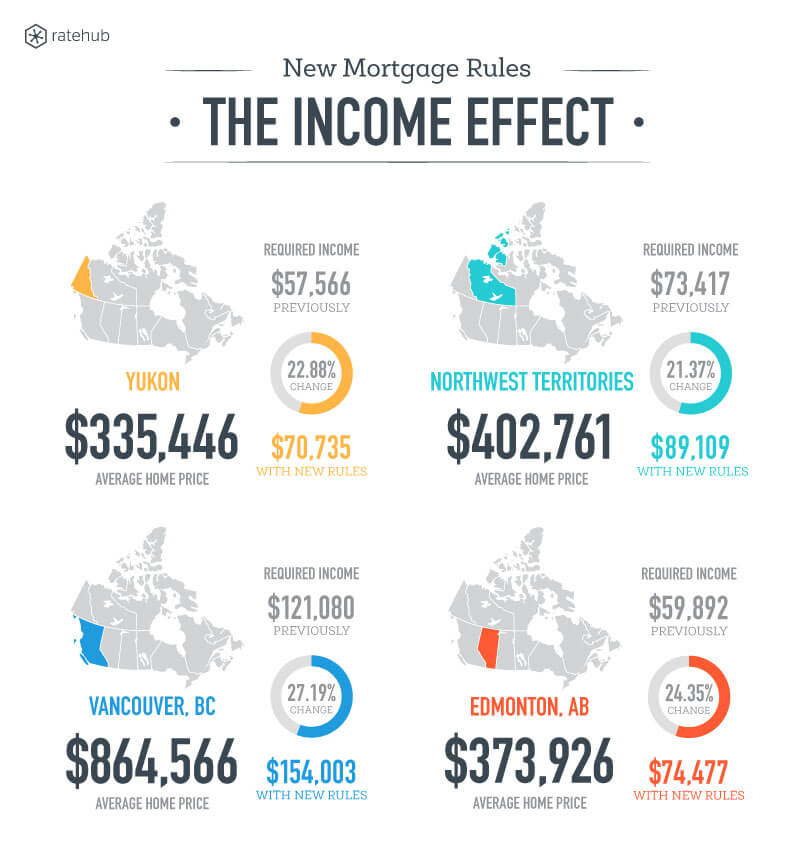

How much more you need to afford a home now

People in Vancouver need to a 27% higher income after new mortgage rules

Advertisement

People in Vancouver need to a 27% higher income after new mortgage rules

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Learn what condo fees pay for, why they rise over time, and how to assess a building's financial health...

If your landlord defaults and the home is sold, your tenancy may still be protected—but rules vary by province....

Thinking of selling your home without a Realtor? Here’s what DIY sellers need to know about commissions, legal risks,...

Short-term rentals can help cover housing costs, but experts say many first-time hosts underestimate the legal, financial, and lifestyle...

As falling home prices leave more Canadians underwater on their mortgages, experts explain the refinancing and renewal options available.

Buying a home can change your life insurance needs fast. Here’s how much coverage young Canadians may actually need—and...

Bank of Canada holds its 2.25% rate for a fourth time amid inflation risks from oil prices, affecting mortgages,...