Am I on track to buy a home in five years?

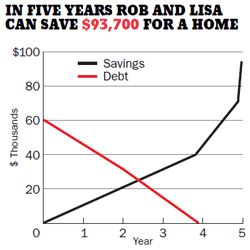

If Rob and Lisa can make their home ownership dreams come true, but it will mean they'll have to start aggressively paying down their debt.

Advertisement

If Rob and Lisa can make their home ownership dreams come true, but it will mean they'll have to start aggressively paying down their debt.

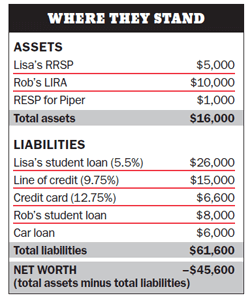

Rob Hamilton, 37, and Lisa Aldworth, 33, rent a two-bedroom apartment in Toronto with their one-year-old daughter, Piper. They would like to own a home, but they are $61,600 in debt. “We think saving for a down payment and buying our house in five years is a more realistic strategy,” says Lisa. They would love to stay in the city, but are also considering Guelph, Ont., since it is more affordable and closer to Lisa’s parents.

Rob Hamilton, 37, and Lisa Aldworth, 33, rent a two-bedroom apartment in Toronto with their one-year-old daughter, Piper. They would like to own a home, but they are $61,600 in debt. “We think saving for a down payment and buying our house in five years is a more realistic strategy,” says Lisa. They would love to stay in the city, but are also considering Guelph, Ont., since it is more affordable and closer to Lisa’s parents.

Each year this couple spends $9,600 on debt repayment, $5,000 for transportation, $18,000 for Piper’s daycare, and $11,820 for rent—a steal in Toronto. With incidentals their expenses hit $53,920. Rob makes $35,000 working for an arts organization while Lisa earns $74,000 as a social worker, giving them a combined after tax income of just $82,328. That leaves them with $28,408 annually to pay down debt and save for their house. “Should we contribute to RRSPs or stick to Tax-Free Savings Accounts?” asks Lisa. “My parents want to give us a $20,000 gift when we’re ready to buy. That will help. Are we on track?”

Each year this couple spends $9,600 on debt repayment, $5,000 for transportation, $18,000 for Piper’s daycare, and $11,820 for rent—a steal in Toronto. With incidentals their expenses hit $53,920. Rob makes $35,000 working for an arts organization while Lisa earns $74,000 as a social worker, giving them a combined after tax income of just $82,328. That leaves them with $28,408 annually to pay down debt and save for their house. “Should we contribute to RRSPs or stick to Tax-Free Savings Accounts?” asks Lisa. “My parents want to give us a $20,000 gift when we’re ready to buy. That will help. Are we on track?”

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The co-founder of online prenuptial agreement startup Jointly talks about leaving Big Law, tracking spending as a system, and...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

Canadian investors have several options for investing in bitcoin and other cryptocurrencies. Here are the pros and cons of...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Many retailers offer buy now, pay later programs to encourage spending. Understand the risks, including how your BNPL data...

These top 10 Canadian momentum stocks all returned more than 40% over the past three months.