Going global with low-cost ETFs

Patrick and Lisa Bourbonnais are engineers near Moncton, N.B. Their defined contribution pensions are at the same employer. They also invest in ETFs at an online brokerage but want to diversify beyond Canada. Here's what we came up with.

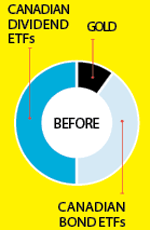

Patrick, 38, and Lisa, 37, moved their RRSPs out of a large investment firm to switch to ETFs. They don’t consider themselves aggressive investors. With sons Philip and Jeremy still in grade school, they aren’t expecting to retire for at least 20 years. “I question whether our asset allocation is optimized,” Patrick says. Half the portfolio is in two iShares dividend ETFs (TSX-listed CDZ and XDV), 40% is in two iShares bond ETFs, and the rest is in the iShares Gold Bullion Fund (CGL). They want to cut costs and add exposure to U.S. and international equity income, but aren’t sure how to do it. “My head is starting to spin,” says Patrick.

Patrick, 38, and Lisa, 37, moved their RRSPs out of a large investment firm to switch to ETFs. They don’t consider themselves aggressive investors. With sons Philip and Jeremy still in grade school, they aren’t expecting to retire for at least 20 years. “I question whether our asset allocation is optimized,” Patrick says. Half the portfolio is in two iShares dividend ETFs (TSX-listed CDZ and XDV), 40% is in two iShares bond ETFs, and the rest is in the iShares Gold Bullion Fund (CGL). They want to cut costs and add exposure to U.S. and international equity income, but aren’t sure how to do it. “My head is starting to spin,” says Patrick.

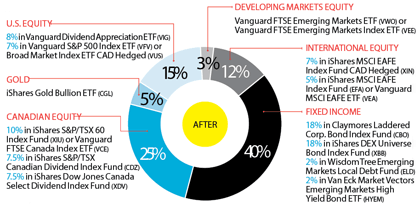

The existing 40% bond exposure is about right but Brian Smith, portfolio manager with Fit Private Investment Counsel, recommends lowering Canadian equity exposure to 25% and halving the gold play to make room for 30% international content. Fit provides discretionary investment counsel only in Ontario and B.C. and most client equity portfolios are tilted to higher dividends, Smith says. “Asset allocation targets can be achieved by utilizing new contributions. As the portfolio grows there will be sufficient assets to include more asset classes and specialization.” Smith actively manages asset mix and tactical components as market conditions change but “for investors attempting to go it alone, it makes more sense to stick to the basic building blocks.” Their pensions already hold some global mutual funds and Lisa says she’s comfortable branching out globally. “There’s high risk everywhere. You can’t hide from it.” As their global exposure grows, some ETFs should be hedged back into the loonie. It’s normal to leave the first 20% or 30% of foreign exposure unhedged, but after that Canadian dollar-hedged ETFs should be used, Smith says. Lisa and Patrick are still under 25% foreign exposure, even in the rejigged portfolio. “Cost isn’t everything,” Smith says. “Most important is to build the portfolio. Be conscious of cost but it’s not the only driver.” Apart from Vanguard, most major ETF companies have at least some low-cost offerings, including BMO ETFs and Horizons BetaPro, he says.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to

The existing 40% bond exposure is about right but Brian Smith, portfolio manager with Fit Private Investment Counsel, recommends lowering Canadian equity exposure to 25% and halving the gold play to make room for 30% international content. Fit provides discretionary investment counsel only in Ontario and B.C. and most client equity portfolios are tilted to higher dividends, Smith says. “Asset allocation targets can be achieved by utilizing new contributions. As the portfolio grows there will be sufficient assets to include more asset classes and specialization.” Smith actively manages asset mix and tactical components as market conditions change but “for investors attempting to go it alone, it makes more sense to stick to the basic building blocks.” Their pensions already hold some global mutual funds and Lisa says she’s comfortable branching out globally. “There’s high risk everywhere. You can’t hide from it.” As their global exposure grows, some ETFs should be hedged back into the loonie. It’s normal to leave the first 20% or 30% of foreign exposure unhedged, but after that Canadian dollar-hedged ETFs should be used, Smith says. Lisa and Patrick are still under 25% foreign exposure, even in the rejigged portfolio. “Cost isn’t everything,” Smith says. “Most important is to build the portfolio. Be conscious of cost but it’s not the only driver.” Apart from Vanguard, most major ETF companies have at least some low-cost offerings, including BMO ETFs and Horizons BetaPro, he says.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to