Poorer than ever

Incomes for young Canadians are falling, even while incomes for retirees soar. What’s going on?

Advertisement

Incomes for young Canadians are falling, even while incomes for retirees soar. What’s going on?

Muhammad Ali Jabbar considers himself one of the lucky ones. When he graduated with a degree in mechanical engineering from Toronto’s Ryerson University last year, the 25-year-old Milton, Ont., resident already had a decent-paying job lined up in his field. But even so, he finds himself struggling to pay his mortgage, his $30,000 student loan and $15,000 line of credit. “Basically all the money I make goes to paying bills,” he says. “I wasn’t able to make my payments last month and I got a call from a collection agency. It’s discouraging.”

Muhammad Ali Jabbar considers himself one of the lucky ones. When he graduated with a degree in mechanical engineering from Toronto’s Ryerson University last year, the 25-year-old Milton, Ont., resident already had a decent-paying job lined up in his field. But even so, he finds himself struggling to pay his mortgage, his $30,000 student loan and $15,000 line of credit. “Basically all the money I make goes to paying bills,” he says. “I wasn’t able to make my payments last month and I got a call from a collection agency. It’s discouraging.”Jabbar lived with his parents while he was at university, and held down various jobs to pay for it—he worked at a gas station, he was in the Canadian Forces reserves, and he was the student union president. But he never made enough to cover his $6,200 tuition. Now he’s weighed down by such a large debt that he and his wife have decided to hold off on having kids, as he’s worried about “having more people to feed.”

Many other young families are finding themselves in a similar bind—and the recent recession has shouldered most of the blame. But is this really just a short-term blip that will evaporate over the next few years? Or is there a deeper problem here? To find out, MoneySense commissioned researcher Roger Sauvé to dig through piles of Statistics Canada data to find out how the incomes for different age groups have changed over the 30-year period between 1978 and 2008. He discovered that the high unemployment and low wages that young Canadians ran into during the recession were just the latest in a long string of losses. Even before the recession hit, young Canadians had been losing income and wealth to older generations for years.

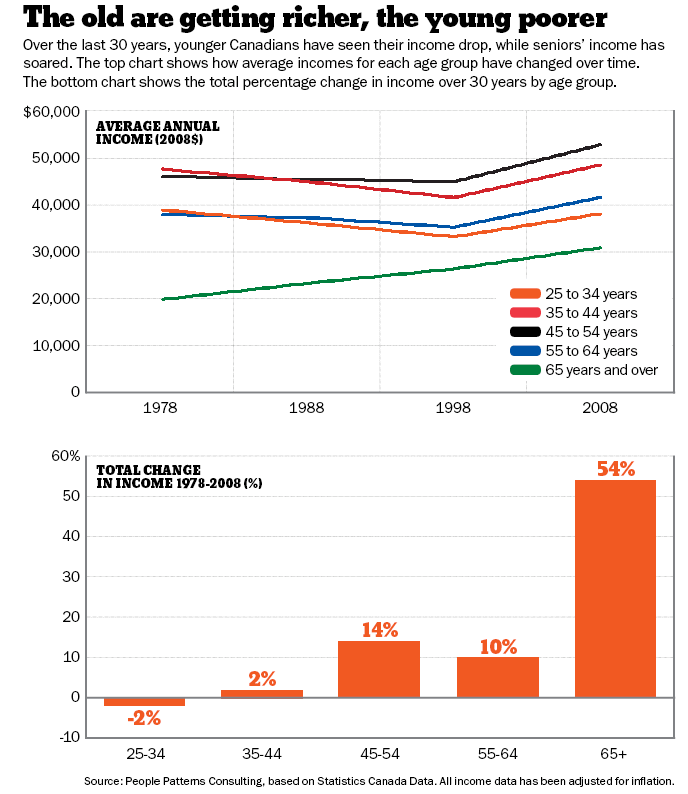

Sauvé found that when you look at incomes for the group of Canadians between the ages of 25 and 34, they haven’t increased by a penny for over three decades. Indeed, incomes actually dropped by 2% (all numbers are adjusted for inflation, so these are real gains and drops). Meanwhile, over the same period, the incomes for the older groups have been rocketing up. Canadians aged 65 and up have seen their incomes soar by an incredible 54%. Those aged 45 to 54 saw their incomes rise by 14%, and those aged 55 to 64 saw a 10% boost.

When we look at the net worth of the different age groups—meaning what they have when you add up the value of all their assets and subtract their debts—the situation for the young looks even worse. Canadians ages 25 to 34 saw a devastating 12% drop in their net worth—down to $83,000—between 1999 to 2005. During the same period, those ages 65 and up experienced a whopping 29% increase, to $519,100.

So what’s going on? Why are the young getting so much poorer while the old get wealthier and wealthier? Sauvé says a lot of the shift is due to government wealth transfers. Over the 30-year period we looked at, taxes have increased, while government programs for the young, such as grants for university, have decreased. At the same time, the older generation has enjoyed more generous tax breaks, such as income splitting, along with a truly amazing rise in government benefits from such programs as the Canada Pension Plan, Old Age Security and the Guaranteed Income Supplement.

Another huge driver of wealth for seniors has been home ownership. All age groups experienced a rise in wealth due to surging housing prices—especially between 1981 and 2006—but the biggest gains were for homeowners aged 75 and up, who saw their home values rise by 63% in real terms over that period. That’s because older Canadians were more likely to have more equity in their homes, and to own lower priced homes that shot up in value. This trend worked against the younger groups, who increasingly found they couldn’t get into the property market at all, because even starter homes were too expensive. Despite one of the biggest housing booms Canada has ever seen, since 1982 the rate of home ownership for those aged 55 and under has actually decreased.

Shifts in both the economy and society are driving these changes. The move away from manufacturing and towards knowledge-based jobs means it’s rare for young people without higher education to walk into high-paying jobs. Young Canadians have to stay in school longer before they can enter the paid workforce, and soaring tuition rates mean that students often graduate with heavy debt loads.

When young men and women finally have enough education to get a job, they still aren’t easy to come by. Canada’s youth unemployment rate is now 14.9%, much higher than the overall rate of 8%. And often the jobs that are available are contract or temporary jobs, a situation that can persist even as people move into their 30s and beyond.

How will today’s young people fare in the future? One possibility is that as the Boomers retire in the coming years, long-predicted labour shortages will finally lead to wage increases. However, some economists are concerned that the slow financial start for today’s youth will cripple them for years. “I’m worried the young will not be able to stay afloat,” says Armine Yalnizyan, senior economist with the Canadian Centre for Policy Alternatives. “With temporary jobs and no benefits and pensions, this generation cannot take care of itself or prepare for bad times. In the long run, some of these people will be fine—but a growing number will not.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Now's the time to toss the piggy bank and open a bank account instead

It's important to start teaching your kids about money early

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...