GICs: The problem with playing it safe

Will corporate bonds give her the boost she needs?

Advertisement

Will corporate bonds give her the boost she needs?

![Portfolio_Builder_banner_1256X300[2][2][2]](https://www.moneysense.ca/wp-content/uploads/2016/05/Portfolio_Builder_banner_1256X300222.jpeg)

Vancouver money coach Annie Kvick says losing 40% of your portfolio when you’re five to 10 years from retirement is stressful. But investing her entire portfolio in GICs and bonds is risky because Heather could lose her nest egg to inflation, or even outlive her money entirely. “Even though she wants safety, Heather needs some growth from equities for her portfolio to last,” says Kvick.

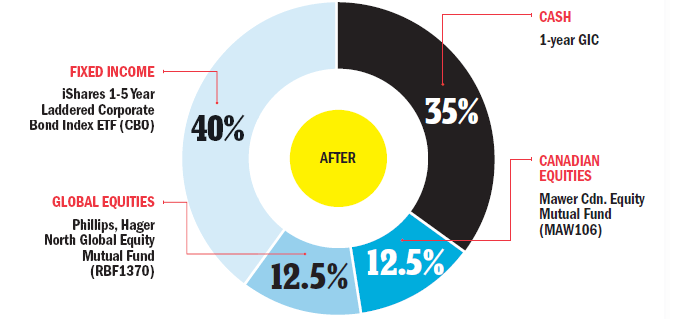

She wants Heather to keep 35% of her portfolio in cash, 25% in equities and 40% in fixed income. “By using exchange-traded funds (ETFs) and keeping fees low, she’ll get a 3.8% average annual real return,” says Kvick. She also wants Heather to think of her money in terms of three “buckets” of income. She’ll need one-third of her portfolio, or $70,000, between ages 65 and 75. So this first bucket will hold Heather’s ultra-safe all cash investments. The second $70,000 portion of her portfolio has a 15- to 25-year time horizon and will be used between ages 75 and 85; it can be structured 70% fixed income and 30% equities. The final $70,000 portion will be needed in 25 years or more, after age 85; it can be invested 50% in income and 50% in equities.

So Heather’s portfolio today should allocate $70,000 to cash, $79,000 to fixed income and $51,000 to equities. The cash can go into a one-year GIC, the fixed-income portion into the iShares 1-5 Year Laddered Corporate Bond Index ETF (CBO) and the equity portion in low-fee equity mutual funds, like those sold by Mawer or Phillips, Hager & North..

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Vancouver money coach Annie Kvick says losing 40% of your portfolio when you’re five to 10 years from retirement is stressful. But investing her entire portfolio in GICs and bonds is risky because Heather could lose her nest egg to inflation, or even outlive her money entirely. “Even though she wants safety, Heather needs some growth from equities for her portfolio to last,” says Kvick.

She wants Heather to keep 35% of her portfolio in cash, 25% in equities and 40% in fixed income. “By using exchange-traded funds (ETFs) and keeping fees low, she’ll get a 3.8% average annual real return,” says Kvick. She also wants Heather to think of her money in terms of three “buckets” of income. She’ll need one-third of her portfolio, or $70,000, between ages 65 and 75. So this first bucket will hold Heather’s ultra-safe all cash investments. The second $70,000 portion of her portfolio has a 15- to 25-year time horizon and will be used between ages 75 and 85; it can be structured 70% fixed income and 30% equities. The final $70,000 portion will be needed in 25 years or more, after age 85; it can be invested 50% in income and 50% in equities.

So Heather’s portfolio today should allocate $70,000 to cash, $79,000 to fixed income and $51,000 to equities. The cash can go into a one-year GIC, the fixed-income portion into the iShares 1-5 Year Laddered Corporate Bond Index ETF (CBO) and the equity portion in low-fee equity mutual funds, like those sold by Mawer or Phillips, Hager & North..

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...

Created By

Ratehub.ca

The Bank of Canada held its key rate at 2.75%, citing high uncertainty, tariffs and more.

Should you hold equities? Fixed income? An annuity? Or all three? Financial advisors debate the options in today’s “tariffied”...

Helping a grandchild pay for post-secondary education is a smart gift that keeps giving. Here’s how to maximize your...