By David Aston on August 17, 2015 Estimated reading time: 16 minutes

A defence of active investing

By David Aston on August 17, 2015 Estimated reading time: 16 minutes

It is possible to pick mutual funds that beat the benchmarks

Advertisement

(Illustration by Sam Island)

If you’ve been investing for a while, you’ve seen the stock market do some pretty crazy things. Who can forget the tech boom of the 1990s? Or the devastating market meltdown of 2008-2009?

I respect Mr. Market—the manic-depressive character legendary investor Benjamin Graham used to describe the ever-changing whims of the stock market—but I prefer not to be obligated to always buy what Mr. Market is buying and always sell what Mr. Market is selling. I don’t necessarily want to have most of my Canadian stocks in banks and resource companies just because that’s what the index says I should do. Instead, I would rather try to invest for the long term in companies that provide quality and value at a reasonable price while being diversified by sector. I want to follow my own risk profile in picking investments, rather than implicitly take on the average risk profile of the overall market at that particular moment. That’s why I invest most of my money through skilled advisors and money managers who share this outlook and charge what I regard as reasonable fees.

All that makes me an active investor, and by extension, a heretic here at MoneySense. You may be aware there is a great debate these days between the advocates of active investing, who choose investments they believe will outperform the markets’ benchmark indexes, and passive investors, who buy index funds and ETFs meant to match the benchmarks’ returns. While active investing is what investors have traditionally done and most still do, passive investing or index investing is gaining adherents and has had the upper hand in articles in academia and the media, including at this magazine. To be sure, advocates of passive investing make a sound case that most active investors underperform the market after fees and therefore most people can do better by investing passively in index ETFs with low fees. So passive investing is a great way to invest, but that doesn’t mean it is always the best way to invest for everyone.

I believe there is a case to be made for active investing for many investors, provided it is done the right way. To make active investing work effectively, you need to be able to do three key things. First, you need to be highly selective in the investments you choose, focusing on ones with a proven long-term approach. Secondly, you need to set an appropriate asset allocation and follow a disciplined investment process, which includes rebalancing. Thirdly, you need to make sure the investment fees you pay are reasonable.

[brightcove video_id=”6023929385001″ account_id=”6015698167001″ player_id=”lYro6suIR”]

In what follows, I will take you through each of those three key tasks. I focus primarily on active investors who use mutual funds to invest in stocks, rather than those who want to select their own individual securities, since that involves different and more complicated issues. (See “So you want to pick your own stocks” for more on how to build a portfolio stock by stock.)

A tough crowd to beat

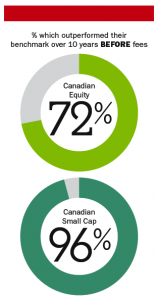

There is lots of evidence that, on average, mutual funds and other active investment vehicles underperform the market after fees. The proportion of U.S. mutual funds that have underperformed the market over 10 years is roughly 70%, according to research by Lipper Associates. More recent Morningstar research by Christopher Davis and Michael Keaveney found that 86% of funds in the broad Canadian Equity category underperformed their benchmarks over the previous decade. As respected investing authority and Winning the Loser’s Game author Charles Ellis has written: “The cruel irony is that so many active managers are so skillful, hardworking, and capable that they collectively dominate the market and thus few, if any, can beat the crowd.” Put another way, active managers pretty much are the market, so it is impossible for them as a group to outperform themselves, particularly after deducting fees.

Given all that evidence, most people would logically conclude that they should instead invest in broad-based index exchange-traded funds (ETFs) with really low fees, and take what the market hands you at a lower cost. But passive investing has its shortcomings, particularly in its classic form based on using market capitalization to weight the stocks that go into an ETF. That approach loads you up on sectors and stocks that are hot, like Nortel and Blackberry during their heydays, or resource stocks during the commodity boom. Then you’re forced to unload them when they grow cold. A purely passive approach means your Canadian investments should be heavily allocated to resources and financials because that is what’s in the index, whether those sector weightings fit your needs or not.

If the markets were completely efficient, meaning that all stocks are always priced at what they are actually worth, then indexing would probably be the way to go. But the bulk of evidence now shows that’s not the case. “The financial literature no longer stands firmly in the efficient markets camp,” says Eric Kirzner, professor of finance at the Rotman School of Management, University of Toronto. “Markets are at times efficient, at other times not efficient. Markets for some stocks are and markets for some stocks aren’t. You do go through periods where it may be possible to find undervalued securities because of the extreme emotions that investors bring to the marketplace.”

There’s lots of evidence that some investors and some active investment styles do outperform over the long term. For example, there is pretty conclusive evidence that “value” investing has consistently beaten “growth” investing over the long term. (Value’s overall outperformance over growth is about 3% a year on average over very long periods of time, says Kirzner.) There’s also strong but less overwhelming evidence of long-term outperformance by other approaches, including low volatility investing, dividend investing and momentum investing.

It’s a fact that at any given time, some of the actively managed mutual funds out there will outperform the market, but the tricky part comes in trying to identify who these outperformers are going to be ahead of time. The fact that a fund has had a few good years doesn’t mean that it will continue to thrive. After all, a manager might perform exceptionally well for a while because she happens to be invested in the right thing at the right time, such as being a technology fund during the technology boom. If you invest in a fund solely based on its record, you may be jumping in at the height of a cycle or fad that it happened to benefit from, which is the precisely the wrong time to invest.

Because of that, while Kirzner says that the active pursuit of outperformance for at least part of your portfolio is a worthy goal for institutions and sophisticated investors, he doesn’t think most individual investors are up to it. “They probably don’t have the time, the training, or the expertise to pick the managers that can do it. Their chance of finding them at the mutual fund level is really quite low. That’s consistent with the studies,” argues Kirzner, who has a long history of advocating index investing using ETFs.

Finding the best funds

But while I agree with Kirzner that it’s not easy, I do believe that individual investors can find good active managers who stand a strong chance of outperforming over the long term. A good place to start is a third-party expert source, such as Morningstar’s analyst rating of mutual funds, available on Morningstar.ca. Look for mutual funds rated gold, silver or bronze in declining order of confidence. (You shouldn’t rely on the Morningstar star ratings, which are based solely on historical performance and aren’t necessarily indicative of future performance.)

There are also certain fund families that have demonstrated an ability to achieve strong results following a disciplined and effective long-term process. These include, for example, funds from Mawer, Beutel Goodman, Mackenzie Ivy, Steadyhand, Leith Wheeler, and Chou Associates. All are mutual fund companies that follow a disciplined and consistent long-term process.

Typically these funds invest in well-managed businesses with strong competitive positions that generate lots of cash flow and which can be expected to continue to do well in the future. The funds are careful to pay only a reasonable price when they buy and generally avoid trendy stocks. Sometimes they’re willing to pay a little more for growing companies, but only if growth is considered reliable. Some consider themselves “value” investors, but others describe their style in other terms. Perhaps most critically, they try to think over long time horizons, don’t worry too much about immediate performance in the next year, and invest in a way that is distinct from the index.

Keeping the balance right

Of course, there’s more to being a successful investor than picking good investments. You also need to set an appropriate asset allocation and follow a disciplined investment process. Most investors should follow a buy-and-hold strategy that maintains their set asset allocation, rebalancing when actual allocations depart substantially from their targets (although a modest dose of contrarianism can help sophisticated investors). “It’s really important that you make sure you spend the time on the asset allocation and the investment process,” advises Kirzner.

What many investors don’t realize is that you can underperform the market in two ways. You can invest in a particular fund (e.g. a Canadian equity fund) that underperforms its benchmark (e.g. the S&P/TSX Composite Index) for the period that you’ve invested in it. You can also underperform by timing the market poorly (e.g. you bulk up in Canadian equities at the wrong time), which you can do just as much by investing in ETFs as mutual funds. It’s easy to get caught up in market sentiment and buy hot stocks or hot sectors near their peaks and sell when they’ve gone cold, which means you’re buying high and selling low. It can also happen more subtly, as when many investors scarred by the 2008-2009 market crash waited until they had seen a few years of rising markets before getting back into stocks.

Many studies have shown that the average investor’s cost of mistiming the market is high. For example, Morningstar found that the average U.S. investor underperformed the buy-and-hold performance of the typical mutual fund by 2.5% per year for the decade ended Dec. 31, 2013. A study by Ilia Dichev of Emory University of 19 stock markets around the world from 1973 to 2004 found that actual investor returns underperformed a buy-and-hold approach by an average of 1.5% a year.

Successful active fund managers tend to insulate themselves from market sentiment by following an independent and dispassionate approach to valuing each stock’s worth. They only buy stocks that are reasonably priced relative to the “intrinsic” value they estimate, and sell stocks when they become overpriced. They understand that good companies can be bad investments if one pays too much for them, but the reverse isn’t true: cheapness does not turn a bad company into a good investment. “You need to figure out intrinsic value, buy when cheap and sell when expensive,” says George Athanassakos, professor of finance and the Ben Graham Chair in Value Investing at Ivey Business School. “Most investors behave like momentum traders. They like to invest in winners. But if you jump on the hot stocks, you never make any money.”

If you find a good fund manager, invest mainly in his or her broad-based funds and avoid narrowly focused sector funds, advises Dan Hallett, vice-president of HighView Financial Group, an investment counsel firm for affluent families. That way you avoid making bets on hot stock sectors, he points out. Also, it allows you to benefit from the skill of the fund managers to shift money from stocks and sectors that become expensive into others that become attractively priced. Surprisingly, many investors who think they are following a passive approach are actually using narrow-focused ETFs to make active bets, he says. “It is cheap active management because they’re making a decision to focus on Brazil, or agricultural stocks, or gold, or whatever.”

If the process of setting and maintaining an asset allocation seems complicated, there is a smart way for active investors to keep it simple, says Hallett. Simply invest in a balanced mutual fund with a top-notch provider that has a good reputation across different broad equity and fixed income asset categories, he says. “It’s as foolproof as possible. The next time stocks drop by 40%, you don’t have to worry about whether to rebalance or not. As long as you leave the money invested, it will get rebalanced for you.”

Watch out for fees

Even a good mutual fund won’t help you beat the market if its fees are too high. So you’ll need to make sure your mutual fund fees are reasonable for what you get. It’s also important to realize that when you compare active investing with passive investing, you need to make “apples-and-apples” comparisons.

If you’re a do-it-yourself investor, you should compare the low cost of ETFs with the growing number of mutual funds designed explicitly for do-it-yourselfers, which are much cheaper than conventional funds because they don’t include full trailer fees for advisors.

Mutual funds for do-it-yourselfers include offerings from low-fee fund companies such as Mawer, Steadyhand, and Leith Wheeler, as well as “D” series versions of conventional funds offered by mainstream fund providers. Low fee funds typically charge you 1.2% to 1.8% for equity funds. That’s still a lot more than broad-based passive ETFs, but the gap becomes smaller.

When you start looking at other forms of active investing besides mutual funds, passive investing isn’t always cheaper. If you have at least $500,000 to invest and you choose to invest actively with a portfolio manager (also known as an investment counsellor), you typically pay 1% to 1.5% a year in fees. Brokers will manage your money for somewhere between 1% and 2% if they’re not selling you mutual funds. In comparison, the all-in cost of passive investing with an advisor will typically cost you about 1% to 1.5% a year, after including the advisor’s fees plus taxes and ETF fees. So the overall cost is often in the same ballpark whether active or passive.

If you can’t beat them join them

By now you probably realize that both passive and active investing have their particular strengths. If you want to try to get the best of both worlds, consider mixing the two.

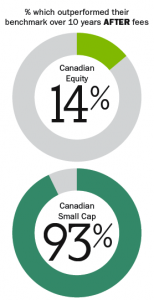

Broad-based ETFs are a great default option if you can’t find an active alternative that you are convinced is better. In general, active strategies tend to perform relatively well in market niches that tend not to be as widely followed by analysts, whereas beating the market is particularly tough in broad categories that are widely followed. Therefore it can make sense to follow a “core and explore” approach where you cover off at least some of your core needs (like U.S. large-cap stocks) with ETFs, then go for active mutual funds for some of the more specialized asset categories (like small-cap stocks). While few large-cap Canadian equity funds outperformed the market in the Morningstar study cited earlier, the vast majority of active Canadian small-cap funds—some 93%—outperformed their benchmarks. Christopher Davis, director of Morningstar manager research says: “Even mediocre to poor small-cap mutual fund managers beat the index in Canada.” You can also invest in a different kind of ETF called “strategic beta” (also called “smart beta”) which can combine attractive features of both active and passive investing at relatively low cost.

Dial down risk in your portfolio

Most of the debate about whether active investing can outperform the market is focused on returns. Implicitly the comparison is with passive ETFs bearing average risks that reflect the overall market. In my view, there should be as much consideration given to risk as there is to return.

To me, one of the advantages of a proper active investing approach is that you are able to go for stocks with a bit lower risk level than the overall market, rather than be forced to accept the “average” market risk. Approaches which can be considered low risk include dividend investing and low-volatility investing. This can be particularly beneficial to investors who are recently retired or approaching retirement, since the impact of a big market downturn can be especially devastating in the first few years of retirement. (This is known as “sequence of returns risk.”) As Hallett says: “People shouldn’t just focus on raw outperformance. On the active side, if you can outperform the benchmark, great. But even if you can’t, if you can achieve a return at or near the benchmark but with significantly less risk, that really is a form of successful active management.”

You can make active investing work effectively if you carefully select investments with a proven long-term investment approach, follow a disciplined investment process, and make sure you pay reasonable fees. Still, active investing isn’t right for everyone, there are no guarantees of future outperformance and you need to temper your expectations. “There’s no magic pill and there’s no pot of gold,” says Kirzner.

But for the right person, active investing can be a great way to invest. While you need to give Mr. Market due respect, you don’t always need to tag along closely wherever Mr. Market happens to go. With the benefit of good advisors and money managers, sometimes you’re best off going your own way.

Mind the gap

How many active Canadian equity fund managers outperformed their index?

Notes: Source: Morningstar Manager Research Paper, “Have Active Canadian Equity Fund Managers Earned Their Keep?” by Christopher Davis and Michael Keaveney, May 7, 2015.’

The comparison period covers the 10 Years ended Feb. 28, 2015. For the broad Canadian Equity category, the comparison was between 59 funds and the iShares S&P/TSX Capped Composite ETF. For the small-cap comparison, 46 funds were compared with the iShares S&P/TSX Small Cap ETF. (The returns for the small-cap ETF were estimated for the period prior to inception in June 2007 by taking the underlying index on which the ETF is based and adjusting it for fees.)

The authors indicated they couldn’t fully explain the very high outperform rate of active managers in the Canadian small-cap category and plan to delve into possible explanations in a follow-up study.

Notes: Source: Morningstar Manager Research Paper, “Have Active Canadian Equity Fund Managers Earned Their Keep?” by Christopher Davis and Michael Keaveney, May 7, 2015.’

The comparison period covers the 10 Years ended Feb. 28, 2015. For the broad Canadian Equity category, the comparison was between 59 funds and the iShares S&P/TSX Capped Composite ETF. For the small-cap comparison, 46 funds were compared with the iShares S&P/TSX Small Cap ETF. (The returns for the small-cap ETF were estimated for the period prior to inception in June 2007 by taking the underlying index on which the ETF is based and adjusting it for fees.)

The authors indicated they couldn’t fully explain the very high outperform rate of active managers in the Canadian small-cap category and plan to delve into possible explanations in a follow-up study.

Notes: Source: Morningstar Manager Research Paper, “Have Active Canadian Equity Fund Managers Earned Their Keep?” by Christopher Davis and Michael Keaveney, May 7, 2015.’

The comparison period covers the 10 Years ended Feb. 28, 2015. For the broad Canadian Equity category, the comparison was between 59 funds and the iShares S&P/TSX Capped Composite ETF. For the small-cap comparison, 46 funds were compared with the iShares S&P/TSX Small Cap ETF. (The returns for the small-cap ETF were estimated for the period prior to inception in June 2007 by taking the underlying index on which the ETF is based and adjusting it for fees.)

The authors indicated they couldn’t fully explain the very high outperform rate of active managers in the Canadian small-cap category and plan to delve into possible explanations in a follow-up study.