Why you’re getting a tax break on dividend income

In some provinces, you may not have to pay any taxes at all

Advertisement

In some provinces, you may not have to pay any taxes at all

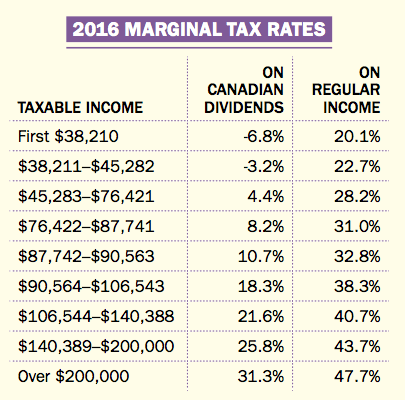

Note that Canadian dividends will get you a nice tax break at all income levels, but the benefit is especially large if you’re in a lower tax bracket.

Amazingly, if you’re in a low enough tax bracket in some provinces (including B.C.), you not only pay no taxes on dividend income at all, but the dividends cause a further small reduction in the rest of your taxes. This is a rare and delightful example of a “negative marginal tax rate”.

The actual calculations are pretty complex and go through a three-step process. First, dividends received are grossed up and included in taxable income. Second, a percentage tax rate is applied and, third, you receive a dividend tax credit which knocks your net taxes back down. The positive impact of the dividend tax credit is greater than the negative impact of the gross up.

A further complication to consider is that while dividend income is taxed favourably, it hurts you when it comes to income-tested government benefits such as the Old Age Security clawback. That’s because the income test incorporates grossed-up income—step one of the three-part process—not the dividends you actually receive.

Related: How to buy dividend stocks

Note that Canadian dividends will get you a nice tax break at all income levels, but the benefit is especially large if you’re in a lower tax bracket.

Amazingly, if you’re in a low enough tax bracket in some provinces (including B.C.), you not only pay no taxes on dividend income at all, but the dividends cause a further small reduction in the rest of your taxes. This is a rare and delightful example of a “negative marginal tax rate”.

The actual calculations are pretty complex and go through a three-step process. First, dividends received are grossed up and included in taxable income. Second, a percentage tax rate is applied and, third, you receive a dividend tax credit which knocks your net taxes back down. The positive impact of the dividend tax credit is greater than the negative impact of the gross up.

A further complication to consider is that while dividend income is taxed favourably, it hurts you when it comes to income-tested government benefits such as the Old Age Security clawback. That’s because the income test incorporates grossed-up income—step one of the three-part process—not the dividends you actually receive.

Related: How to buy dividend stocks

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

These top 10 Canadian momentum stocks all returned more than 40% over the past three months.

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

RBC Direct Investing has introduced commission-free trades on 50 exchange-traded funds (ETFs) from partner iShares.

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

If you’re worried about a recession in Canada, you’re not alone. Here’s what to expect and how you can...

Dollarama reports increases in profits and sales, Transat deals with Canadian travellers avoiding the U.S., and Roots sees Q1...