Am I on track to retire at age 60?

Milan Sengupta of Calgary wants an annual net retirement income of $50,000 so he can travel extensively

Advertisement

Milan Sengupta of Calgary wants an annual net retirement income of $50,000 so he can travel extensively

The verdict

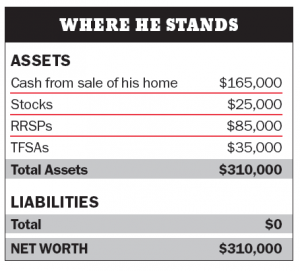

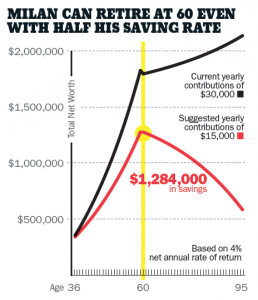

Milan is on track to easily meet his goal, says Vickie Campbell, a certified financial planner with Ryan Lamontagne in Ottawa. “If Milan saves $30,000 annually, and he spends $50,000 a year net from his nest egg starting at age 60, his retirement savings will last him beyond age 95,” she says. “He’s saving much more than he needs to meet his goal.” If Milan continues investing $30,000 a year until age 60, and we assume an annual 4% rate of return, he’ll have a $1.8 million nest egg by the time he retires. Without including any CPP or OAS payments, which he will be entitled to starting at age 60 and 67, his nest egg will be able to maintain a net annual income of $50,000 from age 60 to 95, and then some. At 95, his portfolio would still be worth a whopping $2.1 million because of the power of compounding coupled with the modest withdrawals he intends to make from the nest egg. In fact, if Milan saves just $15,000 annually until age 60, he’ll still have more than enough. At age 60, his nest egg will be worth $1.28 million and at 95, $581,933. “A portfolio with 50% invested in equities and 50% in fixed income will give Milan the returns—and the retirement—he wants. He doesn’t need to take more risk.”

The verdict

Milan is on track to easily meet his goal, says Vickie Campbell, a certified financial planner with Ryan Lamontagne in Ottawa. “If Milan saves $30,000 annually, and he spends $50,000 a year net from his nest egg starting at age 60, his retirement savings will last him beyond age 95,” she says. “He’s saving much more than he needs to meet his goal.” If Milan continues investing $30,000 a year until age 60, and we assume an annual 4% rate of return, he’ll have a $1.8 million nest egg by the time he retires. Without including any CPP or OAS payments, which he will be entitled to starting at age 60 and 67, his nest egg will be able to maintain a net annual income of $50,000 from age 60 to 95, and then some. At 95, his portfolio would still be worth a whopping $2.1 million because of the power of compounding coupled with the modest withdrawals he intends to make from the nest egg. In fact, if Milan saves just $15,000 annually until age 60, he’ll still have more than enough. At age 60, his nest egg will be worth $1.28 million and at 95, $581,933. “A portfolio with 50% invested in equities and 50% in fixed income will give Milan the returns—and the retirement—he wants. He doesn’t need to take more risk.”  Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

Dollarama reports increases in profits and sales, Transat deals with Canadian travellers avoiding the U.S., and Roots sees Q1...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...