An income layer cake

Your retirement income will come from a variety of sources: government, pensions, your portfolio, part-time work, and maybe even your home equity. How can you keep your cash flow smooth and tax-efficient?

Advertisement

Your retirement income will come from a variety of sources: government, pensions, your portfolio, part-time work, and maybe even your home equity. How can you keep your cash flow smooth and tax-efficient?

It’s easy to feel overwhelmed with questions about how to draw retirement income. When do you start collecting government benefits? Which do you tap first: RRSPs, Tax-Free Savings Accounts (TFSAs) or non-registered money? How do other sources of cash flow like employer pensions, annuities and home equity fit in? How do you make sure your income is reliable?

These issues are daunting enough when you consider them individually. But then there’s the burning overall question: How do you put it all together?

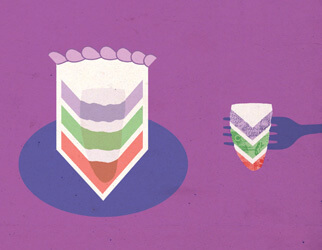

One good approach is called income layering. While there are several versions, the general idea involves using different sources or “layers” of income to make cash flow smooth, reliable and tax-efficient. Think of it as a layer cake of cash. The base (what I’ve called Layer 1) is composed of income that is highly reliable, but usually not tax-efficient or flexible, such as government and employer pensions, annuities, and income from part-time work (if it is reliable and steady). Then you add a more tax-efficient Layer 2: this includes sources of income that are less reliable but more flexible, like your investment portfolio. Finally, you top it all off with Layer 3: the equity in your home or other property, which you can tap late in life if necessary.

Many financial planners use a variation of this approach, including Douglas Nelson, author of Master Your Retirement, and Daryl Diamond, author of Your Retirement Income Blueprint. In what follows, we’ll show you how you can adapt these ideas to your own situation.

“It’s all about taking less risk, paying less tax, generating more income and connecting the dots in those pieces,” says Nelson, a portfolio manager with Nelson Financial Consultants of Winnipeg.

It’s easy to feel overwhelmed with questions about how to draw retirement income. When do you start collecting government benefits? Which do you tap first: RRSPs, Tax-Free Savings Accounts (TFSAs) or non-registered money? How do other sources of cash flow like employer pensions, annuities and home equity fit in? How do you make sure your income is reliable?

These issues are daunting enough when you consider them individually. But then there’s the burning overall question: How do you put it all together?

One good approach is called income layering. While there are several versions, the general idea involves using different sources or “layers” of income to make cash flow smooth, reliable and tax-efficient. Think of it as a layer cake of cash. The base (what I’ve called Layer 1) is composed of income that is highly reliable, but usually not tax-efficient or flexible, such as government and employer pensions, annuities, and income from part-time work (if it is reliable and steady). Then you add a more tax-efficient Layer 2: this includes sources of income that are less reliable but more flexible, like your investment portfolio. Finally, you top it all off with Layer 3: the equity in your home or other property, which you can tap late in life if necessary.

Many financial planners use a variation of this approach, including Douglas Nelson, author of Master Your Retirement, and Daryl Diamond, author of Your Retirement Income Blueprint. In what follows, we’ll show you how you can adapt these ideas to your own situation.

“It’s all about taking less risk, paying less tax, generating more income and connecting the dots in those pieces,” says Nelson, a portfolio manager with Nelson Financial Consultants of Winnipeg.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

Dollarama reports increases in profits and sales, Transat deals with Canadian travellers avoiding the U.S., and Roots sees Q1...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Laurentian Bank reports profits and BRP reports healthy margins and posts for a new CEO.

Thanks for the practical and well rounded plan. I’m just wondering if it’s best regardless of age to tap into all pension benefits asap – regardless of life expectancy- to maximize any potential interest on savings? Assuming of course you can save it?