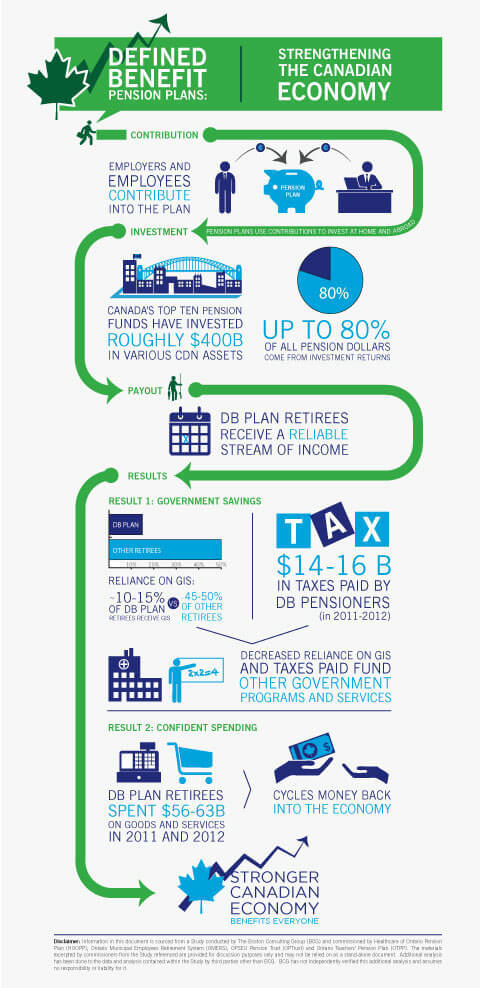

Defined-benefit plans are great: We already knew that

However attractive defined-benefit pension plans are for employees, many employers just don't want to bear the burden any longer.

Advertisement

However attractive defined-benefit pension plans are for employees, many employers just don't want to bear the burden any longer.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Review the 2026 CPP payment dates, how much you could receive, when to apply, and how the Canada Pension...

Plaintiffs allege the Canada Pension Plan is exposing their retirement savings to unnecessary risk by underestimating climate change impacts.

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

The benefits of depleting savings to avoid estate taxes depends on many variables. But if you live a decade...

Should you hold equities? Fixed income? An annuity? Or all three? Financial advisors debate the options in today’s “tariffied”...

Some Canadian seniors enter retirement without savings or run out of money over time. Here’s how they can stay...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...

The senior vice president of retail and wealth at Meridian shares the importance of budgeting and investing in your...