The right way to draw down on retirement savings

Stave off retirement ruin with some quick math

Advertisement

Stave off retirement ruin with some quick math

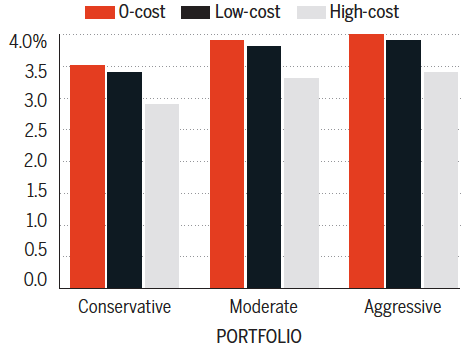

Notes: This figure models expense ratios of 0% (for 0-cost), and 0.25% (for low-cost), and 1.25% (for high-cost). This figure’s projections, generated by the Vanguard Capital Markets Model, are based in U.S. dollars as of December 31, 2011, and assume an 85% overall portfolio success rate.

Source: Vanguard

Jonathan Chevreau is Founder of the Financial Independence hub and co-author of Victory Lap Retirement. Read more of his Retired Money column here.

Notes: This figure models expense ratios of 0% (for 0-cost), and 0.25% (for low-cost), and 1.25% (for high-cost). This figure’s projections, generated by the Vanguard Capital Markets Model, are based in U.S. dollars as of December 31, 2011, and assume an 85% overall portfolio success rate.

Source: Vanguard

Jonathan Chevreau is Founder of the Financial Independence hub and co-author of Victory Lap Retirement. Read more of his Retired Money column here.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

Dollarama reports increases in profits and sales, Transat deals with Canadian travellers avoiding the U.S., and Roots sees Q1...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Laurentian Bank reports profits and BRP reports healthy margins and posts for a new CEO.

The benefits of depleting savings to avoid estate taxes depends on many variables. But if you live a decade...