Single retirees: The power of one

Meet three sixty-something singles who breezed past those obstacles and made it work

Advertisement

Meet three sixty-something singles who breezed past those obstacles and made it work

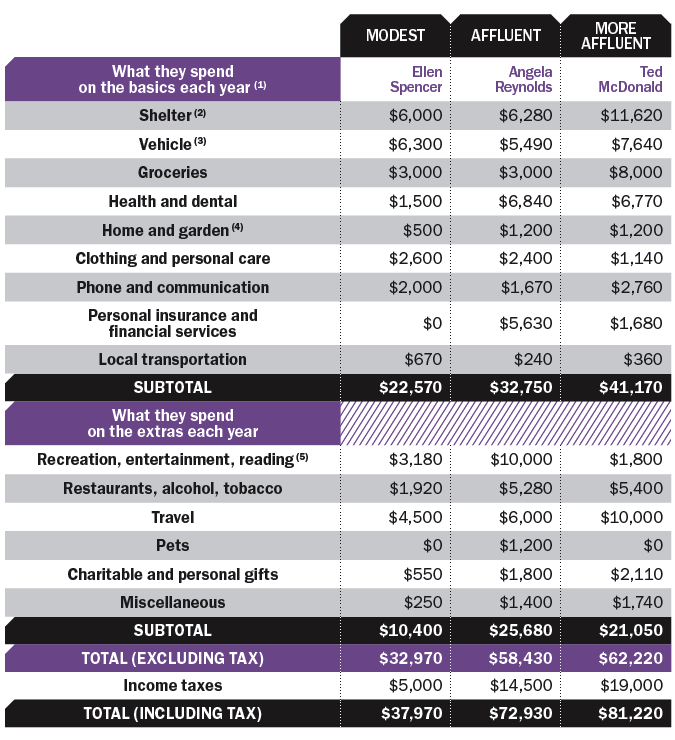

(1) Annie Kvick of Money Coaches Canada helped estimate these budgets. (2) Includes property taxes, utilities, maintenance, home insurance, rent and mortgage payments. (3) We’ve added $2,000 a year for depreciation. (4) Includes cleaning supplies, furnishings, appliances, garden supplies and services. (5) Includes computer equipment and supplies, recreation vehicles, games of chance, educational costs.

(1) Annie Kvick of Money Coaches Canada helped estimate these budgets. (2) Includes property taxes, utilities, maintenance, home insurance, rent and mortgage payments. (3) We’ve added $2,000 a year for depreciation. (4) Includes cleaning supplies, furnishings, appliances, garden supplies and services. (5) Includes computer equipment and supplies, recreation vehicles, games of chance, educational costs.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Incorporating can eliminate the need to pay CPP contributions if you are self-employed but there are trade-offs that should...

Artificial intelligence is best at overcoming the friction that stops you from taking up new pursuits, users insist.

Could moving your RRIF into segregated funds lower estate taxes? Maybe—but higher fees and other trade-offs could leave your...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving benefits, and...

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...