Don’t be fooled by this interest rate mistake

A one percentage point move is not the same as a 1% move

Advertisement

A one percentage point move is not the same as a 1% move

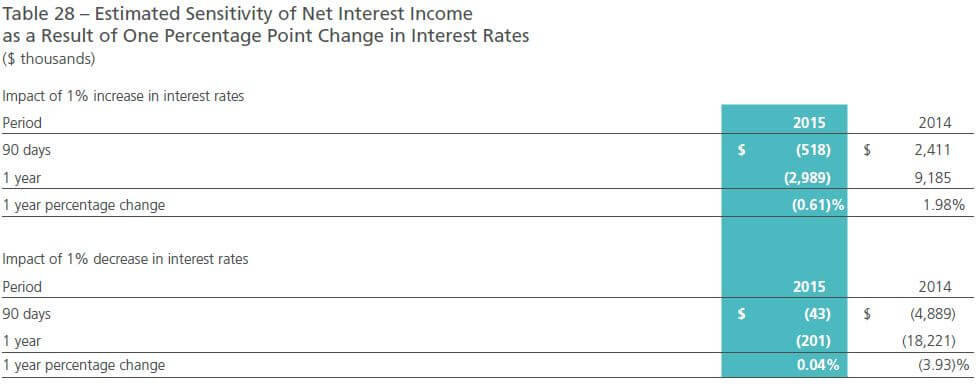

The table shows what the bank’s risk managers think will happen to its net interest income in the event that interest rates climb, or fall, by one percentage point. The same move is also described as a 1% increase, or decrease, in interest rates. Problem is, in almost all cases, a one percentage point move is not the same as a 1% move.

Let’s say interest rates start at 2%. A one percentage point increase would push them up to 3%. Alternately, one can say that interest rates have increased by 50% when they climb from 2% to 3%.

When you boost a 2.00% rate by 1.00% you get 2.02% because 1.00% of 2.00% is 0.02%. (I’ll discuss significant figures another day.)

That said, there is a special case when a one percentage point increase is equivalent to a 1% increase. It occurs when interest rates start at 100%. In this case, both accurately describe an interest rate climb from 100% to 101%.

To be fair to the bank in question, it is reasonably clear that the table shows what they expect will happen under a one percentage point move rather than a 1% move. Nonetheless, it is something worth clearing up in next year’s report.

I hasten to add that basis points are also widely used when talking about interest rate changes. One basis point is equal to one hundredth of a percentage point. For instance, when a 4.00% interest rate climbs by 10 basis points it moves from 4.00% to 4.10%.

When describing differences in percentages (interest rates, growth rates, returns, etc.) you’ll do your readers a kindness by using percentage points or basis points.

The table shows what the bank’s risk managers think will happen to its net interest income in the event that interest rates climb, or fall, by one percentage point. The same move is also described as a 1% increase, or decrease, in interest rates. Problem is, in almost all cases, a one percentage point move is not the same as a 1% move.

Let’s say interest rates start at 2%. A one percentage point increase would push them up to 3%. Alternately, one can say that interest rates have increased by 50% when they climb from 2% to 3%.

When you boost a 2.00% rate by 1.00% you get 2.02% because 1.00% of 2.00% is 0.02%. (I’ll discuss significant figures another day.)

That said, there is a special case when a one percentage point increase is equivalent to a 1% increase. It occurs when interest rates start at 100%. In this case, both accurately describe an interest rate climb from 100% to 101%.

To be fair to the bank in question, it is reasonably clear that the table shows what they expect will happen under a one percentage point move rather than a 1% move. Nonetheless, it is something worth clearing up in next year’s report.

I hasten to add that basis points are also widely used when talking about interest rate changes. One basis point is equal to one hundredth of a percentage point. For instance, when a 4.00% interest rate climbs by 10 basis points it moves from 4.00% to 4.10%.

When describing differences in percentages (interest rates, growth rates, returns, etc.) you’ll do your readers a kindness by using percentage points or basis points.

| Name | Price | P/B | P/E | Earnings Yield | Dividend Yield |

|---|---|---|---|---|---|

| CIBC (CM) | $98.47 | 1.89 | 10.77 | 9.28% | 4.92% |

| National Bank (NA) | $45.03 | 1.62 | 13.05 | 7.66% | 4.89% |

| Power (POW) | $28.30 | 1.06 | 8.88 | 11.26% | 4.73% |

| Shaw (SJR.B) | $25.25 | 2.05 | 9.15 | 10.93% | 4.69% |

| Bank of Nova Scotia (BNS) | $65.45 | 1.61 | 11.69 | 8.56% | 4.40% |

| BCE (BCE) | $62.35 | 4.33 | 19.67 | 5.08% | 4.38% |

| TELUS (T) | $42.96 | 3.33 | 19.09 | 5.24% | 4.28% |

| Bank of Montreal (BMO) | $84.84 | 1.53 | 12.68 | 7.89% | 4.05% |

| Royal Bank (RY) | $80.01 | 1.96 | 12.01 | 8.32% | 4.05% |

| TD Bank (TD) | $56.57 | 1.67 | 12.86 | 7.78% | 3.89% |

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Shopify and energy companies delivered strong quarterly results, while Telus posted a steep loss. Catch up on this week's...

Strategy sold millions in Bitcoin. Learn why, how institutions are tackling quantum computing risks, and whether Coinbase is...

Crypto is going mainstream in Canada. A new OSC survey finds ownership has more than doubled, while advisor recommendations...

The CRA is cracking down on TFSA overcontributions. Learn how penalties work, how to correct mistakes, and when...

Copper production lifted First Quantum, while Intact faced higher catastrophe claims. Catch up on the latest quarterly results from...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup