Where to invest $500,000

More money gets you more options, and some come at a lower cost

Advertisement

More money gets you more options, and some come at a lower cost

If you want to turn over day-to-day management of your money to seasoned professionals, your best option if you have at least $500,000 may be an investment counsel firm (also known as a “portfolio management firm” or “private investment counsel”). These money managers make the day-to-day investment decisions subject to your overall direction, which is known as “discretionary” portfolio management.

While their specific investment philosophies vary, they generally emphasize prudence. “The culture is this is a stay-rich portfolio, not a get-rich portfolio,” says Kelly Rodgers, president of Rodgers Investment Consulting. The main downside? You need a lot of money to access this option. Only some firms will take you as a client if you have $500,000 to invest—many require that you have $1 million or more.

Investment counsel firms are known for rigorous investment processes provided by a team of exceptionally well-qualified professionals. Typically you meet with an account representative holding the well-regarded chartered financial analyst (CFA) designation. Compared to most financial professionals “they have far more in-depth training in portfolio analysis and portfolio construction,” says Rodgers. That person thoroughly examines your financial situation, needs and risk tolerance, and then helps set your asset allocation, all of which is documented in an Investment Policy Statement (IPS). The money is then turned over to investment professionals working in the background who invest the money according to the direction in the IPS.

Fees are typically 1% to 1.5%, roughly comparable to rates charged by full-service brokers for stock and bond portfolios of a similar size, but cheaper than what you will pay for mutual funds through an adviser.

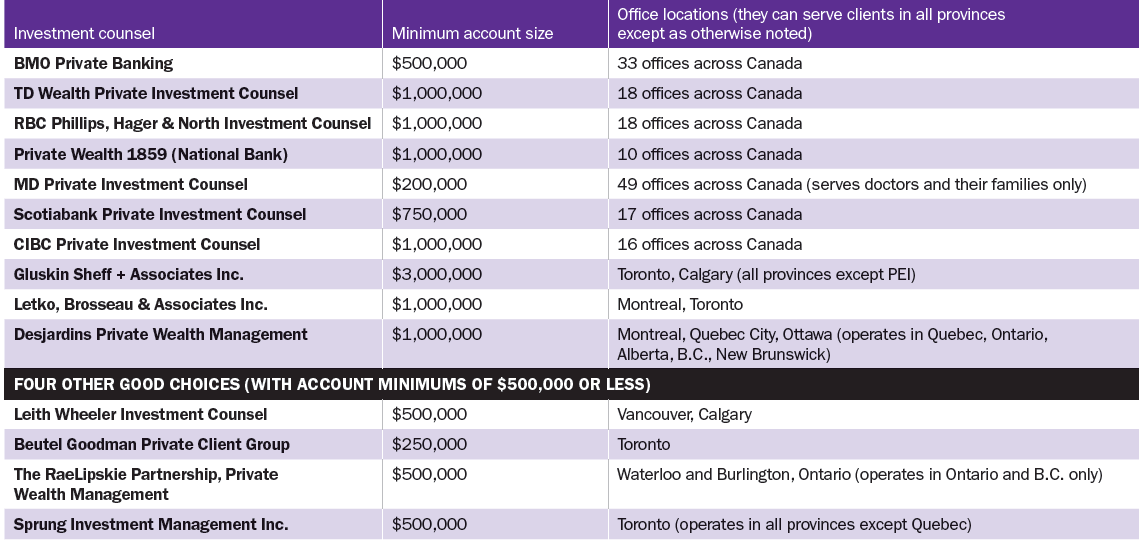

Despite their investment prowess, these low-key firms aren’t well-known. While many of the largest firms are divisions of banks, their services are rarely described in ads. For a list of leading investment counsel firms, see the tables below. You can also find a more extensive listing of firms at the Portfolio Management Association of Canada website, portfoliomanagement.org.

If you want to turn over day-to-day management of your money to seasoned professionals, your best option if you have at least $500,000 may be an investment counsel firm (also known as a “portfolio management firm” or “private investment counsel”). These money managers make the day-to-day investment decisions subject to your overall direction, which is known as “discretionary” portfolio management.

While their specific investment philosophies vary, they generally emphasize prudence. “The culture is this is a stay-rich portfolio, not a get-rich portfolio,” says Kelly Rodgers, president of Rodgers Investment Consulting. The main downside? You need a lot of money to access this option. Only some firms will take you as a client if you have $500,000 to invest—many require that you have $1 million or more.

Investment counsel firms are known for rigorous investment processes provided by a team of exceptionally well-qualified professionals. Typically you meet with an account representative holding the well-regarded chartered financial analyst (CFA) designation. Compared to most financial professionals “they have far more in-depth training in portfolio analysis and portfolio construction,” says Rodgers. That person thoroughly examines your financial situation, needs and risk tolerance, and then helps set your asset allocation, all of which is documented in an Investment Policy Statement (IPS). The money is then turned over to investment professionals working in the background who invest the money according to the direction in the IPS.

Fees are typically 1% to 1.5%, roughly comparable to rates charged by full-service brokers for stock and bond portfolios of a similar size, but cheaper than what you will pay for mutual funds through an adviser.

Despite their investment prowess, these low-key firms aren’t well-known. While many of the largest firms are divisions of banks, their services are rarely described in ads. For a list of leading investment counsel firms, see the tables below. You can also find a more extensive listing of firms at the Portfolio Management Association of Canada website, portfoliomanagement.org.

Another option that makes sense for those with $500,000 or more is income properties. While they’re not for everyone and they can come with significant risks, you may be able to find higher yields than you can get with stocks and bonds.

The key is selectivity. You won’t get decent yields buying condos in Vancouver and Toronto, says Don Campbell, senior analyst and co-founder of the Real Estate Investment Network (REIN). Instead look for townhomes, semis, and multiplexes in small or medium-sized cities with strong income and population growth in centres like Barrie or Hamilton in Ontario; Maple Ridge or Abbotsford in B.C; Saskatoon, Saskatchewan; and Airdrie or Fort Saskatchewan in Alberta, he says.

In my view, prudent investors are best off considering an income property only after they’ve paid off the mortgage on their residence, and then should invest only part of their nest egg. Campbell says putting a third of your investable assets into real estate would be reasonable for many people. He adds that you can find good options in real estate if you start with an initial investment of $150,000 or $200,000. That can provide you with a 25% down payment on a property worth $600,000 to $800,000, with the rest covered by a mortgage.

If you search carefully, you should still be able to find a property which generates a “cash-on-cash” return of 7% or 8%, he says. The cash-on-cash return is the net annual cash flow from the property, net of all costs, including maintenance and mortgage payments, as a percentage of the down payment. While that’s significantly less than you could earn a few years ago when real estate was cheaper, it is much better than yields for reasonably conservative stock and bond investments.

Direct real estate investing won’t suit everyone. You need to be savvy and do your homework thoroughly. Campbell says it’s important to make sure that the property will make money for you based on net rental income alone: “Don’t count on capital appreciation.”

Maintenance costs, such as replacing the roof or furnace, tend to be higher than you’d think, and you always run the risk of having your cash flow disrupted by a problem tenant. You can also run into trouble if you take out a big mortgage and interest rates start to rise. For that reason, it’s a good idea to lock in your mortgage for five to seven years and assess what your payments would be if rates rose by a couple of percentage points at renewal. A good conservative strategy is to plan to pay off the rental mortgage entirely by the time you retire.

Another option that makes sense for those with $500,000 or more is income properties. While they’re not for everyone and they can come with significant risks, you may be able to find higher yields than you can get with stocks and bonds.

The key is selectivity. You won’t get decent yields buying condos in Vancouver and Toronto, says Don Campbell, senior analyst and co-founder of the Real Estate Investment Network (REIN). Instead look for townhomes, semis, and multiplexes in small or medium-sized cities with strong income and population growth in centres like Barrie or Hamilton in Ontario; Maple Ridge or Abbotsford in B.C; Saskatoon, Saskatchewan; and Airdrie or Fort Saskatchewan in Alberta, he says.

In my view, prudent investors are best off considering an income property only after they’ve paid off the mortgage on their residence, and then should invest only part of their nest egg. Campbell says putting a third of your investable assets into real estate would be reasonable for many people. He adds that you can find good options in real estate if you start with an initial investment of $150,000 or $200,000. That can provide you with a 25% down payment on a property worth $600,000 to $800,000, with the rest covered by a mortgage.

If you search carefully, you should still be able to find a property which generates a “cash-on-cash” return of 7% or 8%, he says. The cash-on-cash return is the net annual cash flow from the property, net of all costs, including maintenance and mortgage payments, as a percentage of the down payment. While that’s significantly less than you could earn a few years ago when real estate was cheaper, it is much better than yields for reasonably conservative stock and bond investments.

Direct real estate investing won’t suit everyone. You need to be savvy and do your homework thoroughly. Campbell says it’s important to make sure that the property will make money for you based on net rental income alone: “Don’t count on capital appreciation.”

Maintenance costs, such as replacing the roof or furnace, tend to be higher than you’d think, and you always run the risk of having your cash flow disrupted by a problem tenant. You can also run into trouble if you take out a big mortgage and interest rates start to rise. For that reason, it’s a good idea to lock in your mortgage for five to seven years and assess what your payments would be if rates rose by a couple of percentage points at renewal. A good conservative strategy is to plan to pay off the rental mortgage entirely by the time you retire.

Notes: The largest firms are ranked by assets under management, by order of size. One additional firm had sufficient assets to be included in the top 10 but asked not to be identified. Source of largest firms by assets is: Investor Economics, Winter 2015. Minimum account size and office locations were provided by each firm.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Prediction markets are booming, but critics warn they can resemble gambling. Here's what investors need to know before trying...

Markets keep climbing despite economic headwinds. Allan Small explains why AI is driving growth and how investors can benefit...

The right cash allocation depends on your goals and stage of life. Here's how to think about cash in...

Reitmans narrowed its quarterly loss and Empire raised its dividend, but investors sent Groupe Dynamite and Gildan shares sharply...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

Investors seeking cash flow from real assets and inflation resistance should consider these infrastructure ETFs.

Optimization culture says that every dollar must be maximized and every latte is a betrayal of your future self,...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.