Working their way back from debt

The Medinas lost everything in their native Uruguay before starting fresh in Canada. Now that they have healthy salaries, they want to pay their debts and start saving for retirement. But is it too late?

Advertisement

The Medinas lost everything in their native Uruguay before starting fresh in Canada. Now that they have healthy salaries, they want to pay their debts and start saving for retirement. But is it too late?

Last fall Rocco Medina had a financial epiphany. The 50-year-old software engineer was working at his new $80,000-a-year job in Montreal when he noticed some magazines lying on a desk. “I picked up MoneySense and read the Family Profile during my lunch break,” says Rocco. “I was shocked. The couple in the article seemed to have a lot of savings compared to my own situation. I thought, ‘Man, if these people are worried about their future, then my family and I are in trouble.’”

Rocco, his wife Catalina, and their three children—Peter, now 24, Salina, 18, and Paolo, 15—emigrated from Uruguay nine years ago with only $20,000 to their name. (We’ve changed names to protect privacy.) They decided to leave their native land after enduring two years of financial hardship. “In 2002, there was a huge economic crisis in Uruguay,” says Catalina, 47, an accountant. “The currency lost over one-third of its value overnight and it was catastrophic for us. We lost all our savings.”

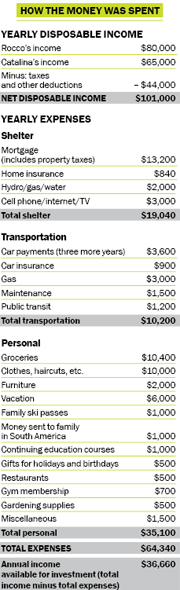

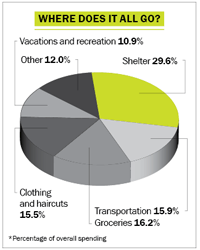

Today the Medinas are slowly rebuilding their lives. They became Canadian citizens five years ago and bought a three-bedroom home in a middle-class suburb of Montreal. After struggling with several low-paying, dead-end jobs the family now has an annual household income of $145,000 and an annual surplus of about $36,000 after their taxes and monthly expenses have been looked after. That’s the good news.

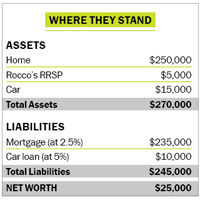

Unfortunately, they have virtually no savings and their assets are minuscule. They have a modest $250,000 home with a mortgage of $235,000 at 2.5%. Their RRSPs amount to just $5,000, and they need to pay back $11,000 they borrowed in 2009 through the RRSP Home Buyers’ Plan. The family shares a Toyota Corolla worth $15,000 and still has $10,000 left on the car loan. All told, their net worth is just $25,000. “It’s embarrassing,” says Rocco.

The Medinas have three key goals. The first is to pay off their mortgage before Rocco is 65. The couple would also like to save enough money to give them an after-tax retirement income of $40,000. “I have a small $300 a month pension that will come from Uruguay when I’m 65, but nothing more than that,” says Rocco.

Finally, they want to help Salina and Paolo pay for four years of post-secondary education. Peter graduated last year and the couple is thankful he has found a job he loves in video game design. “He’s making $47,000 a year and is on his own now,” says Rocco. “He loves his job and leads an active social life. We’re so happy for him.” The Medinas want to provide an eduction for their other two children to help them get good jobs, too.

While they have clear goals, the Medinas have no idea how to achieve them. “We came to Canada because we wanted to start fresh,” says Rocco. “We knew it had a solid economy with a society that reflected our values. What we need now is a plan.”

The Medinas were raised in middle-class families in Uruguay, and both attended university. They married in 1986. “From the start, I loved everything about Catalina,” says Rocco. “She’s smart, beautiful and very funny. Who could ask for more?”

University is free in Uruguay, but it’s extremely competitive. “It’s easy to get in, but staying in is another matter,” says Rocco. “With a starting class of 500 kids in my engineering program, only 40 made it to graduation. The filtering process is insane.”

The Medinas settled in Montevideo, Uruguay’s capital, where their children were born. Rocco and Catalina had well-paid jobs, and in 1995 bought a townhouse for $80,000. Their only savings strategy was to pay down the mortgage, and when the 2002 banking crisis shocked the country their home equity evaporated. “The interest rate rose to 18% on the $45,000 mortgage,” says Rocco. “The mortgage was in U.S. dollars, but my salary was paid in pesos, which were worth next to nothing.” There was a run on the banks from people desperate to withdraw their money.

“Both Catalina and I were eventually laid off from our jobs because our employers could no longer pay our salaries,” says Rocco, who had worked with the same engineering firm for 17 years. “Our debt ballooned and our household income went to zero. I was 40 and we had three small kids. We decided to leave.”

The Medinas tried to emigrate to Australia but were turned down. Their second choice was Canada, and they were accepted in 2004. Before they left, their house in Uruguay was auctioned off for a paltry $28,000. That money helped them get settled in Montreal. “The first six months were really scary,” says Catalina. “We lived on the little bit of savings we had.”

There were other challenges, too. “We really knew nothing about Montreal, except that one of its main languages was French,” says Rocco. “We could speak Italian and Spanish, so we figured it would be easy for the whole family to adapt, but the accents were so tough!”

Getting good jobs in Canada also proved difficult. “When we arrived it was hard to find work at the level we were used to back home,” says Rocco. “Catalina initially found work at a local bakery, while my first job was working at a factory installing components in heavy machinery. It was depressing work.”

Rocco and Catalina slowly worked their way back up the salary scale. By 2009 they were even able to borrow some money from Rocco’s RRSP and put $20,000 down on a three-bedroom home in a middle-class suburb. “It’s just a modest little house but we love it,” says Rocco.

The family loves to swim, sail and ski. They also enjoy an active social life with the local South American social club. “We thought we would hate winter, but now we can’t get enough of the snow,” says Rocco. “It just goes to show, you never know what life has in store for you, and sometimes the surprises can be wonderful.”

The Medinas are grateful for how far they have come since arriving in Canada with almost nothing. But they feel they’re coming up short compared with their Montreal friends. “They have paid off their homes already and saved thousands for retirement,” says Catalina. “Have we been left behind?”

That MoneySense article spurred the Medinas to realize they need to make some changes if they’re going to enjoy a comfortable retirement. “That’s fantastic,” says Annie Kvick, a fee-only planner with Money Coaches Canada in North Vancouver. “It’s never too late to start saving for retirement.”

Al Feth, a fee-only financial planner in Waterloo, Ont., agrees. “The Medinas went through a true financial disaster, and they certainly had a difficult few years,” he says. “But they’ve proven themselves to be truly self-reliant. Now that they have $36,000 of income available for investing, they can accomplish a lot in a few short years.” Here’s what they need to do.

Start an RESP for Paolo. The Medinas want to give $6,000 a year to each of their two youngest children to help fund their post-secondary education. They should start by immediately opening a Registered Education Savings Plan (RESP) for Paolo.

When you contribute to an RESP, you’re eligible for a 20% top-up in the form of the Canada Education Savings Grant (CESG). But special rules apply to accounts opened when a child reaches the mid-teens, Kvick explains. “The Medinas need to start this year. The rule is you have to put in a minimum of $2,000 by the end of the calendar year your child turns 15 or you’re not eligible for the CESG at age 16 and 17.”

Kvick says if the couple makes RESP contributions of at least $5,000 in 2013 and in each of the next two years, they will get $1,000 in CESG annually. “That’s $3,000 in free money.” At the end of those three years they will have at least $18,000 in the RESP, plus whatever return they earn on investments. That won’t be enough to fund Paolo’s entire education, but it’s a good start.

Kvick says if the couple makes RESP contributions of at least $5,000 in 2013 and in each of the next two years, they will get $1,000 in CESG annually. “That’s $3,000 in free money.” At the end of those three years they will have at least $18,000 in the RESP, plus whatever return they earn on investments. That won’t be enough to fund Paolo’s entire education, but it’s a good start.

Salina no longer qualifies for grant money, so there is no point opening an RESP for her. The Medinas should simply give her the $6,000 annually for the next four years to help finance her education. Some of this could be tax-sheltered in a TFSA.

Pay off their debt. This year the couple should pay off their $11,000 RRSP Home Buyers’ Plan loan as well as the $10,000 remaining on their car loan. “That will save them $3,600 a year in car payments, bringing the amount they have available for investing to $40,000 going forward,” says Feth.

Starting next year, the Medinas should also put an extra $10,000 towards their mortgage annually. “If they do this,” says Barb Garbens, a fee-only financial planner in Toronto, “their house will be paid off by 2026—just before retirement.”

Use Tax-Free Savings Accounts. The couple should start using TFSAs—not RRSPs—for retirement savings. When you draw money from an RRSP in retirement you need to claim it as income, but that’s not true of TFSA withdrawals. This flexibility will help keep the Medinas’ annual retirement income low enough to qualify for income-tested benefits such as the Guaranteed Income Supplement (GIS). It will also help them avoid OAS clawbacks.

Beginning in 2014, the Medinas should contribute about $11,000 each to their TFSAs until they are maxed out by 2017 (after which they would put in the annual $5,500 each).

Commit to a simple investment strategy. The Medinas are novice investors who don’t have the time or inclination to manage their money. They are also starting with a modest sum, so they’re not likely to find an adviser who is willing to help them.

That’s why they need a hassle-free strategy that will give them the broad diversification and investment returns they need to retire comfortably.

An ideal solution would be to open an account with ING Direct (ingdirect.ca) and use their Streetwise Portfolios. These one-stop Couch Potato portfolios are well-suited to first-time investors like the Medinas. Although the fees are relatively high for index funds (1.07%), there are no account minimums, no other fees or commissions, no need to rebalance, and no need to work with a discount brokerage.

The Streetwise Portfolios are available in four versions ranging from 25% to 100% equities. For their TFSAs, the Medinas should use the Streetwise Balanced Portfolio, which invests 40% in Canadian bonds, 20% in Canadian stocks, 20% in U.S. stocks and 20% in international stocks. This mix is conservative enough to use even in late retirement, but they can dial down risk by adding GICs as they get older.

Open a non-registered account in 2018. In four years the Medinas will be largely done paying for their children’s education. Then they could save more money, even after maxing out annual TFSA contributions until age 65. They should keep paying down an extra $10,000 a year on the mortgage until it’s gone. The remaining $20,000 should be put into non-registered accounts and invested like their TFSAs. (By now they’ll need an adviser to help.)

If they follow this plan, they will have over $400,000 in TFSAs and other investments by 65, assuming a 5% annual return. Add in government benefits and they should be fine. “With their work experience, I estimate they will receive a combined $1,000 a month from CPP, a combined $700 a month from OAS and $300 a month from Rocco’s Uruguay pension,” says Kvick. “Add in a combined $8,400 a year from the Guaranteed Income Supplement (GIS) and their annual retirement income will be $32,400. If they need a few thousand dollars more, they can draw from their savings with no fear of losing their GIS. Because they will have a paid-off house and very modest expenses, life will be just fine.”

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Why and how ETF closures happen, which warning signs to watch for, and what it means if a fund...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Sponsored By

Equifax

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Bonds are considered safer than stocks, but higher interest rates can still lead to losses. Here's what investors need...

Incorporating can eliminate the need to pay CPP contributions if you are self-employed but there are trade-offs that should...