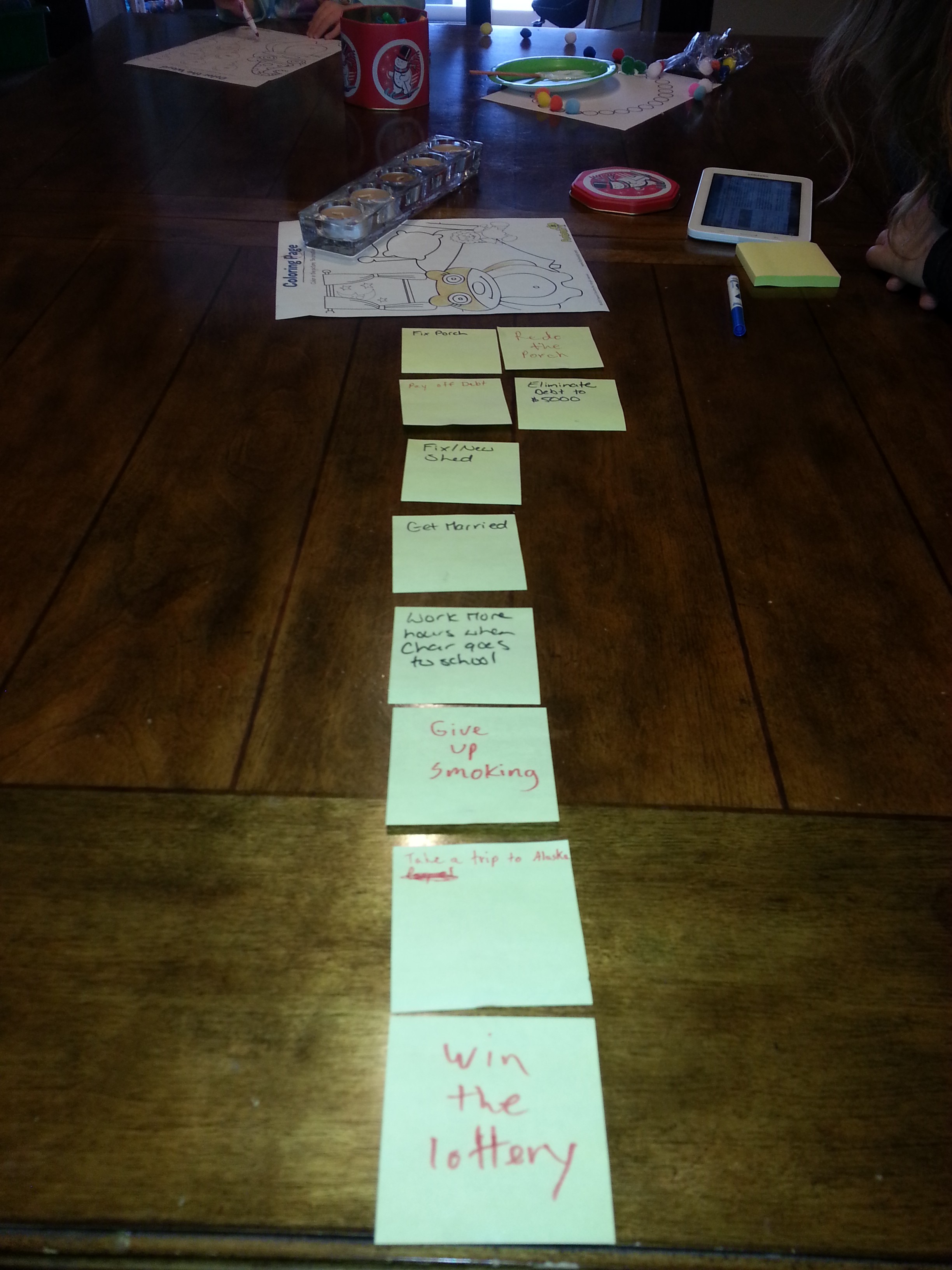

What are our money goals and can we reach them?

Shannon and Marcin take on their first Money Fit challenge

Advertisement

Shannon and Marcin take on their first Money Fit challenge

Embark on your own financial makeover! It’s not as hard as it sounds. Join the Money Fit Club to curb spending, boost your earnings, lower your taxes and more!

Learn to tone your money muscles all year long with our interactive calendar and sign up for our weekly newsletter for advice straight to your inbox.

Embark on your own financial makeover! It’s not as hard as it sounds. Join the Money Fit Club to curb spending, boost your earnings, lower your taxes and more!

Learn to tone your money muscles all year long with our interactive calendar and sign up for our weekly newsletter for advice straight to your inbox.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Experts say the best way to prepare for a single-income household is to test your budget first. Here's how...

Optimization culture says that every dollar must be maximized and every latte is a betrayal of your future self,...

Placing a few bets during the World Cup may feel low-stakes, but experts say it’s easy to lose track...

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

If it feels impossible to get ahead, you’re not imagining it. Here’s how inequality and policy choices are...

Find the 2026 Canadian federal and provincial tax brackets for 2025 income. Learn how marginal tax rates work, estimate...

The first home savings account was created to help you save more money for a home purchase. Here’s how...

Everyday costs in Canada keep rising even as inflation cools. Here are practical, lesser-known money-saving hacks to stretch your...

Moving home can boost savings—but it comes with financial, emotional, and lifestyle costs. Here’s how to decide if it’s...

Automating bills and savings reduces stress, prevents late fees, and helps you stay on track with your financial goals.