Am I on track to retire in 10 years?

Are Shannon and Hector's home equity savings enough?

Advertisement

Are Shannon and Hector's home equity savings enough?

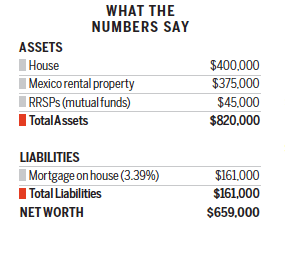

Shannon Jimenez, 47, lives in Chilliwack, B.C. with her husband Hector, 55. She’s a part-time customer service rep while Hector is a manager. “We’ve spent the last 25 years building up the equity in our home and in our Mexican rental property so savings are slim,” says Shannon. Right now, the couple has $45,000 in RRSPs earning 3.5% annually after fees. Neither has an employer pension but they are saving $1,000 a month from their $95,000 household income (which includes $10,000 in rental income). They also put $1,400 per month towards their mortgage—an amount that will be reduced to $700 in two years, allowing them to increase their savings to $1,700 per month for the next eight years. “We hope that by beefing up our savings in two years we can retire in 10 years on $40,000 net per year,” says Shannon.

Shannon Jimenez, 47, lives in Chilliwack, B.C. with her husband Hector, 55. She’s a part-time customer service rep while Hector is a manager. “We’ve spent the last 25 years building up the equity in our home and in our Mexican rental property so savings are slim,” says Shannon. Right now, the couple has $45,000 in RRSPs earning 3.5% annually after fees. Neither has an employer pension but they are saving $1,000 a month from their $95,000 household income (which includes $10,000 in rental income). They also put $1,400 per month towards their mortgage—an amount that will be reduced to $700 in two years, allowing them to increase their savings to $1,700 per month for the next eight years. “We hope that by beefing up our savings in two years we can retire in 10 years on $40,000 net per year,” says Shannon.

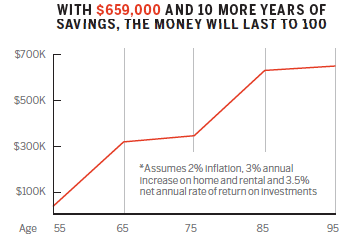

Janet Gray of Money Coaches Canada says the couple is on track to retire in 10 years, but only if they sell their Mexico rental property when

Hector reaches age 75. “They should watch the real estate market for the best time to sell,” says Gray. In two years, they should use the extra $700 they free up from lower mortgage payments to contribute $350 each month to each of their TFSAs. “The $1,000 per month they are currently saving should continue to go to the mutual funds in their RRSPs,” says Gray. If they stick to the $700 per month mortgage on their principal residence, the debt will be paid off in 15 years. “If Shannon and Hector retire in 10 years, and Shannon takes CPP at age 60, they’ll have annual income of $43,000, more than enough for a comfortable retirement.”

Janet Gray of Money Coaches Canada says the couple is on track to retire in 10 years, but only if they sell their Mexico rental property when

Hector reaches age 75. “They should watch the real estate market for the best time to sell,” says Gray. In two years, they should use the extra $700 they free up from lower mortgage payments to contribute $350 each month to each of their TFSAs. “The $1,000 per month they are currently saving should continue to go to the mutual funds in their RRSPs,” says Gray. If they stick to the $700 per month mortgage on their principal residence, the debt will be paid off in 15 years. “If Shannon and Hector retire in 10 years, and Shannon takes CPP at age 60, they’ll have annual income of $43,000, more than enough for a comfortable retirement.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

Created By

Ratehub

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

If you’re worried about a recession in Canada, you’re not alone. Here’s what to expect and how you can...

Canadians accustomed to annual tax refunds may be surprised to owe tax in retirement and have government benefits clawed...

Learn about Canada’s carbon tax, launched in 2019 and ended in 2025.