How to establish a scholarship fund

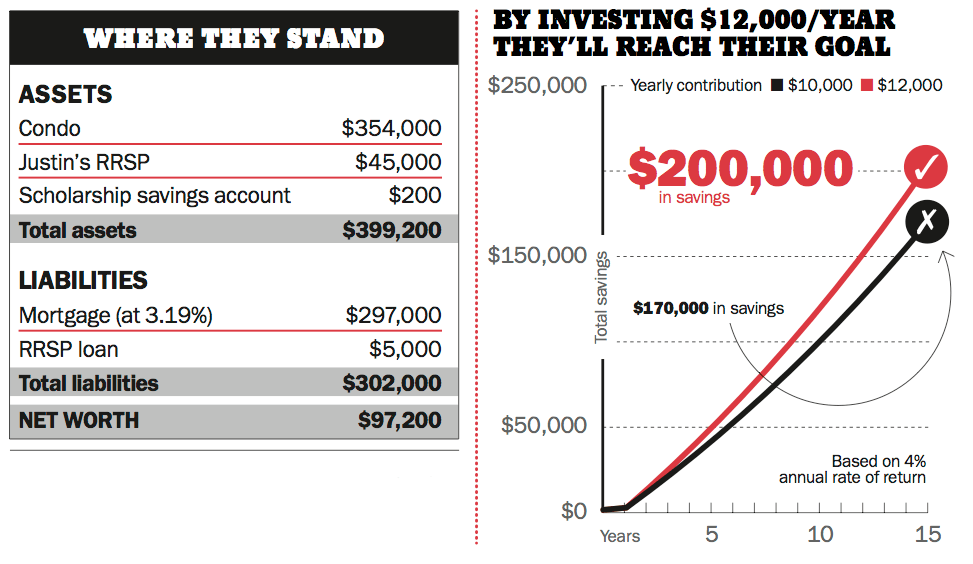

Can this couple make their dream of creating a $200,000 endowment fund a reality?

Advertisement

Can this couple make their dream of creating a $200,000 endowment fund a reality?

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Prediction markets are booming, but critics warn they can resemble gambling. Here's what investors need to know before trying...

Markets keep climbing despite economic headwinds. Allan Small explains why AI is driving growth and how investors can benefit...

The right cash allocation depends on your goals and stage of life. Here's how to think about cash in...

Reitmans narrowed its quarterly loss and Empire raised its dividend, but investors sent Groupe Dynamite and Gildan shares sharply...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

Investors seeking cash flow from real assets and inflation resistance should consider these infrastructure ETFs.

Optimization culture says that every dollar must be maximized and every latte is a betrayal of your future self,...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.