Lots of debt, no financial plan

Randy and Gabriel have three properties, lots of debt and no plan. Can they build a nest egg together while maintaining their financial independence?

Advertisement

Randy and Gabriel have three properties, lots of debt and no plan. Can they build a nest egg together while maintaining their financial independence?

Not helping matters is the fact that Gabriel and Randy are completely at odds over what to do with two investment properties that are draining their bank accounts. In addition to their $750,000 townhouse (and its $564,000 mortgage), Gabriel stills owns and now rents out a condo he purchased three years ago. He also has a half-interest in a rental home in Kitchener that he inherited last year when his father died. While the condo is worth $500,000, it still has a $316,000 mortgage and has become a financial handicap.

“Even though I pride myself on my math skills, I discovered I was losing money on my rental condo—about $200 a month,” says Gabriel. “I’m beginning to question whether the condo is worth keeping. We had romanticized the idea of having an executive suite we could manage in the future but the costs are driving me nuts. Real estate investing is just proving to be a better idea on paper than in real life for me.”

Gabriel is also questioning what to do with his half-interest in the $400,000 Kitchener house and its remaining $75,000 mortgage. His sister, who owns the other half, plans to live in it until next fall, after which he thinks the best thing to do is just unload it rather than keep it as a rental. “The house needs a lot of work done to it,” he says. “My share of the renos is $7,500. My plan is to sell the house, take my profit and put it towards savings.”

Randy, however, sees things differently. “I love the idea of real estate investing,” he says. “It’s an investment that’s easy to understand and always pays off in the long-term.” His dad, a small businessman, made some very successful investments in real estate, he points out. All the same, he’s sensitive to the fact that Gabriel is wary about a possible downturn in Toronto’s condo market. “I understand Gabriel’s concerns, but when he wants to retire, we can just sell the condo and pocket a huge chunk of money. That’s an option too,” Randy says.

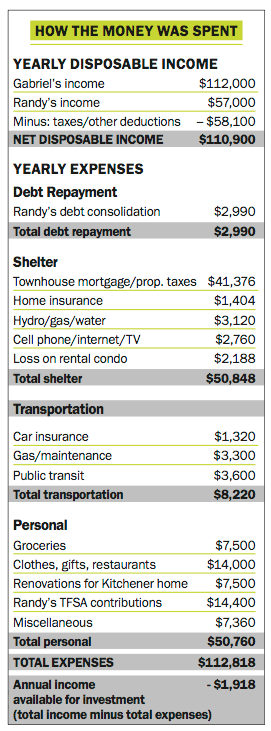

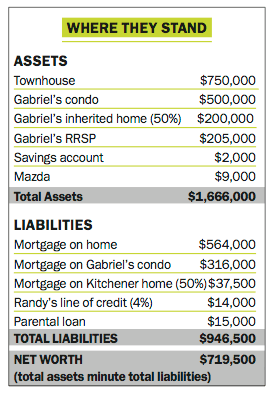

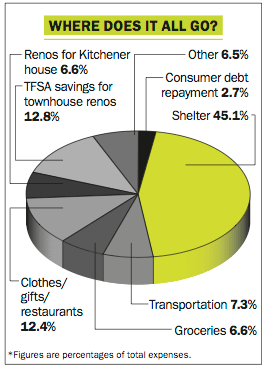

A closer examination of the couple’s net worth and annual expenses is eye-opening. Together, they have $946,500 in liabilities and the expenses associated with carrying all of their real estate is putting them in the hole by $1,918 a year.

The couple’s contrasting opinions on how to get their financial house in order spring from their very different attitudes about money management. From the outset of their relationship, says Gabriel, “I could see Randy was more adventurous with his money. I’m the saver and do all of my own investing.” In fact, he adds, both of them immediately noticed differences in their whole approach to life from the first moment they started dating seven years ago.

Randy, for instance, eschewed higher education to focus on his musical ambitions. Since high school, he’s been writing songs and after graduating in 2000, he started writing and recording. “I love what I do,” says Randy. “It doesn’t feel like work.”

Gabriel chose a different path. After finishing high school, he completed an undergraduate degree in history. He then received his masters degree in 1995, but later dropped out of a PhD program when he realized that academic jobs were tough to get. “I started working in web development and production management. I had a knack for it and the pay was fantastic.”

The financial difficulties Randy and Gabriel find themselves in today, however, have been a major wake-up call for the couple. They are now united in wanting to figure out the right financial plan to move forward with together.

Unfortunately, it won’t be straightforward. Planning will be complicated because the couple wants to keep most of their finances separate. Gabriel is still feeling financially stung from a previous relationship and he’s vowed to avoid similar mistakes in his new partnership with Randy. “Because I’m 12 years older I’ve accumulated substantial assets, while Randy has focused on building his musical career—requiring him to take on some debt,” says Gabriel. “So we’ve signed a pre-nup agreement but we’re both on title for the townhouse.”

In addition to his two rental properties, Gabriel is fortunate to be enrolled in his employer’s defined benefit pension plan and also has $205,000 in RRSP money, which makes up the bulk of the couple’s liquid assets. He’s managed his RRSP himself for several years by investing in the MoneySense Couch Potato Portfolio. “I’m very happy with the results,” Gabriel says. Randy, on the other hand, owes $14,000 on a line of credit and has practically no savings.

Eventually, the couple would like to merge their finances together, but for now the arrangement gives both of them peace of mind. “I never want Gabriel to feel I’m in this relationship for his money,” says Randy.

The couple’s age difference offers yet another hiccup when it comes to long-term planning. At age 44, Gabriel is now very focused on wanting to retire by 55 with a paid-off house and enough savings to lead a comfortable middle-class lifestyle. Randy, however, is just at the outset of his career and, unlike Gabriel, envisions working indefinitely as a musician.

Not helping matters is the fact that Gabriel and Randy are completely at odds over what to do with two investment properties that are draining their bank accounts. In addition to their $750,000 townhouse (and its $564,000 mortgage), Gabriel stills owns and now rents out a condo he purchased three years ago. He also has a half-interest in a rental home in Kitchener that he inherited last year when his father died. While the condo is worth $500,000, it still has a $316,000 mortgage and has become a financial handicap.

“Even though I pride myself on my math skills, I discovered I was losing money on my rental condo—about $200 a month,” says Gabriel. “I’m beginning to question whether the condo is worth keeping. We had romanticized the idea of having an executive suite we could manage in the future but the costs are driving me nuts. Real estate investing is just proving to be a better idea on paper than in real life for me.”

Gabriel is also questioning what to do with his half-interest in the $400,000 Kitchener house and its remaining $75,000 mortgage. His sister, who owns the other half, plans to live in it until next fall, after which he thinks the best thing to do is just unload it rather than keep it as a rental. “The house needs a lot of work done to it,” he says. “My share of the renos is $7,500. My plan is to sell the house, take my profit and put it towards savings.”

Randy, however, sees things differently. “I love the idea of real estate investing,” he says. “It’s an investment that’s easy to understand and always pays off in the long-term.” His dad, a small businessman, made some very successful investments in real estate, he points out. All the same, he’s sensitive to the fact that Gabriel is wary about a possible downturn in Toronto’s condo market. “I understand Gabriel’s concerns, but when he wants to retire, we can just sell the condo and pocket a huge chunk of money. That’s an option too,” Randy says.

A closer examination of the couple’s net worth and annual expenses is eye-opening. Together, they have $946,500 in liabilities and the expenses associated with carrying all of their real estate is putting them in the hole by $1,918 a year.

The couple’s contrasting opinions on how to get their financial house in order spring from their very different attitudes about money management. From the outset of their relationship, says Gabriel, “I could see Randy was more adventurous with his money. I’m the saver and do all of my own investing.” In fact, he adds, both of them immediately noticed differences in their whole approach to life from the first moment they started dating seven years ago.

Randy, for instance, eschewed higher education to focus on his musical ambitions. Since high school, he’s been writing songs and after graduating in 2000, he started writing and recording. “I love what I do,” says Randy. “It doesn’t feel like work.”

Gabriel chose a different path. After finishing high school, he completed an undergraduate degree in history. He then received his masters degree in 1995, but later dropped out of a PhD program when he realized that academic jobs were tough to get. “I started working in web development and production management. I had a knack for it and the pay was fantastic.”

The financial difficulties Randy and Gabriel find themselves in today, however, have been a major wake-up call for the couple. They are now united in wanting to figure out the right financial plan to move forward with together.

Unfortunately, it won’t be straightforward. Planning will be complicated because the couple wants to keep most of their finances separate. Gabriel is still feeling financially stung from a previous relationship and he’s vowed to avoid similar mistakes in his new partnership with Randy. “Because I’m 12 years older I’ve accumulated substantial assets, while Randy has focused on building his musical career—requiring him to take on some debt,” says Gabriel. “So we’ve signed a pre-nup agreement but we’re both on title for the townhouse.”

In addition to his two rental properties, Gabriel is fortunate to be enrolled in his employer’s defined benefit pension plan and also has $205,000 in RRSP money, which makes up the bulk of the couple’s liquid assets. He’s managed his RRSP himself for several years by investing in the MoneySense Couch Potato Portfolio. “I’m very happy with the results,” Gabriel says. Randy, on the other hand, owes $14,000 on a line of credit and has practically no savings.

Eventually, the couple would like to merge their finances together, but for now the arrangement gives both of them peace of mind. “I never want Gabriel to feel I’m in this relationship for his money,” says Randy.

The couple’s age difference offers yet another hiccup when it comes to long-term planning. At age 44, Gabriel is now very focused on wanting to retire by 55 with a paid-off house and enough savings to lead a comfortable middle-class lifestyle. Randy, however, is just at the outset of his career and, unlike Gabriel, envisions working indefinitely as a musician. On a positive note, the couple is aware they’re not taking advantage of tax-sheltering tools that will enhance their rate of savings. Randy, for instance, has just started putting away $1,200 a month in a TFSA to go toward the completion of townhouse renos within the next year. Likewise, Gabriel wants to start a TFSA as well and still has $100,000 in unused RRSP contribution room, while Randy has $20,000. “We know we need to start using TFSAs and RRSPs more effectively but don’t know how to structure it best for our particular situation,” says Gabriel.

Provided they can get these financial problems sorted out, the couple otherwise feels the sky’s the limit when it comes to their future together. “We complement each other,” says Randy. “We just need to work out the details.”

On a positive note, the couple is aware they’re not taking advantage of tax-sheltering tools that will enhance their rate of savings. Randy, for instance, has just started putting away $1,200 a month in a TFSA to go toward the completion of townhouse renos within the next year. Likewise, Gabriel wants to start a TFSA as well and still has $100,000 in unused RRSP contribution room, while Randy has $20,000. “We know we need to start using TFSAs and RRSPs more effectively but don’t know how to structure it best for our particular situation,” says Gabriel.

Provided they can get these financial problems sorted out, the couple otherwise feels the sky’s the limit when it comes to their future together. “We complement each other,” says Randy. “We just need to work out the details.”

That strategy will provide Gabriel with a $23,000 tax refund for 2014, and a $14,000 refund for 2015. “From the $23,000 tax refund, $14,000 could be used for their townhouse renos and the remaining $9,000 can be ‘loaned’ to Randy to contribute to his RRSP, generating a $3,000 refund,” says Dekanic. “If their relationship remains solid, then Gabriel can forgive this loan in the future or in his will. If it dissolves, Gabriel can be repaid through the proceeds of their townhouse sale or from Randy’s TFSAs.” The lending of funds for Randy’s RRSP should continue for the second year as well.

Top up the TFSA. With the $160,000 he expects to get from the sale of his dad’s Kitchener home, Gabriel should make use of all of his unused TFSA contribution room—$36,500 as of Jan. 1, 2015. That still leaves him with $193,500 in cash: $123,500 left over from the Kitchener sale and $70,000 from the condo sale.

If Gabriel wants to pay down the mortgage on their principal residence quicker, he could make an annual lump sum prepayment of $85,000 for each of 2015 and 2016, leaving the remaining $23,500 in an emergency cash fund. “If they maintain the same payment structure after this, their townhouse would be paid off in about 10 years from the renewal date,” says Dekanic.

At age 53, Gabriel should have an actuary run the numbers on what company pension payments he can expect to receive if he retires at 55 and takes his CPP at 60. With a 5% gross rate of return on his investments, he should have more than $500,000 in his nest egg by age 55. “With a paid-off townhouse, a modest company pension and CPP at age 60, Gabriel should easily be able to fund the $20,000 or so he feels he’ll need annually (over and above his pension payments) to live a comfortable life,” says Campbell. “Add to that Randy earning more income in the future—and maybe even a modest income from some part-time work from Gabriel—and the couple will be just fine.”

That strategy will provide Gabriel with a $23,000 tax refund for 2014, and a $14,000 refund for 2015. “From the $23,000 tax refund, $14,000 could be used for their townhouse renos and the remaining $9,000 can be ‘loaned’ to Randy to contribute to his RRSP, generating a $3,000 refund,” says Dekanic. “If their relationship remains solid, then Gabriel can forgive this loan in the future or in his will. If it dissolves, Gabriel can be repaid through the proceeds of their townhouse sale or from Randy’s TFSAs.” The lending of funds for Randy’s RRSP should continue for the second year as well.

Top up the TFSA. With the $160,000 he expects to get from the sale of his dad’s Kitchener home, Gabriel should make use of all of his unused TFSA contribution room—$36,500 as of Jan. 1, 2015. That still leaves him with $193,500 in cash: $123,500 left over from the Kitchener sale and $70,000 from the condo sale.

If Gabriel wants to pay down the mortgage on their principal residence quicker, he could make an annual lump sum prepayment of $85,000 for each of 2015 and 2016, leaving the remaining $23,500 in an emergency cash fund. “If they maintain the same payment structure after this, their townhouse would be paid off in about 10 years from the renewal date,” says Dekanic.

At age 53, Gabriel should have an actuary run the numbers on what company pension payments he can expect to receive if he retires at 55 and takes his CPP at 60. With a 5% gross rate of return on his investments, he should have more than $500,000 in his nest egg by age 55. “With a paid-off townhouse, a modest company pension and CPP at age 60, Gabriel should easily be able to fund the $20,000 or so he feels he’ll need annually (over and above his pension payments) to live a comfortable life,” says Campbell. “Add to that Randy earning more income in the future—and maybe even a modest income from some part-time work from Gabriel—and the couple will be just fine.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

More Canadians are turning to ChatGPT and other AI tools for money advice. Here's what to know about trust...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

Canadians may be tired of tipping culture, but newcomers are still trying to figure out the rules.

Financial advisors aren’t always necessary. Learn when you can DIY, when help adds value, and how to decide what’s...