Picking up the pieces: Retirement after divorce

Newly divorced Shauna needs to learn to live on less and rebuild her broken investment portfolio

Advertisement

Newly divorced Shauna needs to learn to live on less and rebuild her broken investment portfolio

Immediately downsizing from the 2,900 square foot ranch-style bungalow she once shared with her ex-husband to the smaller 1,400 square foot townhouse that she lives in today was a no-brainer. It’s worth $448,000 and with the money she made from the sale of her former marital home, she’s now completely mortgage free. “I plan to stay put for a while,” she says.

Not so great are Shauna’s excessive spending habits. Even after blowing through the $50,000 cash settlement from her divorce, she then went on to rack up nearly $44,000 in liabilities from loans and credit debt. “After the divorce, I overmedicated with buying furniture for the house,” she says. There was also the purchase of a brand new car, despite already owning a serviceable vehicle. “I spent way more than I should have. In hindsight I wish I had approached things slower.”

She now wants to get rid of her debt as quickly as possible but isn’t sure whether she should be prioritizing that over socking away money in her nest egg. “I don’t have much saved and I’m always torn between saving or paying down debt,” she says. “Which is best?” And what Shauna does have set aside for retirement is invested so poorly that it’s headache-inducing to even think about, particularly since she considers herself a conservative investor. “My accounts are full of crazy high-risk uranium and mining stocks that Dan bought for me while we were married. Some of these accounts have lost more than 70% of their value. Should I hold on? Or kiss it all good-bye and start over?”

Despite all the decisions—good and bad—that Shauna has made and despite all the questions about her finances that remain unanswered, she realizes it’s now time to create a budget and stick to it. “I know I spend too much but before I always felt it was okay because Dan made a lot of money and we had no kids.”

The one area Shauna won’t cut back on, however, is her charitable giving. Through her church, she sponsors seven children and that will remain a priority, she says. “I hope to meet each child I’ve sponsored at some point in my life. I’m ready to cut my budget in other areas to accommodate this.”

In fact, it was Shauna’s faith and involvement in her church that initially drew her to her ex-husband all those years ago. She was attracted to Dan, she says, mainly because they had the same religious beliefs and were part of the same congregation. The couple married in 1997 when Shauna was 25, and over the years Dan was always the breadwinner while she mostly worked part-time at odd jobs. During their marriage, whatever money the Rays had was invested either in their house, or in cyclical penny stocks that Dan was convinced would one day make them both rich. “He made most of the income so I let him invest it the way he wanted,” she says. “In hindsight, it was a disastrous thing to do but he really seemed to enjoy it more than I did.”

Thankfully, in the years preceding her divorce Shauna started pursuing full-time job opportunities for herself. “I never worked full-time until four years ago,” she says. “I took some accounting courses off and on during our marriage, and was lucky enough to get this payroll accounting job with a great company a couple of years before my marriage broke up.”

And with her new payroll coordinator job, Shauna is working to build a solid financial plan. Right now, she’s investing $2,500 a year in her company’s defined contribution pension plan, where her money is matched dollar for dollar by her employer. And despite her hesitation about saving versus paying down debt, she’s also contributing $20 biweekly towards the purchase of Canada Savings Bonds. “I’ve never really saved methodically,” she says. “I’m trying to change that now.”

Immediately downsizing from the 2,900 square foot ranch-style bungalow she once shared with her ex-husband to the smaller 1,400 square foot townhouse that she lives in today was a no-brainer. It’s worth $448,000 and with the money she made from the sale of her former marital home, she’s now completely mortgage free. “I plan to stay put for a while,” she says.

Not so great are Shauna’s excessive spending habits. Even after blowing through the $50,000 cash settlement from her divorce, she then went on to rack up nearly $44,000 in liabilities from loans and credit debt. “After the divorce, I overmedicated with buying furniture for the house,” she says. There was also the purchase of a brand new car, despite already owning a serviceable vehicle. “I spent way more than I should have. In hindsight I wish I had approached things slower.”

She now wants to get rid of her debt as quickly as possible but isn’t sure whether she should be prioritizing that over socking away money in her nest egg. “I don’t have much saved and I’m always torn between saving or paying down debt,” she says. “Which is best?” And what Shauna does have set aside for retirement is invested so poorly that it’s headache-inducing to even think about, particularly since she considers herself a conservative investor. “My accounts are full of crazy high-risk uranium and mining stocks that Dan bought for me while we were married. Some of these accounts have lost more than 70% of their value. Should I hold on? Or kiss it all good-bye and start over?”

Despite all the decisions—good and bad—that Shauna has made and despite all the questions about her finances that remain unanswered, she realizes it’s now time to create a budget and stick to it. “I know I spend too much but before I always felt it was okay because Dan made a lot of money and we had no kids.”

The one area Shauna won’t cut back on, however, is her charitable giving. Through her church, she sponsors seven children and that will remain a priority, she says. “I hope to meet each child I’ve sponsored at some point in my life. I’m ready to cut my budget in other areas to accommodate this.”

In fact, it was Shauna’s faith and involvement in her church that initially drew her to her ex-husband all those years ago. She was attracted to Dan, she says, mainly because they had the same religious beliefs and were part of the same congregation. The couple married in 1997 when Shauna was 25, and over the years Dan was always the breadwinner while she mostly worked part-time at odd jobs. During their marriage, whatever money the Rays had was invested either in their house, or in cyclical penny stocks that Dan was convinced would one day make them both rich. “He made most of the income so I let him invest it the way he wanted,” she says. “In hindsight, it was a disastrous thing to do but he really seemed to enjoy it more than I did.”

Thankfully, in the years preceding her divorce Shauna started pursuing full-time job opportunities for herself. “I never worked full-time until four years ago,” she says. “I took some accounting courses off and on during our marriage, and was lucky enough to get this payroll accounting job with a great company a couple of years before my marriage broke up.”

And with her new payroll coordinator job, Shauna is working to build a solid financial plan. Right now, she’s investing $2,500 a year in her company’s defined contribution pension plan, where her money is matched dollar for dollar by her employer. And despite her hesitation about saving versus paying down debt, she’s also contributing $20 biweekly towards the purchase of Canada Savings Bonds. “I’ve never really saved methodically,” she says. “I’m trying to change that now.”

Something else she’d like to accomplish is to learn a sensible approach to investing that will help grow her own personal portfolio. Recently, she picked a couple of mutual funds and says she’s happy with their performance—but also admits, “I’ve just been doing what I see others doing.” She knows the next step is to find an advisor she likes and to put together an investment plan—not to mention, deal with all the penny stocks in her various accounts—so that she can have a bright future. That’s proving to be challenging, however.

“I met with one advisor at a local financial institution but he never called me back,” Shauna says. But even if he had, she’s not certain she would have been able to determine if he had her best interests at heart. From her experience, advisors “will often say they’re not commission-based, but it’s hard to know whose rubbing whose back. I want to take control of my own finances and do what’s right for me and my future. I don’t want to squander this second chance.”

That includes investing in the right man this time around as well. “Dating in your 20s is so different from dating in your 40s,” Shauna says. “But I decided last fall that I did not want to date guys in their 40s with kids. No baby mama drama for me.” In fact, she’s been in a long-distance relationship with an American doctor 10 years her senior that she met just before Christmas at a religious conference in Washington. He’s divorced with no children, too.

Knowing she’d love to get another shot at marriage some day, Shauna wants to be smarter about her money now. “I need to protect my assets if I get involved in another committed relationship. I want to make the right choices so I don’t regret it later on.” That being said, she doesn’t want to get too far ahead of herself either. “I first want to have a concise plan for my own future. When I retire at 65, I’d like to do volunteer work full-time and give more to charity. To know that I’ve changed the lives of people in need is what really gives me true satisfaction in life.”

Something else she’d like to accomplish is to learn a sensible approach to investing that will help grow her own personal portfolio. Recently, she picked a couple of mutual funds and says she’s happy with their performance—but also admits, “I’ve just been doing what I see others doing.” She knows the next step is to find an advisor she likes and to put together an investment plan—not to mention, deal with all the penny stocks in her various accounts—so that she can have a bright future. That’s proving to be challenging, however.

“I met with one advisor at a local financial institution but he never called me back,” Shauna says. But even if he had, she’s not certain she would have been able to determine if he had her best interests at heart. From her experience, advisors “will often say they’re not commission-based, but it’s hard to know whose rubbing whose back. I want to take control of my own finances and do what’s right for me and my future. I don’t want to squander this second chance.”

That includes investing in the right man this time around as well. “Dating in your 20s is so different from dating in your 40s,” Shauna says. “But I decided last fall that I did not want to date guys in their 40s with kids. No baby mama drama for me.” In fact, she’s been in a long-distance relationship with an American doctor 10 years her senior that she met just before Christmas at a religious conference in Washington. He’s divorced with no children, too.

Knowing she’d love to get another shot at marriage some day, Shauna wants to be smarter about her money now. “I need to protect my assets if I get involved in another committed relationship. I want to make the right choices so I don’t regret it later on.” That being said, she doesn’t want to get too far ahead of herself either. “I first want to have a concise plan for my own future. When I retire at 65, I’d like to do volunteer work full-time and give more to charity. To know that I’ve changed the lives of people in need is what really gives me true satisfaction in life.”

Moreover, adds Vickie Campbell, a certified financial planner in Ottawa, “Shauna is confused over whether she should save or pay down the debt. She needs to prioritize.” Here’s what she should do.

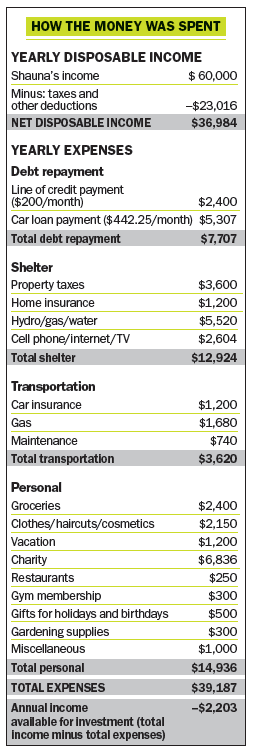

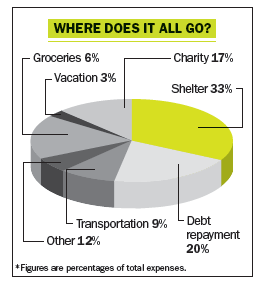

Draw up a budget. Shauna is spending $2,203 more annually than she’s earning. “She needs to track her spending to ensure she doesn’t spend more than she makes,” says Campbell. One of her two vehicles needs to go, which will reduce her car insurance. Modest reductions in her cosmetics and clothing expenses, coupled with putting an end to her biweekly Canada Savings Bond contributions, will help keep on her track too.

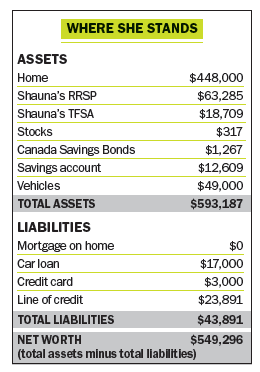

Pay down the debt. Shauna has funds available to pay off her debt in full. “She should take the money in her savings account, Canada Savings Bonds and TFSA—$32,585 in total—and put it towards her line of credit debt, credit card debt and car loan, leaving her with just $11,306 on the car loan,” says Campbell. And by selling her older car, she’ll bring her debt to zero.

Rebuild her savings. Once all of Shauna’s debt is paid off, the $7,707 that was going towards yearly debt repayment will be available for investing. “She should put this money into an RRSP annually,” says Campbell. “The tax refund she receives can be put into her TFSA to rebuild her savings.” With low housing costs and a keen eye on keeping her expenses down, Shauna should be able to save 20% of her net income annually.

Regarding her pension plan, adds Campbell, “she should make sure she is contributing the maximum so she receives the full matching contribution. This is free money waiting to be taken.”

Find a financial advisor. Both Van Nest and Campbell believe that Shauna’s investment holdings don’t reflect her personality and risk profile. They recommend she look for an advisor with a certified financial planner designation that she can work with on a long-term basis. Checking out moneysense.ca/planner will get her started.

“She should bite the bullet, sell all her high-risk stocks and replace them with a more conservative investment strategy,” says Campbell. “One option is the Mawer balanced fund, which she can contribute to monthly through a preauthorized payment plan through a discount brokerage account at her bank. This will keep her costs low and investment plan simple. Her new advisor will help her with this.” Van Nest agrees, adding, “this will eliminate the risk of loss that comes from stock-picking.”

Campbell also suggests Shauna track her net worth with her new advisor, and set short-term and long-term goals. “Watching her money grow every year will keep Shauna motivated to stay on plan.”

Protect her assets. “If Shauna finds herself in a serious relationship , she should consider a cohabitation or prenuptial agreement,” says Van Nest. The CRA defines a common-law relationship as 12 months of cohabitation, but Alberta law defines it as not less than three years. Regardless of the timeline, Van Nest says that as soon as Shauna enters into marriage or a shared living arrangement, she may want a lawyer to draw up a document to make it clear what would happen if a split were to occur. “This is the only way Shauna can legally protect her assets from a future partner,” says Van Nest.

Stay in the pension plan. “If Shauna’s retirement contributions and employer matching continue until age 65, she will have built up $473,000 assuming a 5% annual return and 2% annual pay increases,” says Van Nest. When CPP at 65 and Old Age Security at 67 are added, Shauna can anticipate an annual taxable income of about $36,000 in today’s dollars throughout her retirement for a modest standard of living. Add in the $300,000 or more she will have built up in her RRSP, and Shauna will be just fine.

Moreover, adds Vickie Campbell, a certified financial planner in Ottawa, “Shauna is confused over whether she should save or pay down the debt. She needs to prioritize.” Here’s what she should do.

Draw up a budget. Shauna is spending $2,203 more annually than she’s earning. “She needs to track her spending to ensure she doesn’t spend more than she makes,” says Campbell. One of her two vehicles needs to go, which will reduce her car insurance. Modest reductions in her cosmetics and clothing expenses, coupled with putting an end to her biweekly Canada Savings Bond contributions, will help keep on her track too.

Pay down the debt. Shauna has funds available to pay off her debt in full. “She should take the money in her savings account, Canada Savings Bonds and TFSA—$32,585 in total—and put it towards her line of credit debt, credit card debt and car loan, leaving her with just $11,306 on the car loan,” says Campbell. And by selling her older car, she’ll bring her debt to zero.

Rebuild her savings. Once all of Shauna’s debt is paid off, the $7,707 that was going towards yearly debt repayment will be available for investing. “She should put this money into an RRSP annually,” says Campbell. “The tax refund she receives can be put into her TFSA to rebuild her savings.” With low housing costs and a keen eye on keeping her expenses down, Shauna should be able to save 20% of her net income annually.

Regarding her pension plan, adds Campbell, “she should make sure she is contributing the maximum so she receives the full matching contribution. This is free money waiting to be taken.”

Find a financial advisor. Both Van Nest and Campbell believe that Shauna’s investment holdings don’t reflect her personality and risk profile. They recommend she look for an advisor with a certified financial planner designation that she can work with on a long-term basis. Checking out moneysense.ca/planner will get her started.

“She should bite the bullet, sell all her high-risk stocks and replace them with a more conservative investment strategy,” says Campbell. “One option is the Mawer balanced fund, which she can contribute to monthly through a preauthorized payment plan through a discount brokerage account at her bank. This will keep her costs low and investment plan simple. Her new advisor will help her with this.” Van Nest agrees, adding, “this will eliminate the risk of loss that comes from stock-picking.”

Campbell also suggests Shauna track her net worth with her new advisor, and set short-term and long-term goals. “Watching her money grow every year will keep Shauna motivated to stay on plan.”

Protect her assets. “If Shauna finds herself in a serious relationship , she should consider a cohabitation or prenuptial agreement,” says Van Nest. The CRA defines a common-law relationship as 12 months of cohabitation, but Alberta law defines it as not less than three years. Regardless of the timeline, Van Nest says that as soon as Shauna enters into marriage or a shared living arrangement, she may want a lawyer to draw up a document to make it clear what would happen if a split were to occur. “This is the only way Shauna can legally protect her assets from a future partner,” says Van Nest.

Stay in the pension plan. “If Shauna’s retirement contributions and employer matching continue until age 65, she will have built up $473,000 assuming a 5% annual return and 2% annual pay increases,” says Van Nest. When CPP at 65 and Old Age Security at 67 are added, Shauna can anticipate an annual taxable income of about $36,000 in today’s dollars throughout her retirement for a modest standard of living. Add in the $300,000 or more she will have built up in her RRSP, and Shauna will be just fine.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

More Canadians are turning to ChatGPT and other AI tools for money advice. Here's what to know about trust...

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.