Assuring income for an aging mom

How to generate the cash flow Gordon's mother needs.

Advertisement

How to generate the cash flow Gordon's mother needs.

The problem

The problemAfter his mother Elizabeth was diagnosed with dementia, Gordon Warburton became concerned her investment portfolio wouldn’t be able to generate the income she needs to pay for her care. The cost is $24,000 annually, or about 6% of the portfolio’s value. But the $125,000 she has in guaranteed investment certificates (GICs) and Canada Savings Bonds will have to be reinvested at today’s low rates when they mature. And Gordon knows if interest rates rise, the value of her two bond ETFs (currently $260,000) will fall. Only 5% of the portfolio is in equity ETFs, and Gordon wonders whether they’ll need to take a bit more risk to reach their goal.

Heather Holjevac, a senior wealth adviser with TriDelta Financial Partners of Oakville, Ont., says planners frequently face this dilemma. Previously, people in Elizabeth’s generation could get by on GICs, but today’s rates barely keep pace with inflation. The problem is exacerbated by the fact women live longer than men.

Holjevac recommends keeping most of the portfolio in a mix of cash, laddered GICs and bonds. TriDelta is wary of holding bond ETFs in a rising rate environment, so would advise holding the bonds directly. Holjevac suggests increasing the allocation of dividend-paying stocks and preferred shares.

The asset mix is conservative, but it falls in line with the Warburtons’ risk tolerance. The portfolio has an expected annual return of 3.3%, less than the 6% Gordon thought they needed. While Elizabeth will have to draw down some capital to cover expenses, she has more than enough money to last a lifetime.

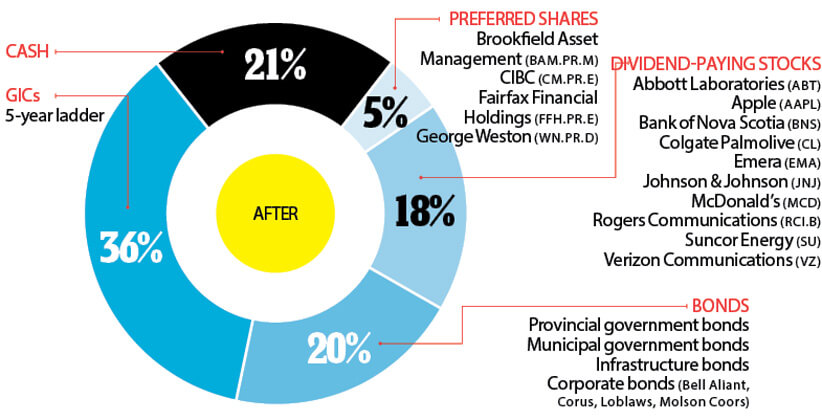

A third of Elizabeth’s portfolio remains in GICs. The current average GIC payout is 2.8%, but new issues are likely to pay 2%. A further 21% is in cash paying 1.5%, which can be reinvested in GICs if rates rise. And 20% is in bonds with coupons between 3% and 6.5%. (Because they trade at a premium they will suffer a loss when they mature). Holjevac has 5% in preferred shares yielding 5.4%. “Preferreds go in and out of favour but hold their value.” Large-cap North American dividend stocks make up the final 18%, with an average yield of 3.7%.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Find out which Canadian robo-advisors offer the lowest fees, helpful support, best returns, and most account types with the...

The first home savings account was created to help you save more money for a home purchase. Here’s how...

Both products promise upside participation with downside protection, but come with unique trade-offs and costs investors should be aware...

Your RRSP contribution limit comes from unused deduction room plus 18% of last year’s income. Use our RRSP calculator...

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...