Are you ready for the Hot Potato?

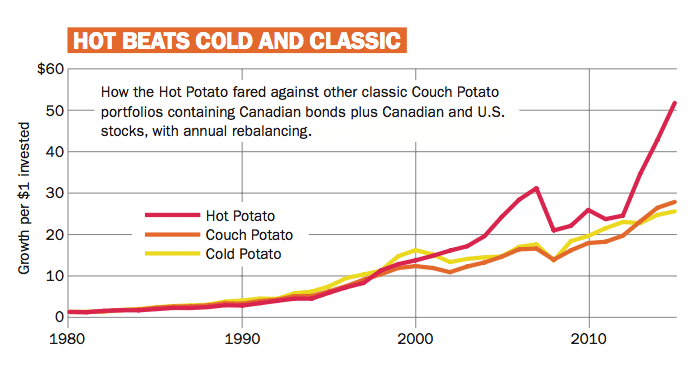

Love the steady returns of the classic Couch Potato strategy? This spicier version beat it by 6.7 percentage points annually. It’s hot stuff

Advertisement

Love the steady returns of the classic Couch Potato strategy? This spicier version beat it by 6.7 percentage points annually. It’s hot stuff

The Global Hot Potato portfolio, rebalanced monthly, gained an average of 16.7% per year from the start of 1981 to the end of 2015. It beat the classic Couch Potato by a whopping 6.7 percentage points annually.

While the global version of the Hot Potato was certainly more volatile than the Couch Potato, it came mostly from the sort of upside volatility that few investors complain about. In addition, it nimbly sidestepped several market crashes along the way. In fact, the largest drawdown for the monthly-balanced Global Hot Potato came after the Internet bubble popped in 2000, when it declined 21.4%. But it bounced back almost two years before the Global Couch Potato did, having fallen 29.2% during the same downturn.

The Global Couch Potato drew its biggest loss during the 2008 collapse (31.1%) and didn’t recover until 2011. Its spicier sibling fared better because it was invested in bonds for a good part of that period: It fell only 10% from its 2007 high to its 2008 low, and had recovered fully by the summer of 2009.

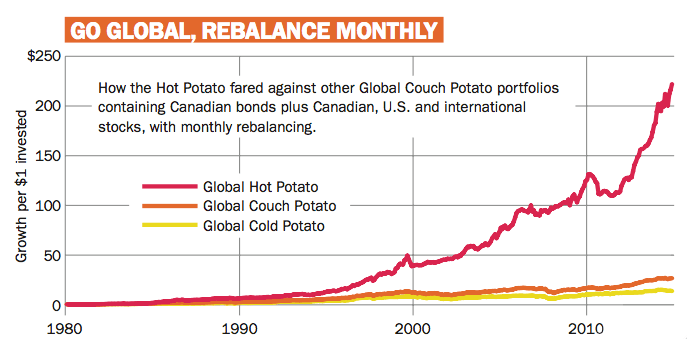

Once again contrarians fared poorly. The Global Cold Potato Portfolio is moved monthly into the worst performing asset class of the prior year. By doing so, it gained an average of 7.9% annually and trailed the Global Couch Potato by 2.1 percentage points per year. The monthly return history of all three global potato variants is shown in the charts on the opposite page.

The Global Hot Potato portfolio, rebalanced monthly, gained an average of 16.7% per year from the start of 1981 to the end of 2015. It beat the classic Couch Potato by a whopping 6.7 percentage points annually.

While the global version of the Hot Potato was certainly more volatile than the Couch Potato, it came mostly from the sort of upside volatility that few investors complain about. In addition, it nimbly sidestepped several market crashes along the way. In fact, the largest drawdown for the monthly-balanced Global Hot Potato came after the Internet bubble popped in 2000, when it declined 21.4%. But it bounced back almost two years before the Global Couch Potato did, having fallen 29.2% during the same downturn.

The Global Couch Potato drew its biggest loss during the 2008 collapse (31.1%) and didn’t recover until 2011. Its spicier sibling fared better because it was invested in bonds for a good part of that period: It fell only 10% from its 2007 high to its 2008 low, and had recovered fully by the summer of 2009.

Once again contrarians fared poorly. The Global Cold Potato Portfolio is moved monthly into the worst performing asset class of the prior year. By doing so, it gained an average of 7.9% annually and trailed the Global Couch Potato by 2.1 percentage points per year. The monthly return history of all three global potato variants is shown in the charts on the opposite page.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Couche-Tard reports higher Q4 profit and revenue, BlackBerry raises full-year outlook after a stronger quarter, and Metro sees earnings...

Reitmans narrowed its quarterly loss and Empire raised its dividend, but investors sent Groupe Dynamite and Gildan shares sharply...

Robinhood’s WonderFi acquisition closes as Shopify adds US$3 billion to its buyback plan and Apotex targets a $1-billion IPO.

Canadian bank earnings season delivered higher profits, lower credit-loss provisions and dividend increases across much of the sector.

Canadian depository receipts may offer convenience and accessibility, but they come with numerous trade-offs investors should be mindful of.

Canadian investors got a wave of earnings news this week, from Barrick’s profit surge to stronger results at Cineplex...

Investors may be paying high fees for lower risk-adjusted returns with these concentrated covered-call ETFs, all in the name...

A mixed Q1 earnings roundup that includes gains from Bombardier and Gildan alongside losses at Spin Master and others.

BlackBerry’s Nvidia-driven rally and Lululemon’s selloff highlighted a mixed week for Canadian stocks, alongside strong results from Teck Resources...