How to retire at 55 on $55,000 a year

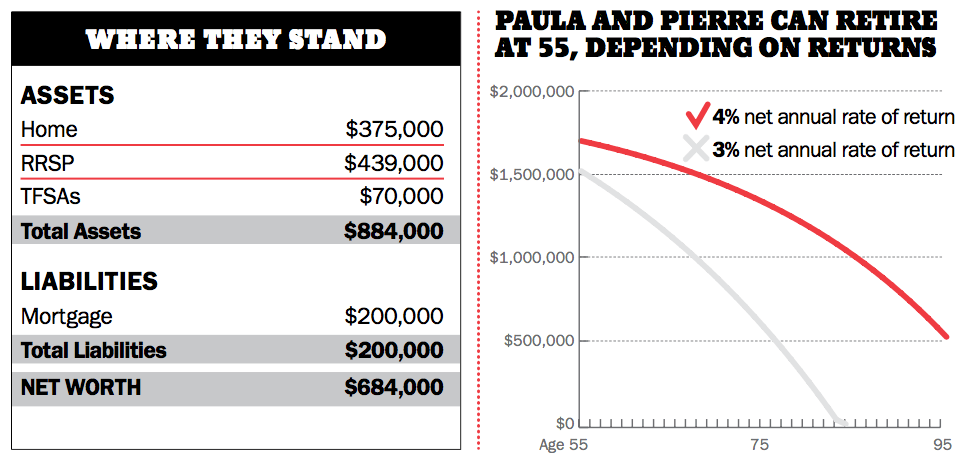

Paula and Pierre's dream retirement rests solely on their investment returns

Advertisement

Paula and Pierre's dream retirement rests solely on their investment returns

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

Dollarama reports increases in profits and sales, Transat deals with Canadian travellers avoiding the U.S., and Roots sees Q1...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...