The right path to riches

Seth and Rachel have all their money invested in real estate. Can they still retire at 65?

Advertisement

Seth and Rachel have all their money invested in real estate. Can they still retire at 65?

Eight years ago, Seth and Rachel Jacobson of Edmonton met through an online dating website. The two hit it off right away in their initial meeting at a local diner. “We realized immediately that we had a lot in common,” says Rachel, 37, an office manager in Edmonton. “We both love adventure travel and given that we both spent time studying theology in bible college, our philosophy about life and how to live it meshed nicely.” (We’ve changed names to protect privacy.)

While the couple have two dogs, their focus shifted this past year. Now, they want to start a family—hoping for two or three children over the next five years. Trouble is, the Jacobsons consider themselves novices when it comes to investing in anything besides real estate and they’re afraid they’ve missed the boat when it comes to building a financial portfolio. Currently, they own a house and two rental properties—all of which have mortgages. “One of us grew up in a very religious home where investing was considered ‘worldly’ and not ‘planning for heaven,’” says Seth, who works in communications for a local college. “So we’ve come late to investing in stocks or mutual funds. But we’re realizing that we may have too many eggs in the real estate basket and I don’t know how to change that.”

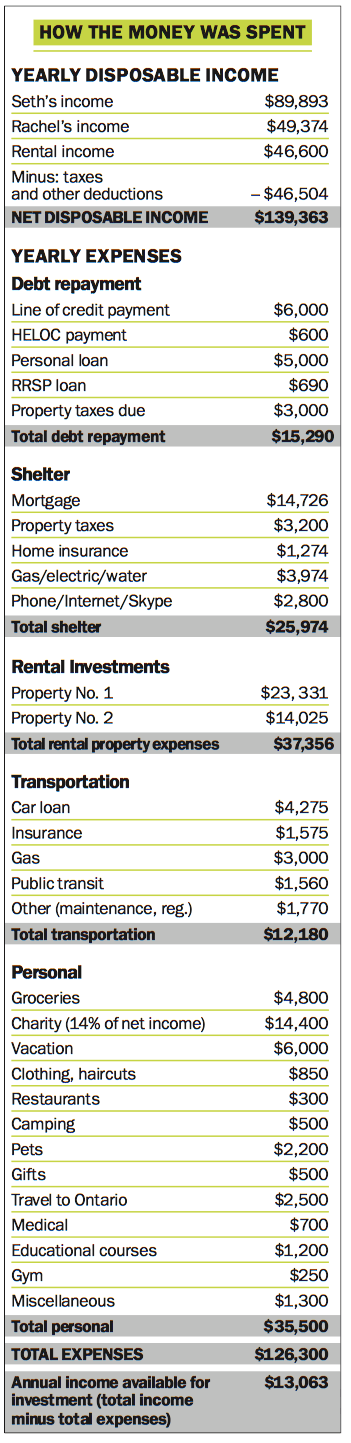

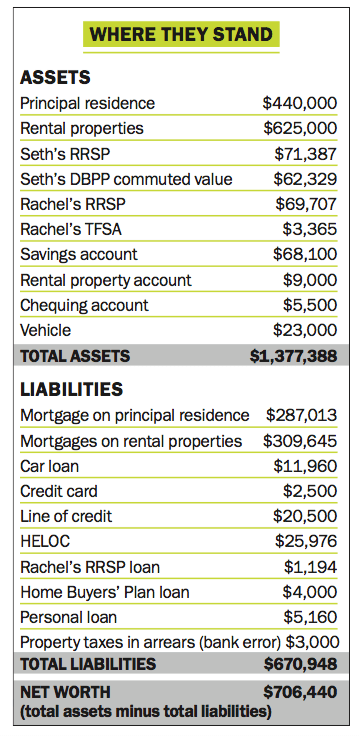

Between them, Seth and Rachel make about $140,000 in household income and their three properties are worth approximately $1,065,000, although they still owe just under $600,000 on the mortgages. The couple also has $708,850 in savings with the majority invested in GIC rates and roughly $145,000 invested in their TFSAs and RRSPs. They also have another $83,000 sitting in various bank accounts. “We parked our money here because we’re unsure of where to invest outside of real estate,” says Seth.

The crux of the couple’s frustration is whether or not they should be using TFSAs and RRSPs more strategically. Right now, the couple is on track to pay off all their mortgages by the time Seth turns 65. This debt repayment is helped, in part, by the $5,000 in net income they earn each year from their rental properties. If finding a good investment strategy wasn’t challenging enough, Seth and Rachel have decided that once they have children, they will remain a one-income family for 12 to 14 years, with their children being home-schooled by Rachel. Their priority now is to grow their family. “I’m undergoing fertility treatments and we’ve put our names on adoption lists. We want a full and happy family life,” says Rachel. But Seth is worried. “Looking at the numbers and facing the fact that I’m 45, I don’t know how we’re going to reconcile our goals to have a family with our desire to retire at 65,” says Seth. “Are both these goals still achievable for us?”

The good news is that Seth and Rachel were able to prioritize their goals, and for this couple, family now comes first. In fact, this goal is so important they are willing to cut back on many of their expenses, including the $14,000 they give annually to charity. However, cutting out charitable donations completely isn’t an option. It was Seth’s generosity that first drew Rachel to him: “He had strong religious beliefs, was frugal and made charitable giving a priority,” says Rachel. “Add that to his adventurous side and his love for travel and I was drawn to him.“ Both Seth and Rachel were raised in religious families where giving was a priority. “When we have kids, we will bring our charitable giving down to whatever is within our means,” says Rachel. “The amount itself is not critical to us.”

Having goals and values that are the same is certainly an advantage and this is, in part, because both Rachel and Seth attended bible college in their twenties. Each one then went on to complete college diplomas—in communications for Seth and in office management for Rachel. When they met online in 2006, they immediately recognized their shared values and joys. This has translated into some wonderful adventures for Seth and Rachel. “This was a first marriage for both of us and we’ve enjoyed a lot of travel, including a $6,000 safari in Africa last year,” says Rachel. “When we have a family, we plan to keep travelling, but just doing it different. Maybe doing some home-exchange vacations and throwing some house-sitting into the mix.”

Another big advantage is the couple’s ability to save. Before marrying in 2010, both Seth and Rachel each bought a duplex. (Rachel bought the investment property with her sister, while Seth went at it alone.) After marrying the two bought a home together just outside of Edmonton. Today, the house has a market value of $440,000 and there is $287,013 left on the mortgage. “One day we’d like to have a small home in the country, but we realize that’s a lot of work,” says Seth. “So for now, we plan to stay in our home.”

Right now, what worries them is the fact that their debt repayment has been at a minimum, while their savings are ballooning. In addition to their home mortgage, they also owe $309,000 on their rental properties as well as $74,290 in other personal debt, including a car loan, equity line of credit and a personal loan that was used to pay for their trip to Africa. “Unfortunately, all we did over the past five years was make regular biweekly payments on our principal residence—no extra payments, mainly because interest rates were so low and we were planning to build savings for another rental property,” says Seth.

“The truth is, real estate investing has been good to us and we’ve been building up cash because we’re considering the purchase of a third rental property,” says Seth. “But I think a good stock portfolio also has its merits. We’re unsure of what to do next.”

Seth points out that his parents never discussed money but managed and saved well. “Dad thought the stock market was too risky, but never lived beyond his means,” says Seth. “I’m like him in that I believe in the value of looking for a good deal, and Dad’s wisdom of ‘I can save even more if I don’t buy it,’ has guided me through life.” This philosophy hasn’t stopped the couple from living, though. Each year they spend about $2,500 on two separate trips to Saskatoon to visit Seth’s ailing parents. They also spend about $2,200 each year on their two black labs—Goldi and Pablo. This leaves the couple just over $13,000 each year to invest, but that may change dramatically when Rachel leaves her job to become a full-time mom. “These expenses probably won’t go down much,” says Rachel, “but everything else is available for trimming.”

But the couple’s indecision has led to paralysis and confusion when it comes to choosing an investment strategy. “Our limited investment knowledge gets in the way of making good decisions,” says Seth.

For instance, Seth doesn’t know if he should maximize his own RRSP savings, given that he’s been a member of his company’s defined benefit pension plan for the last 11 years. With eyes on the long term, Seth is concerned that the pension won’t provide enough money for their retirement at age 65. “We’ll have three kids at that time who will still need to be supported in some way or another,” says Seth. “If it means working past age 65 that may be a compromise I will have to make for the family.”

To overcome their concerns, the couple reads about investing and they like the idea of building a low-cost, passive portfolio with ETFs and index funds. But they’re still not sure of two things: their risk tolerance and how much money they’ll need once Rachel leaves the workforce. “We’ll be a one-income family for a while so that’s challenging,” says Seth.

Seth and Rachel Jacobson are doing lots of things right. Their two greatest assets are a solid household income coupled with the fact that they see eye-to-eye in their philosophies about life and money. “They strike me as being two very capable people who are surrounded by a lot of noise which leaves them feeling scattered,” says Julia Chung, a certified financial planner with JYC Financial in Vancouver. “They have to pick one priority and, right now, that’s growing their family. Then their financial goals need to suit that life goal.” Here’s what the couple should do.

Pay down their debts. With a growing family, the Jacobsons will have many years ahead with a lower household income and higher expenses. Annie Kvick, a certified financial planner in Vancouver says they should focus on paying off their personal debts (their credit card, line of credit, car loan, etc.) before Rachel goes on maternity leave. The couple also needs to cut their charitable donations to $1,000 a year, from $14,000. Do all this and, along with Seth’s income and the $5,000 in rental income, they should have an annual household income around $65,000—enough to live well as a one-income family, says Kvick.

Reconsider real estate. Right now, the Jacobson’s have 77% of their assets in real estate. That’s too much, say the experts. “It makes sense to diversify,” says Chung. “Any additional real estate purchases should be put on hold until their primary goal of having and managing a family has been realized.” Heather Franklin, a financial planner in Toronto, goes one step further: She thinks the Jacobsons should sell one of their rental properties and use the proceeds to pay off the mortgage on their principal residence. “If they sold both rental properties they could pay down their mortgage and their personal debt and get close to debt-free, an ideal position when living on one income and starting a family,” says Franklin.

Maximize Rachel’s RRSPs. Chung advises Rachel to top up her RRSP while she’s still working. This will give her a tax rebate each year and that can be used to further pay down debt. “It will also give her some RRSP savings to draw on, if the need arises, when she’s raising the kids.”

Top up TFSAs. Then, the couple should use the balance to top up both Seth and Rachel’s TFSAs. Do this every year, says Kvick. “The money can serve as their emergency fund.”

Seek professional advice. To determine an investment strategy, the Jacobsons should get help from a fee-for-service financial planner. “Then, they can build a DIY couch potato portfolio, or one using dividend-paying stocks if they’re comfortable with that,” says Franklin. “The key is to start and get something in place with some help from an unbiased third-party.”

Review life insurance. Seth has excellent disability insurance coverage at work but the couple needs to review their life insurance needs. “The rule of thumb is enough to [replace] five to 10 times your annual income,” says Lorne Marr of LSM Insurance in Markham, Ont. The lesser amount applies if you have kids under the age of 10. But increase your coverage when the kids are older than age 10. A 20-year term policy for Seth that pays out $900,000 will cost $1,776 annually. For Rachel, a stay-at-home mom, a 20-year term policy for $300,000—which should cover the cost of a nanny should something happen to Rachel—will cost $276 annually. “It’s the minimum they should consider,” says Marr.

If they take all this advice, the couple will have a solid income of close to $70,000 per year throughout retirement. This would include Seth’s defined benefit pension plan (likely worth $40,000 per year in retirement in today’s dollars), CPP of $16,000 and OAS of $13,200. At that time, they will also have either paid off all their properties or sold the rentals and built up an investment portfolio worth a few hundred thousand dollars. “If they decide to keep the rental properties and have a minimal investment portfolio, they’ll still do well,” says Kvick.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Sponsored By

Equifax

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Bonds are considered safer than stocks, but higher interest rates can still lead to losses. Here's what investors need...

Incorporating can eliminate the need to pay CPP contributions if you are self-employed but there are trade-offs that should...

BlackBerry is back, baby, and other standout stories from yet another good quarter for Canadian equities.

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Experts say the best way to prepare for a single-income household is to test your budget first. Here's how...

Moving to the U.S. doesn’t automatically mean you should convert your Canadian investments. Here’s why tax rules, currency risk...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...