Income splitting a boon to families

Canadians tasted income splitting with pension splitting for seniors. Extending it to families would be an even greater benefit.

Advertisement

Canadians tasted income splitting with pension splitting for seniors. Extending it to families would be an even greater benefit.

However, income is not always a true test of ability to pay. It’s possible to have little income but great wealth, as many investors, farmers and landlords may tell you. It’s hard to achieve absolute tax fairness when sources of income and capital are so diverse.

One neighbour may earn employment income while his wife is self-employed. There may be dividend sprinkling from Grandpa’s family trust, and refundable and non-refundable tax credits for their children.

But your other neighbours may be pensioners who are already income splitting, drawing investment earnings from their Tax-Free Savings Accounts—never taxable—while deferring tax on accrued gains in registered and non-registered investments. They may have downsized, enjoying a large tax-exempt gain on the sale of their former principal residence, and claiming significant tax credits for a new disability in the family.

Across the street, a young family with newborn twins may be waiting for their first Universal Child Care Benefits (not income tested) and Canada Child Tax Benefits, where the benefit is based on combined family net income.

When we ask a simple question like who benefits from income splitting, the answer is complex. In some scenarios, the household economic unit as a whole must be taken into account. This raises the question whether our tax system would benefit from broader tax reform; one that taxes the household rather than individuals.

Statistics Canada defines a household as a group of individuals sharing a common dwelling unit, related by blood, marriage/common law or adoption. Stats from 2011 show two-parent families with children under 18 had an average market income of $106,100; an economic family of two people or more earned an average $84,400; Lone-parent families earned an average $39,100.

These figures put the size of actual market income—total income of a household minus government transfers—into perspective. It helps us better answer the key question: Would family income splitting help average families with children?

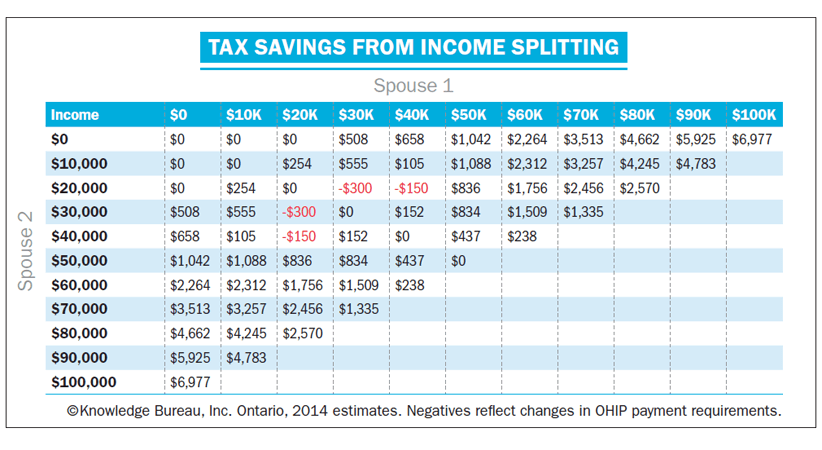

The answer is a resounding yes, particularly if one spouse has no income and the other earns all of it. As the chart shows, for an Ontario family, savings can reach almost $7,000 a year. Over 25 years, that’s $175,000 a family before investment returns.

From those tax savings $5,500 could be invested annually in a TFSA for the spouse who didn’t work over a 25-year child-rearing period. This stay-at-home spouse ends up with a tax-free retirement fund of $275,624 (based on 5% returns). Since average couples should save $250,000 to $750,000 for retirement, depending on desired lifestyle, that’s enough security to trade work time for more time with family.

Note that the savings shown here chiefly accrue to families with one big income and one much smaller. Low-income families would benefit more by raising the Basic Personal Amount instead.

This may be an issue in the next election. If you believe a simpler tax system is a more compliant one, family income splitting could indeed be a really good thing.

Evelyn Jacks is President of Knowledge Bureau, a national financial educational institute. She tweets @evelynjacks.

However, income is not always a true test of ability to pay. It’s possible to have little income but great wealth, as many investors, farmers and landlords may tell you. It’s hard to achieve absolute tax fairness when sources of income and capital are so diverse.

One neighbour may earn employment income while his wife is self-employed. There may be dividend sprinkling from Grandpa’s family trust, and refundable and non-refundable tax credits for their children.

But your other neighbours may be pensioners who are already income splitting, drawing investment earnings from their Tax-Free Savings Accounts—never taxable—while deferring tax on accrued gains in registered and non-registered investments. They may have downsized, enjoying a large tax-exempt gain on the sale of their former principal residence, and claiming significant tax credits for a new disability in the family.

Across the street, a young family with newborn twins may be waiting for their first Universal Child Care Benefits (not income tested) and Canada Child Tax Benefits, where the benefit is based on combined family net income.

When we ask a simple question like who benefits from income splitting, the answer is complex. In some scenarios, the household economic unit as a whole must be taken into account. This raises the question whether our tax system would benefit from broader tax reform; one that taxes the household rather than individuals.

Statistics Canada defines a household as a group of individuals sharing a common dwelling unit, related by blood, marriage/common law or adoption. Stats from 2011 show two-parent families with children under 18 had an average market income of $106,100; an economic family of two people or more earned an average $84,400; Lone-parent families earned an average $39,100.

These figures put the size of actual market income—total income of a household minus government transfers—into perspective. It helps us better answer the key question: Would family income splitting help average families with children?

The answer is a resounding yes, particularly if one spouse has no income and the other earns all of it. As the chart shows, for an Ontario family, savings can reach almost $7,000 a year. Over 25 years, that’s $175,000 a family before investment returns.

From those tax savings $5,500 could be invested annually in a TFSA for the spouse who didn’t work over a 25-year child-rearing period. This stay-at-home spouse ends up with a tax-free retirement fund of $275,624 (based on 5% returns). Since average couples should save $250,000 to $750,000 for retirement, depending on desired lifestyle, that’s enough security to trade work time for more time with family.

Note that the savings shown here chiefly accrue to families with one big income and one much smaller. Low-income families would benefit more by raising the Basic Personal Amount instead.

This may be an issue in the next election. If you believe a simpler tax system is a more compliant one, family income splitting could indeed be a really good thing.

Evelyn Jacks is President of Knowledge Bureau, a national financial educational institute. She tweets @evelynjacks.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The GST quick method can simplify tax reporting for small businesses—but it’s not right for everyone. Here’s who qualifies...

Changes to Canada’s Disability Tax Credit will make it easier to qualify, reduce CRA red tape, and expand access...

You might be missing valuable tax credits, deductions, and filing opportunities. Here are nine ways to maximize your tax...

Tax instalments can be confusing. Learn how the CRA calculates quarterly payments, when you can adjust them, and how...

How Canadians with disabilities can navigate tax season, including credits, deductions, and programs that can help offset higher costs...

Your CRA My Account may hold uncashed cheques, credits, and tax info you’ve missed. Here are 5 key areas...

Filing your taxes isn’t just a requirement—it’s the first step to accessing benefits, credits, and financial opportunities in Canada....

Make the most of your 2026 tax refund with smart strategies to pay down debt and build savings, so...

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...