Just because your credit score needs some work doesn’t mean you can’t get a credit card—but you’ll need to pay a bit more attention to eligibility requirements, and consider getting a secured credit card that can help you improve your credit score.

We’ve listed our favourite secured credit cards that are easy to qualify for, as well as alternative unsecured cards. Many of these unsecured options are geared toward students or newcomers who may not have a solid credit score yet.

The best credit cards for bad credit in Canada

Maybe you’re one of the many Canadians who missed a debt payment in the last year. Or, perhaps you’re a newcomer to Canada or a young person without an established credit history.

Whatever the reason for your low or non-existent credit score, you’ll need to show lenders that you can handle credit responsibly. The credit cards on this list can help you do that—and they’re accessible to almost all applicants.

Home Trust Secured Visa Card

Secured Neo Mastercard

Scotiabank Momentum No-Fee VISA Card

Gold: Capital One Guaranteed Secured Mastercard

Card type: Secured

Minimum credit score: N/A

Minimum income required: N/A

You’re guaranteed to be approved for the Capital One Guaranteed Secured Mastercard, as long as you’re of the age of majority in your province, you don’t have an existing Capital One account (or have applied for one in the past 30 days), and you haven’t had a Capital One account in bad standing in the past year. This card offers an effective way to build your credit and even offers a few extras.

Capital One Guaranteed Secured Mastercard

Annual fee: $0

Rewards: None

Welcome offer: None at this time

Card details

| Interest rates | 21.9% to 29.9% on purchases, cash advances and balance transfers |

| Income required | None specified |

| Credit score | None specified |

Pros

- No annual fee

- Guaranteed approval as long as you meet basic eligibility criteria

- Includes some travel benefits, such as common carrier travel accident coverage and car rental CDW/LDW

Cons

- No rewards or cash back

- Purchase interest rate of 21.9% to 29.9%—not ideal if you’ll carry a balance

Silver: Secured Neo Mastercard

Card type: Secured

Minimum credit score: N/A

Minimum income required: N/A

You can start using the Secured Neo Mastercard with instant approval and has a cash back program that can get you an average of 5% cash back for purchases at partner businesses. You can also subscribe to optional “Bundles” that give you the ability to make your card more suited to your spending habits, with boosted rewards and perks like insurance coverage.

Secured Neo Mastercard

Annual fee: $96 ($7.99/month)

Rewards: 1% cashback on gas & groceries, plus up to 15% back at over 10,000 Neo partners across Canada

Welcome offer: None at this time

Card details

| Interest rates | 19.99% to 29.99% on purchases (19.99% to 24.99% for Quebec residents) and 22.99% to 31.99% on cash advances (22.99% to 25.99% for Quebec residents) |

| Income required | None |

| Credit score | None |

Pros

- Customizable Bundles to tailor the card to your needs

- Unlimited cash back on your purchases

- Guaranteed approval

- Gift card offer: $50 Indigo, SkipTheDishes or a Virtual Prepaid Mastercard $150. Offer ends September 15, 2026.

Cons

- Must shop with partners to get the most cash back

- Almost no extras unless you subscribe to Bundles

- No insurance coverage without Bundles

Bronze: Home Trust Secured Visa

Card type: Secured

Minimum credit score: 300

Minimum income required: N/A

The Home Trust Secured Visa offers more flexibility than most secured credit cards by offering you two options: an interest rate of 19.99% with no annual fee, or a lower interest rate of 14.90% with a $59 annual fee. You also have a say on your credit limit: deposit $500 to $10,000 and your chosen amount becomes your limit. And since Home Trust reports your payments to the credit bureaus, responsible use of this card will boost your score.

Home Trust Secured Visa

Annual fee: $0

Rewards: Does not offer rewards.

Welcome offer: None at this time.

Card details

| Interest rates | 19.99% on purchases and 19.99% on cash advances |

| Income required | None specified |

| Credit score | 300 or higher |

Pros

- No annual fee—or lower your purchase interest rate to 14.90% for a $59 annual fee

- Issued by a bank, with protection for your security deposit

Cons

- $500 minimum security deposit

- No rewards or perks

- $12 fee for accounts that are inactive for a year

- Not available to residents of Quebec

How we determine the best cards

To select the best cards in this somewhat-limited category, we evaluated key factors that are important when choosing a card if you have poor credit: approval likelihood, annual income requirements, and annual fees, plus interest rates, and welcome offers. The addition of links from affiliate partners has no bearing on the results in this ranking. Read more about the MoneySense selection process and about how MoneySense makes money.

Other top credit cards if you have bad credit

While we originally highlighted secured credit cards, you might actually qualify for unsecured credit cards even with bad credit. Check out some of these cards that have low credit scores or income requirements to see if they’re a better fit.

| Credit card | Annual fee | Recommended income | Apply now (featured cards only) |

|---|---|---|---|

| Scotiabank Momentum No-Fee Visa | $0 | $12,000 per year | Apply now |

| BMO CashBack Mastercard | $0 | $15,000 per year | Apply now |

| PC Mastercard | $0 | None specified | Apply now |

| CIBC Aeroplan Visa Card for Students | $0 | None specified | Not available |

Scotia Momentum No-Fee Visa Card

Card type: Unsecured

Minimum credit score: 660

Minimum income required: $12,000

Scotia Momentum No-Fee Visa Card

Annual fee: $0

- 1% cash back at gas stations, grocery stores, drug stores and recurring bills

- 1% cash back on transit, rideshare and food delivery

- 0.5% on everything else

Welcome offer: Earn 5% cash back for the first 3 months (up to $2,000 in total purchases). Plus, pay 0% interest on balance transfers for the first 6 months. Offer ends March 1, 2026.

Card details

| Interest rates | 19.99% on purchases, 22.99% on cash advances, 22.99% on balance transfers |

| Income required | $12,000 per year |

| Credit score | 725 or higher |

Pros

- 1% cash back on gas, groceries, drug stores, and recurring payments

- No interest for six months on balance transfers

- Free supplementary cards

- Cash Back anytime feature redeem your Cash Back anytime ($25.00 minimum required) instead of having to wait for an annual payout in November.

Cons

- 0.5% base earn rate on non-boosted purchases

- No included insurance coverage

- 22.99% interest on balance transfers after the promotional period

BMO CashBack Mastercard

Card type: Unsecured

Minimum credit score: N/A

Minimum income required: N/A

BMO CashBack Mastercard

Annual fee: $0

- 3% cash back on groceries (on the first $500 per month)

- 1% on recurring bills

- 0.5% on everything else

Welcome offer: Get up to 5% cash back in your first 3 months and a 0.99% introductory interest rate on Balance Transfers for 9 months with a 2% transfer fee.

Card details

| Interest rates | 21.99% on purchases, 23.99% on cash advances, 23.99% on balance transfers |

| Income required | n/a |

| Credit score | None specified |

Pros

- No credit check

- Welcome offer of 5% cash back in your first 3 months

- 3% cash back on groceries and 1% on recurring bills

- Redeem cash back with as little as $1 accrued

- Discount of up to 7 cents off per litre at Shell

- No annual fee

- Enjoy six months of Instacart+ and a $10 monthly Instacart credit when you enroll your eligible BMO Credit Card.

Cons

- 0.5% cash back on non-boosted purchases

- Limited purchase insurance included

PC Mastercard

Card type: Unsecured

Minimum credit score: 560

Minimum income required: N/A

PC Mastercard

Annual fee: $0

Welcome offer: Earn 20K points when you spend $50 or more at participating stores within 60 days of account approval.

- 25 points per $1 spent at Shoppers Drug Mart

- At least 30 points per litre at Esso and Mobil gas stations

- 10 points per $1 on everything else

Card details

| Interest rates | 21.99% on purchases, 22.97% on cash advances and % on balance transfers |

| Income required | None specified |

| Credit score | 560 or higher |

| Point value | 1 PC Optimum point is worth $0.001 (redeem 10,000 points for $10) |

Pros

- 25 points per $1 spent at Shoppers Drug Mart and 30 points per litre of gas at Esso and Mobil—a return of up to 3%

- Easy redemption at Loblaw-affiliated stores and Esso stations

- No cap on how many PC Optimum points you can earn

Cons

- Redemptions are restricted to specific retailers

- Must redeem a minimum of $10 at a time

- Relatively high standard purchase interest rate of 21.99%

CIBC Aeroplan Visa Card for Students

Card type: Unsecured

Minimum credit score: N/A

Minimum income required: N/A

CIBC Aeroplan Visa Card for Students

Annual fee: $0

- 1 point per $1 spent on gas and EV charging, groceries and Air Canada purchases

- 0.67 points per $1 on everything else

Welcome offer: earn 10,000 Aeroplan points when you make your first purchase ($200 value)

Card details

| Interest rates | 20.99% on purchases and 22.99% on cash advances (21.99% in Quebec) |

| Income required | None specified |

| Credit score | None specified |

| Point value | . |

Pros

- Up to 1.5 Aeroplan points per $1 spent on the card

- Flexible redemption options, including flights and merchandise.

- No blackout dates on Air Canada flight redemptions

- Free SPC+ membership for savings at select merchants

Cons

- No Status Qualifying Miles earned on everyday purchases

- Limited value if you don’t frequently travel with Air Canada or its partners

- Limited insurance included

Reddit reviews: What cardholders say

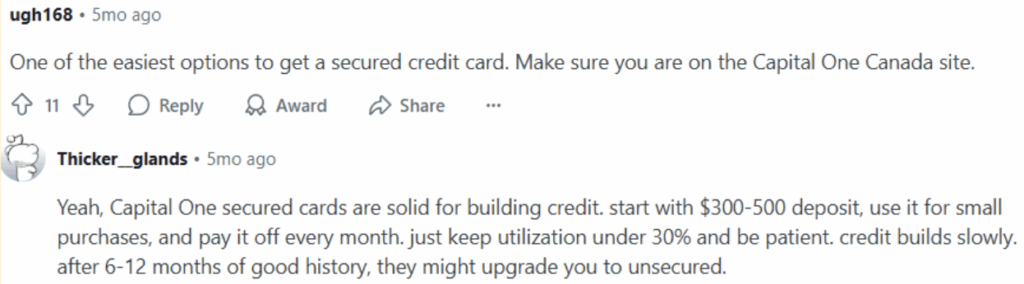

We were curious to see how our top cards for bad credit fared in real life, so we checked out Reddit for real user feedback.

Many Redditors recommended the Capital One Secured Mastercard and offered useful advice.

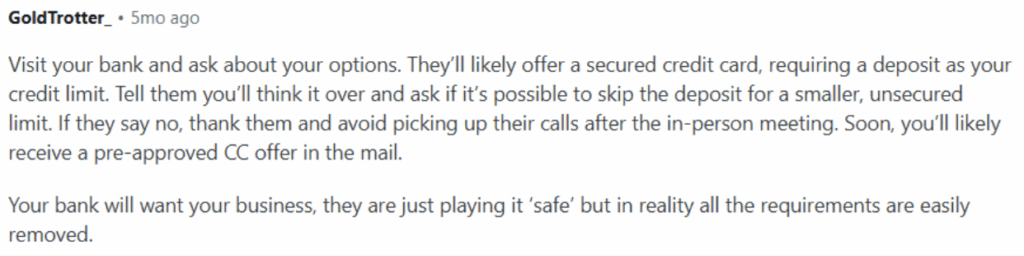

Another person pointed out a helpful strategy if you’re getting denied for credit cards.

Ultimately, building your credit score depends less on the card you choose and more on how you use the card.

Find the perfect card with CardFinder

In under 60 seconds, get matched with a personalized list of the best credit cards based on your spending personality and approval likelihood. No SIN required.

How credit cards can help you build credit

Once you have a credit card, your payment history will be reported to the credit monitoring bureaus that generate your credit score. It’s actually the most important factor in determining your score.

To improve your payment history, make at least the minimum credit card payment on time every month. Ideally, you’d pay your credit card balance in full so you’re not charged interest. If you think you might have trouble making the monthly minimum payment, contact your card issuer and discuss your payment options. This is better than skipping the payment and hoping you’ll be able to pay it later.

You should also be strategic about using your credit card. Never go over your card’s limit or you could face additional fees. This can also damage your credit utilization ratio, which is an important piece in your credit score calculation.

What is a credit utilization ratio?

Credit utilization ratio is the amount of available credit you’re currently using (usually shown as a percentage). The higher the percentage, the more strapped for cash you may appear—a definite warning sign for credit bureaus.

3 types of credit cards for bad credit

It helps to be familiar with credit card types since they have different eligibility requirements and expectations.

- Secured credit cards: A secured credit card requires you to pay a security deposit upfront, which then becomes your credit card limit. These cards are marketed directly to those with bad credit, so they have an easier approval process—although the cards themselves come with no frills. Lenders report your activity to Canada’s two main credit bureaus, TransUnion and Equifax. As you continue to repay your debts responsibly, you’ll build a credit history and improve your score.

- Unsecured credit cards: These are what most people think of when they picture credit cards. You’ll usually have to meet strict income and/or credit score requirements, so they’re not generally available to people with credit scores under 600. If approved, the card issuer gives you a credit limit that you borrow against. You’re essentially borrowing money and paying it back (sometimes, with interest).

- Credit builder products: Although using both a secured or unsecured credit card responsibly can build your credit score over time, you may be able to take out a KOHO prepaid credit card and subscribe to KOHO’s Credit Builder program. This reports your activity to Equifax, which can build your score over a matter of months.

We’ll also mention another option: becoming an authorized user on someone else’s credit card account. Depending on their credit card, they may have to pay a fee to add you, but you would have access to credit and earn rewards for the primary cardholder. Responsible use will help build your credit score—but conversely, irresponsible use can damage the credit score of the account holder.

How to improve your approval odds

Being prepared and informed is one of the best ways to improve credit card approval odds. In a nutshell, here’s what we recommend to tilt the odds in your favour:

- Check your credit report before applying: Look for inaccuracies that could be damaging your score and report the errors to the credit monitoring bureau. You may need to give it some time for your score to update, but find out what your score is before you apply for a credit card.

- Apply to cards that are designed for low-credit applicants: The cards on our list typically have lower credit score requirements. Many don’t have income requirements, or if they do, they’re low.

- Maintain a consistent income with low debt: This helps verify for credit card issuers that you’re responsible with your money. They may be hesitant to extend credit if you’re not holding down a steady job, as it could indicate that you’ll struggle to repay your credit card purchases.

- Limit the number of credit cards you apply for: Each time you submit an application, the card issuer pulls your credit report (known as a hard inquiry), which causes your score to temporarily dip. This isn’t a big deal if you’re only applying for one card, but submitting several applications can have a more significant impact.

- Pay down your existing debt: If you have loans or other credit cards with balances, try to pay them down before applying for a new card. Credit card issuers look at how much access to credit you have—and how much of it you’re using. If you’re already tapped out, they are unlikely to issue you a new card.

FAQs

Our top choice is the Capital One Secured Mastercard since you’re guaranteed approval as long as you make a security deposit and meet basic eligibility requirements.

It is possible, but it’s up to the card issuer to set your credit limit. In many cases, you’ll start with a low credit limit, which is increased over time with responsible use.

Secured credit cards have near-guaranteed approval since you provide a security deposit that acts as collateral. Essentially, you’re borrowing money from yourself. If you can’t pay your credit card debt, the issuer will use your deposit to cover it.

Most credit card issuers check credit scores—even for secured cards. The only cards that are guaranteed not to check your score are prepaid credit cards since they aren’t truly credit products.