By Romana King on December 3, 2014 Estimated reading time: 10 minutes

Condo overbuilding in Canada

By Romana King on December 3, 2014 Estimated reading time: 10 minutes

Increasing cranes in the skyline is not anecdotal proof of overbuilding

This article is 11 years old. Some details may be outdated.

Advertisement

(Getty Images / Michael Blann)

I’m not at all surprised that our government-backed housing agency—the Canada Mortgage and Housing Corporation—is warning condo builders to sell more of their current inventory before building more condos.

But I don’t think it’s a signal we’re overbuilding. I think it’s a signal that the government doesn’t want another close call.

From the late 1990s to 2008, the government loosened housing and mortgage policies. For instance, the government lowered down payment requirements so that home buyers could avoid default insurance (otherwise known as mortgage insurance); the government also introduced 35-year and 40-year amortizations and introduced government backed 100% financing—even for rental properties; and income documentation to obtain a mortgage was far more lenient than it is today. Then the U.S. housing market took a dive and the 2009 world wide credit crunch made everyone take a step back—including our government.

As such, policies were introduced to tighten up the lax regulations that were previously introduced by the government. This included putting our national $600-billion insurance company, otherwise known as the CMHC, under the watchful-eye of the banking and insurance regulator (the Office of the Superintendent of Financial Institutions).

So…? What does this have to do with CMHC’s recent warnings to condo-developers to slow down on building? It’s the next move in the government’s attempt to reduce any and all exposure it has in Canada’s continually robust housing market. It’s taxpayer money, so this is exactly what the CMHC and the government should be doing—staying conservative. But that doesn’t mean we’re overbuilding.

I recently spoke to Marc Pinsonneault, senior economist with the National Bank of Canada, about the supply of condos in Canada’s big cities. Based on his analysis, there is overbuilding in the Canadian condo market—but not in the cities you’d expect.

According to Pinsonneault developers are not overbuilding in Toronto, Vancouver or Calgary. However, buyers in Montreal, Saskatoon, Regina and Winnipeg should be careful as developers have overbuilt for these markets, explains Pinsonneault.

A little surprised? I was, particularly given all the commentary about overbuilding in Canada’s three hottest real estate markets. So, how can so many analysts—both within Canada and from international organizations—be so wrong? “It’s all about context,” says Pinsonneault.

When you examine permit applications and building starts we see that the numbers are increasing. Add context to these numbers and we see the bigger picture: Supply is actually keeping up with demand.

DEFINING THE TERMS

Before I jump in and qualify that last statement, I first want to get a few definitions in place.

Housing starts: Measures all developments that have actually started being built. This measurement can be broken down into condo units or freehold units (otherwise known as homeowner units).

Unabsorbed units: This is the number of unsold condos that are currently in the market (often in developer hands). This is measured in terms of real numbers—as in there are 35,000 unabsorbed units currently in the Montreal marketplace—as well as through a length of supply, as in there are two months of unabsorbed units, which means if no other condos are built, it will take approximately two months to sell off existing unsold inventory.

Absorption rate: The rate at which available homes are sold in a specific real estate market during a given time period, usually a 12-month period. It is calculated by dividing the total number of available homes by the average number of sales per month.

Importance of condos

Part of the reason why developers have not overbuilt in the three hottest markets in Canada is because demand is high in all three cities. But even from a national perspective demand, in general, is keeping up.

“In Canada as a whole, the number of completed and unabsorbed condo units amounts to only two months [worth of supply], versus the more than four months [of unabsorbed condos that existed] in the 1990s,” explains Pinsonneault.

But could this mean we’re heading into dangerous territory? Wasn’t there a housing bubble and a nationwide price correction in the 1990s and could that happen today? Not likely, says Pinsonneault.

While the quantity of unabsorbed condo units is back up to where it was just before the 1990s housing crash, this number doesn’t take into consideration the “growing importance of the condo market in the last 20 years,” says Pinsonneault. “The rising popularity of condos means that the market is now absorbing almost twice as many new condo units annually as in 1990.” While there may be the same number of unsold condos as there were 20 years ago, demand for these unsold units has more than doubled in the last two decades.

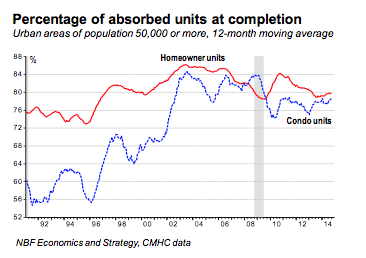

To get an idea of how increased demand in condos has changed the landscape of housing starts in Canada, take a look at this chart from the National Bank of Canada (below):

(Source: National Bank of Canada/Marc Pinsonneault)

“It’s very hard to take the number of unabsorbed new units as evidence that Canada, as a whole, has a glut of new housing,” says Pinsonneault. “For a glut to emerge, absorptions—which have been remarkably stable since 2010—would have to fall sharply without a corresponding reduction in housing starts.” Fact is, during the 12-month period ending September 2014, almost 80% of completed units (whether freehold or condo units) were sold.

But, as we all know, real estate is regional and overall condo starts don’t really provide a good enough picture when it comes to specific markets.

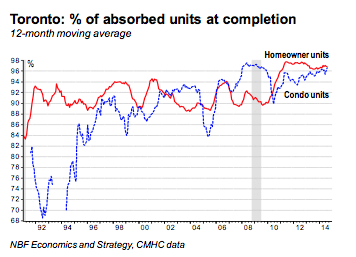

Toronto’s condo market is strong

In Toronto, the number of unsold condo units has remained low since late 2010. As of September 2014, there was less than a month of unsold units. The low inventory of unabsorbed units is actually due, in part, to the lack of land that can be used for freehold (or single family) homes. As a result, this has stimulated the supply of high-rise condo buildings, particularly in the downtown core, but also reaching further out into the inner suburbs of North York and Scarborough. As a result, this has meant a lot of cranes in the Toronto skyline—and as of September 2014, it’s meant that 47% of condo units currently under construction in Canada are located within the Greater Toronto Area.

This surge in building did actually cause a spike in housing starts in 2012, says Pinsonneault, and, without context, could’ve been mistaken as a period of overbuilding. However, when Pinsonneault normalized the length of time it takes developer to finish a condo project, the spike drops and, as of September 2014, the absorption rate was 0.8 months. That means the proportion of sold units at completion has averaged 96% since September 2013. And, judging by the firms that follow the Toronto condo market, most of the 55,000 condo units currently under construction are 85% to 90% presold, says Pinsonneault.

(Source: National Bank of Canada / Marc Pinsonneault)

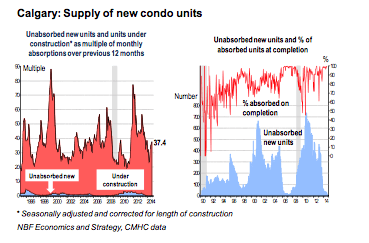

Calgary’s condo market is even stronger

Only one word can accurately describe Cow-Town’s 2014 condo market: Tight. By the end of the third quarter (Sept. 30) fewer than 400 unsold units existed in the fast-growing oil city. “We’ve not seen that level since early 1993,” says Pinsonneault. As such, there was only 0.6 months of absorption, a historical low for Calgary.

But over the last year, more and more cranes are seen in Cow-Town’s skyline. Could this be developer’s rushing to cash-in, only to create an oversupply? Not likely. But you never know.

In the last two decades, the city has experienced only two condo gluts: the first was 1998 to 1999, when 25% of new condos failed to find buyers. The other was 2009 going into 2010. It was the eve of the recession and with falling employment rates, buyers in the condo market dried up.

While the Calgary condo market has definitely pulled itself out of this glut—there’s almost a 100% absorption rate in 2014—the threat of unemployment due to continued decreases in oil prices remains a dark cloud in a relatively sunny condo climate. That said, Pinsonneault is not at all alarmed by the record number of condo starts in 2014. “The market is clearly undersupplied.”

(Source: National Bank of Canada / Marc Pinsonneault)

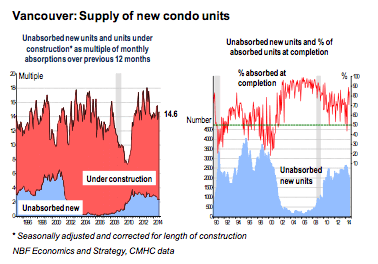

Vancouver’s condo market re-balanced, but is it enough?

Turns out all the predictions were true: Vancouver did overbuild. But the overbuilding occured between 2010 and mid-2012, when the percentage of sold, new units fell below 50%. Then, when developers faced a glut of unsold condos—numbers that exceeded the peaks of the last two recessions—they sharply readjusted by just halting new builds. The result was a market correction in 2013, and continued market correction this year. At present, more than 40% of all new units—both freehold and condo—are unsold upon completion. “Developers need to be prudent,” says Pinsonneault. I agree, only I would caution buyers. There’s enough in the market to demand better prices or more perks, but it may be prudent to simply wait and see if prices will readjust based on downward pressure from oversupply.

(Source: National Bank of Canada / Marc Pinsonneault)

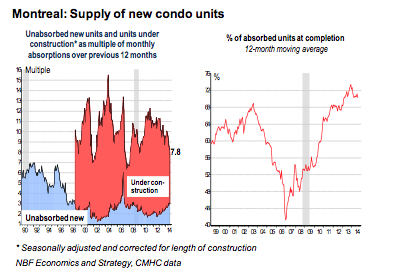

Montreal’s condo market is struggling

For the eighth consecutive year, Montreal ended with a greater number of unsold condo units then Toronto, despite have a population that’s a third less than the GTA.

From 1997 to 2005, absorptions were fairly stable in Montreal, but starting in 2005 the number of sold units at completion has continually declined. As of September, this meant an absorption rate of 2.1 months—a level not seen since 1997, says Pinsonneault. “The situation could worsen.”

For almost a year, the number of units under construction in Montreal has been growing relative to the number of units sold. This points to overbuilding, says Pinsonneault, due, primarily to excessive building in 2011 and 2012.

As a result developers are facing tougher competition, which will drive prices down in an oversupplied condo resale market. To prevent price drops in both the new and resale market, developers will have to slow down or stop future condo developments and reduce their number of unsold condos, says Pinsonneault.

(Source: National Bank of Canada / Marc Pinsonneault)

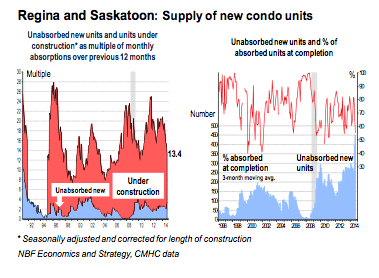

Regina and Saskatoon: Overbuilding still needs to go through correction

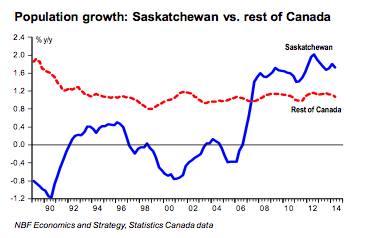

Before 2005, the population in Saskatchewan had been on a long, slow decline. This changed radically in 2007 when the the province’s population began to grow faster than the national average, due to an influx of oil workers.

(Source: National Bank of Canada / Marc Pinsonneault)

Developers saw a chance to try and beat demand and started to build, which prompted a spike in housing starts in 2012 and 2013. But slower than expected absorption forced developers to put the brake on building and, as a result, there’s been fewer starts in 2014. Still, the new condo market is struggling to off-load current new build supply. At present, there are 3.4 months of supply left in the marketplace.

(Source: National Bank of Canada / Marc Pinsonneault)

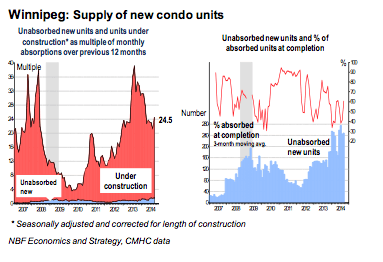

Winnipeg’s boom didn’t translate to the condo market

Unless you’re from Winnipeg, you may be scratching your head as to why the city’s condo market is currently overbuilt. Fact is, the condo market really didn’t exist in Winnipeg prior to 2007. But in 2012, the number of starts surged upwards—probably because developers wanted to cash-in on a hot real estate market (the city was ranked 5th best large city to live in MoneySense’sBest Places to Live ranking). As a result the stock of unsold units rose from 53 in April 2012 to 248 in September 2014. While this is only 1.5 months of absorption, Pinsonneault is convinced the number of unsold units will grow, given the number of condo projects currently under construction.

(Source: National Bank of Canada / Marc Pinsonneault)

Fact is, we can all look at the numbers, see increases and assume we’re in dangerous overbuilding territory. While this might be true for a few markets, it’s not the case for Canada’s largest real estate markets.

Read more from Romana King at Home Owner on Facebook »

For more on Canada’s potential housing bubble:

Read: Housing bubble? Depends on whether or read the numbers or the market

Read: Why are condos still being built in Toronto, Vancouver and Calgary?

Read: Condo complexity can add uncertainty to pricing