Use RRSPs and TFSAs to save on taxes

No. 1 way to thwart the tax man

Advertisement

No. 1 way to thwart the tax man

Of all the tax tips, this is the one that’s most important—after all, it’s the No. 1 way to thwart the tax man. While RRSPs and TFSAs work a bit differently, both are amazing tax shelters that can help you hold onto thousands of dollars of your hard-earned money every year. The RRSP lets you defer paying taxes on a portion of your yearly income until you retire in a lower tax bracket—which will be true for most people. Until then, your RRSP contributions grow tax-free, meaning you don’t have to pay capital gains taxes when you sell stock or funds at a profit, nor do you have to pay tax on dividends or interest. TFSAs are similar to RRSPs in that contributions put into these accounts grow tax-free. Unlike the RRSP, TFSA contributions earn no up-front tax refund, but the government doesn’t get a dime of your money when funds are withdrawn.

» RRSP vs. TFSA: Which is right for you?

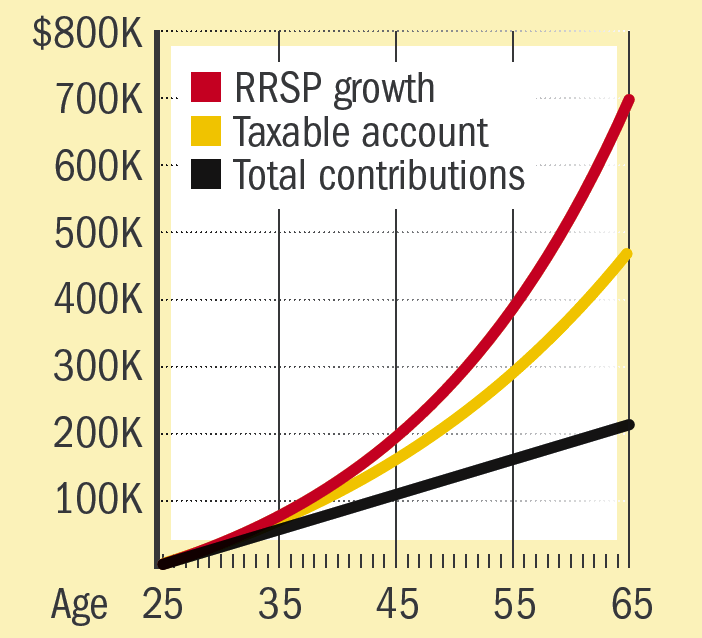

Tax savings: The more you make and the more you contribute, the more you’ll save. The chart to the above shows how much faster weekly $100 contributions made in an RRSP over 40 years grow versus a regular taxable savings account. Assuming a 5% annual rate of return on investments and a 30% marginal tax rate, using the RRSP makes a $220,537 difference!

Of all the tax tips, this is the one that’s most important—after all, it’s the No. 1 way to thwart the tax man. While RRSPs and TFSAs work a bit differently, both are amazing tax shelters that can help you hold onto thousands of dollars of your hard-earned money every year. The RRSP lets you defer paying taxes on a portion of your yearly income until you retire in a lower tax bracket—which will be true for most people. Until then, your RRSP contributions grow tax-free, meaning you don’t have to pay capital gains taxes when you sell stock or funds at a profit, nor do you have to pay tax on dividends or interest. TFSAs are similar to RRSPs in that contributions put into these accounts grow tax-free. Unlike the RRSP, TFSA contributions earn no up-front tax refund, but the government doesn’t get a dime of your money when funds are withdrawn.

» RRSP vs. TFSA: Which is right for you?

Tax savings: The more you make and the more you contribute, the more you’ll save. The chart to the above shows how much faster weekly $100 contributions made in an RRSP over 40 years grow versus a regular taxable savings account. Assuming a 5% annual rate of return on investments and a 30% marginal tax rate, using the RRSP makes a $220,537 difference!

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Now's the time to toss the piggy bank and open a bank account instead

It's important to start teaching your kids about money early

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...