Marrying their money

Miranda and Jake both brought significant assets into their relationship, and now the couple is struggling to combine accounts and stay financially independent. It's time for them to stop acting like roommates.

Advertisement

Miranda and Jake both brought significant assets into their relationship, and now the couple is struggling to combine accounts and stay financially independent. It's time for them to stop acting like roommates.

Two years ago, if you had asked Jake and Miranda Rodriguez about the secret to a happy marriage, they would have said “separate finances.” Jake, 38, a city planner in the Ontario government, earns $96,000 annually. Miranda, 35, is a social services worker who makes $84,000. They married in 2010. (We’ve changed their names to protect their privacy.) “We talked about our goals, took a pre-marriage course and discussed some ideas on how we would manage our money together,” says Miranda. “But talking about it and doing it are two different things. We both brought significant assets to the marriage and want to be fair. It’s harder to do than it sounds.”

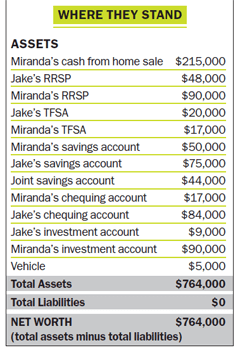

The couple’s finances are in excellent shape. Both have worked full-time for over a dozen years and they’ve saved lots of cash in their RRSPs, TFSAs and other accounts, in addition to their solid government pensions. They have no debt. Miranda even owned a home mortgage-free—a small two-bedroom bungalow in Oshawa, Ont.—until she sold it this summer for $215,000. “The money I got for the house is now sitting in a savings account. Jake and I are renting a duplex apartment now and plan to buy a house together in three years.”

Why so far into the future? Because Jake plans to save $215,000 himself before the couple buys the house together. “We really want to make equal contributions to our new home,” says Miranda. “Jake says he will need three years to come up with his share so when he reaches that milestone, we’ll buy.”

This summer the couple sat down and worked out a system for their finances that allowed each to maintain some independence. As a result, they keep separate chequing* and savings accounts*, TFSAs*, RRSPs* and non-registered investment accounts, plus joint chequing and savings accounts used for several different purposes. “Even though all our bills are getting paid, we’re finding it’s overwhelming having all these accounts,” says Jake. “We really need to streamline our system, while at the same time being fair about where our money goes every month.”

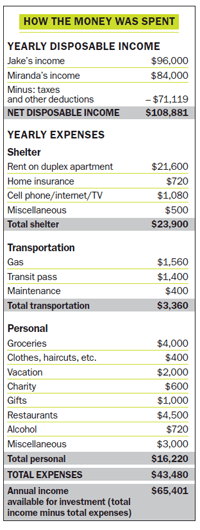

While Jake and Miranda value their independence, they’re starting to feel they’re drifting without a joint financial plan. “Right now we have almost all of our money in cash in almost a dozen accounts,” says Miranda. “It’s not very efficient.” Each contributes $500 a month to a joint chequing account to pay household bills. They also contribute weekly to an individual savings account ($187.50 each), and make monthly contributions to TFSAs and RRSPs. “Until now we’ve used different accounts for different financial goals,” says Miranda. “But it’s getting a bit unwieldy.”

Another concern is they have no investment plan. “All our investments have produced lacklustre returns,” says Miranda. “The truth is we’re great savers but the money isn’t working for us at all.” They have almost $140,000 in RRSPs, largely invested in mutual funds. “Our returns on our mutual funds have been flat,” says Jake. Total it all up and the couple has more than $700,000 in liquid assets, most of it sitting in cash. “And our savings have given us next to nothing in interest. We want to do it right but don’t know where to start. It’s quite overwhelming.”

Miranda has started to investigate laddered GICs and exchange-traded funds (ETFs) as possible options, but hasn’t yet acted on it. “I want to be actively engaged in managing my money,” she says. “But Jake sees it differently.” That’s because Jake lost $12,000 on some stock trades with a broker in the 1990s and it’s turned him off investing. “I was pretty disappointed over losing that money,” says Jake. “I don’t have the confidence to invest like that again.”

Two years ago, if you had asked Jake and Miranda Rodriguez about the secret to a happy marriage, they would have said “separate finances.” Jake, 38, a city planner in the Ontario government, earns $96,000 annually. Miranda, 35, is a social services worker who makes $84,000. They married in 2010. (We’ve changed their names to protect their privacy.) “We talked about our goals, took a pre-marriage course and discussed some ideas on how we would manage our money together,” says Miranda. “But talking about it and doing it are two different things. We both brought significant assets to the marriage and want to be fair. It’s harder to do than it sounds.”

The couple’s finances are in excellent shape. Both have worked full-time for over a dozen years and they’ve saved lots of cash in their RRSPs, TFSAs and other accounts, in addition to their solid government pensions. They have no debt. Miranda even owned a home mortgage-free—a small two-bedroom bungalow in Oshawa, Ont.—until she sold it this summer for $215,000. “The money I got for the house is now sitting in a savings account. Jake and I are renting a duplex apartment now and plan to buy a house together in three years.”

Why so far into the future? Because Jake plans to save $215,000 himself before the couple buys the house together. “We really want to make equal contributions to our new home,” says Miranda. “Jake says he will need three years to come up with his share so when he reaches that milestone, we’ll buy.”

This summer the couple sat down and worked out a system for their finances that allowed each to maintain some independence. As a result, they keep separate chequing* and savings accounts*, TFSAs*, RRSPs* and non-registered investment accounts, plus joint chequing and savings accounts used for several different purposes. “Even though all our bills are getting paid, we’re finding it’s overwhelming having all these accounts,” says Jake. “We really need to streamline our system, while at the same time being fair about where our money goes every month.”

While Jake and Miranda value their independence, they’re starting to feel they’re drifting without a joint financial plan. “Right now we have almost all of our money in cash in almost a dozen accounts,” says Miranda. “It’s not very efficient.” Each contributes $500 a month to a joint chequing account to pay household bills. They also contribute weekly to an individual savings account ($187.50 each), and make monthly contributions to TFSAs and RRSPs. “Until now we’ve used different accounts for different financial goals,” says Miranda. “But it’s getting a bit unwieldy.”

Another concern is they have no investment plan. “All our investments have produced lacklustre returns,” says Miranda. “The truth is we’re great savers but the money isn’t working for us at all.” They have almost $140,000 in RRSPs, largely invested in mutual funds. “Our returns on our mutual funds have been flat,” says Jake. Total it all up and the couple has more than $700,000 in liquid assets, most of it sitting in cash. “And our savings have given us next to nothing in interest. We want to do it right but don’t know where to start. It’s quite overwhelming.”

Miranda has started to investigate laddered GICs and exchange-traded funds (ETFs) as possible options, but hasn’t yet acted on it. “I want to be actively engaged in managing my money,” she says. “But Jake sees it differently.” That’s because Jake lost $12,000 on some stock trades with a broker in the 1990s and it’s turned him off investing. “I was pretty disappointed over losing that money,” says Jake. “I don’t have the confidence to invest like that again.”

In 10 years, Miranda dreams of working part-time and doing volunteer work. Jake is in no hurry to retire, though he’d like to keep travel a key part of the agenda. “I like my job and plan to work until 65,” he says. “I’ll support Miranda in anything she wants to do. We’re good savers and have two good pensions so I don’t think we’ll jeopardize a comfortable retirement by having her work part-time. Dealing with our money in the best way possible between now and then, and getting an investment plan in place, is the real issue for us.”

Miranda is especially anxious for that to happen. She’s always been keenly interested in money matters, having worked since age eight, when she shared a paper route with her brother. “My parents always encouraged us to work and earn our own money so we could pay for our own university costs and learn to invest,” says Miranda. “They were very entrepreneurial, owning four real estate rental properties over the years.”

Jake, meanwhile, comes from a single-parent household. “We never overindulged or owned any gadgets. We paid our bills on time, lived within our means and saved the rest. It worked for us.”

Jake has a Master’s in architecture from the University of Toronto, while Miranda graduated from Carleton University in Ottawa in 1999 with a degree in social work. For a decade she worked on several provincial government contracts, and three years ago was hired full-time in the social services department of the Ontario government in Oshawa. Jake has worked for the Ontario government for 13 years and finds the work challenging and rewarding. “It’s exactly the job I wanted when I finished my degree. I’m a lifer if they’ll have me.”

The Rodriguezes are now busy planning for six months of self-funded travel. While both have signed up for a sabbatical plan—work three years for 25% less and get the fourth year off at 75% of salary—they figure they’ll need another $50,000 for those six months of travel and have already saved much of it. “We spent an extended honeymoon on a trip around the world and wish we were still doing it,” says Miranda. “Travelling is our passion. We visited Hong Kong, Thailand, New Zealand, Vietnam and parts of Europe. It was fantastic.” For their dream trip they hope to visit Africa and parts of Asia missed on their last trip.

They have left one last unanswered question. “We’re still sitting on the fence about having kids,” says Miranda. “But my bet is we probably won’t, and that will be just fine with us. Our priority is to feel our financial life is in order. We want to feel safe and that we’re being fair with each other. If a long-term investment plan can do that for us, we’ll be extremely grateful.”

In 10 years, Miranda dreams of working part-time and doing volunteer work. Jake is in no hurry to retire, though he’d like to keep travel a key part of the agenda. “I like my job and plan to work until 65,” he says. “I’ll support Miranda in anything she wants to do. We’re good savers and have two good pensions so I don’t think we’ll jeopardize a comfortable retirement by having her work part-time. Dealing with our money in the best way possible between now and then, and getting an investment plan in place, is the real issue for us.”

Miranda is especially anxious for that to happen. She’s always been keenly interested in money matters, having worked since age eight, when she shared a paper route with her brother. “My parents always encouraged us to work and earn our own money so we could pay for our own university costs and learn to invest,” says Miranda. “They were very entrepreneurial, owning four real estate rental properties over the years.”

Jake, meanwhile, comes from a single-parent household. “We never overindulged or owned any gadgets. We paid our bills on time, lived within our means and saved the rest. It worked for us.”

Jake has a Master’s in architecture from the University of Toronto, while Miranda graduated from Carleton University in Ottawa in 1999 with a degree in social work. For a decade she worked on several provincial government contracts, and three years ago was hired full-time in the social services department of the Ontario government in Oshawa. Jake has worked for the Ontario government for 13 years and finds the work challenging and rewarding. “It’s exactly the job I wanted when I finished my degree. I’m a lifer if they’ll have me.”

The Rodriguezes are now busy planning for six months of self-funded travel. While both have signed up for a sabbatical plan—work three years for 25% less and get the fourth year off at 75% of salary—they figure they’ll need another $50,000 for those six months of travel and have already saved much of it. “We spent an extended honeymoon on a trip around the world and wish we were still doing it,” says Miranda. “Travelling is our passion. We visited Hong Kong, Thailand, New Zealand, Vietnam and parts of Europe. It was fantastic.” For their dream trip they hope to visit Africa and parts of Asia missed on their last trip.

They have left one last unanswered question. “We’re still sitting on the fence about having kids,” says Miranda. “But my bet is we probably won’t, and that will be just fine with us. Our priority is to feel our financial life is in order. We want to feel safe and that we’re being fair with each other. If a long-term investment plan can do that for us, we’ll be extremely grateful.”

Franklin suggests their overall investment portfolio should be about 70% equities (individual stocks and ETFs) to 30% fixed income (GICs and bond ETFs). That’s more aggressive than the Rodriguezes are used to, but it will give them a better chance of reaching their goals. “This conservative couple needs to understand the difference between volatility and risk,” says Ruth Hayden. “Volatility is just ups and downs in the market. Risk is similar to a car going off the road. They have to learn to live with a bit of volatility to get better returns for their money.”

To get their plan started properly, Miranda and Jake should go to a fee-only adviser who will build the investment portfolio with them. Then once a year they should check in with the adviser to make sure their investments are on track.

Buy the house in a year There’s no need for the couple to wait three years to buy their home, the experts say. They have a substantial down payment now. “Jake has never owned a home and he’s lost out on good gains because of it,” says Franklin. “A house is a good investment for them. If they wait until things look fair and equal, it will never happen.”

Draw up a marriage contract After all this, if the couple is still worried about being equal financial partners, they should have a lawyer draft a marriage contract. (This legal document is similar to a prenup, but is drawn up after the marriage.) “It will basically state what is hers, and what is his,” Hayden explains. “This approach gives clarity to partners who bring a lot of assets into a marriage and can’t help but wonder what will happen to those assets if they split up.”

The document should be one page long—quick and clean. “In this case, the couple can simply use Miranda’s $215,000 as a down payment on another home that will be jointly held by the two of them,” says Hayden. “Then they can pay the mortgage off together. The contract can simply state, ‘When we sell our house, the first $215,000 is Miranda’s and the rest of the gain will be split 50-50.’ She may miss out on a bit of gain, but that’s okay. The important thing is to be clear and tell yourself you can live with it. Then move on with your lives and be happy with each other. That’s the best thing for both of them.”

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto. For previous Family Profiles and other stories by Julie, please click here.

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected] If we use your story, your name will be changed to protect your privacy.

Franklin suggests their overall investment portfolio should be about 70% equities (individual stocks and ETFs) to 30% fixed income (GICs and bond ETFs). That’s more aggressive than the Rodriguezes are used to, but it will give them a better chance of reaching their goals. “This conservative couple needs to understand the difference between volatility and risk,” says Ruth Hayden. “Volatility is just ups and downs in the market. Risk is similar to a car going off the road. They have to learn to live with a bit of volatility to get better returns for their money.”

To get their plan started properly, Miranda and Jake should go to a fee-only adviser who will build the investment portfolio with them. Then once a year they should check in with the adviser to make sure their investments are on track.

Buy the house in a year There’s no need for the couple to wait three years to buy their home, the experts say. They have a substantial down payment now. “Jake has never owned a home and he’s lost out on good gains because of it,” says Franklin. “A house is a good investment for them. If they wait until things look fair and equal, it will never happen.”

Draw up a marriage contract After all this, if the couple is still worried about being equal financial partners, they should have a lawyer draft a marriage contract. (This legal document is similar to a prenup, but is drawn up after the marriage.) “It will basically state what is hers, and what is his,” Hayden explains. “This approach gives clarity to partners who bring a lot of assets into a marriage and can’t help but wonder what will happen to those assets if they split up.”

The document should be one page long—quick and clean. “In this case, the couple can simply use Miranda’s $215,000 as a down payment on another home that will be jointly held by the two of them,” says Hayden. “Then they can pay the mortgage off together. The contract can simply state, ‘When we sell our house, the first $215,000 is Miranda’s and the rest of the gain will be split 50-50.’ She may miss out on a bit of gain, but that’s okay. The important thing is to be clear and tell yourself you can live with it. Then move on with your lives and be happy with each other. That’s the best thing for both of them.”

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto. For previous Family Profiles and other stories by Julie, please click here.

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected] If we use your story, your name will be changed to protect your privacy.Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

Canadians may be tired of tipping culture, but newcomers are still trying to figure out the rules.

Financial advisors aren’t always necessary. Learn when you can DIY, when help adds value, and how to decide what’s...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...