What to do with a sudden inheritance

Diego just received a windfall. So why is he so miserable?

Advertisement

Diego just received a windfall. So why is he so miserable?

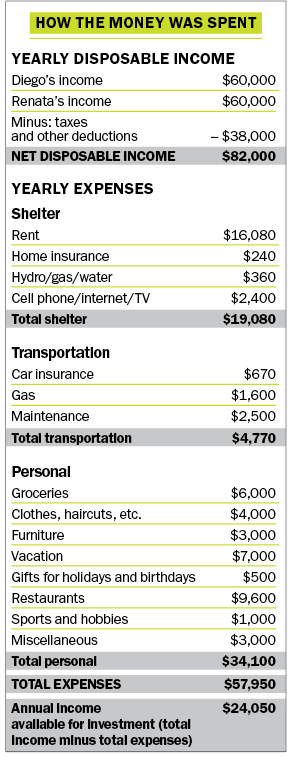

For now, Diego and Renata continue to rent a two-bedroom apartment in the Montreal neighbourhood they hold close to their hearts. “Both Renata’s parents and my own rented in this same neighbourhood all their lives and we grew up here too. We have no plans to leave,” says Diego, noting that he and his wife have known each other since elementary school. “If we ever bought a house, it will be here,” agrees Renata. But while the couple’s rent is modest (just $1,340 a month), the truth is that real estate prices for detached homes in their beloved stomping grounds are astronomical—from $1 million to $5 million.

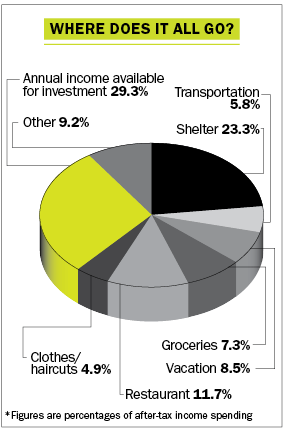

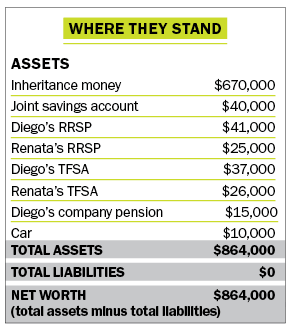

Right now, the Padillas earn $120,000 a year between them, and they have about $150,000 saved in RRSPs, TFSAs and a joint bank account. They had been planning to use most of their savings to make a 20% home down payment within the next five to 10 years. Living a simple lifestyle and following an ambitious savings plan has enabled them to get far ahead financially, given their relatively young ages. “We knew it would take us several years to save up a down payment but we’re patient,” says Renata, adding that they’re still putting $24,000 of their annual incomes into RRSPs and TFSAs.

Diego’s $670,000 inheritance, of course, now has the couple contemplating immediate home ownership—but only in fits and starts, as Diego vacillates on what course of action he should take. Believe it or not, his apprehension about what to do with hundreds of thousands of dollars of free money has even made for some sleepless nights in their household. “Honestly,” says Renata, “the inheritance complicates things for us.”

That the couple should even find themselves in such a position—deciding what do with Diego’s golden ticket—is fairly remarkable. Both Diego and Renata grew up modestly, and while there was always enough money to go around, both of their families shunned frivolous or unnecessary spending. Education, however, was a big priority, and it was at the University of Sherbrooke—Diego for engineering, Renata for business administration—that the couple’s relationship morphed from friendship into something much more special. “We discovered that we get along well and generally agree on everything,” says Diego. Three years ago, the couple had a big church wedding and then moved into their present rental apartment, where there’s now a lot of teeth-gnashing over what do with a big chunk of money.

For now, Diego and Renata continue to rent a two-bedroom apartment in the Montreal neighbourhood they hold close to their hearts. “Both Renata’s parents and my own rented in this same neighbourhood all their lives and we grew up here too. We have no plans to leave,” says Diego, noting that he and his wife have known each other since elementary school. “If we ever bought a house, it will be here,” agrees Renata. But while the couple’s rent is modest (just $1,340 a month), the truth is that real estate prices for detached homes in their beloved stomping grounds are astronomical—from $1 million to $5 million.

Right now, the Padillas earn $120,000 a year between them, and they have about $150,000 saved in RRSPs, TFSAs and a joint bank account. They had been planning to use most of their savings to make a 20% home down payment within the next five to 10 years. Living a simple lifestyle and following an ambitious savings plan has enabled them to get far ahead financially, given their relatively young ages. “We knew it would take us several years to save up a down payment but we’re patient,” says Renata, adding that they’re still putting $24,000 of their annual incomes into RRSPs and TFSAs.

Diego’s $670,000 inheritance, of course, now has the couple contemplating immediate home ownership—but only in fits and starts, as Diego vacillates on what course of action he should take. Believe it or not, his apprehension about what to do with hundreds of thousands of dollars of free money has even made for some sleepless nights in their household. “Honestly,” says Renata, “the inheritance complicates things for us.”

That the couple should even find themselves in such a position—deciding what do with Diego’s golden ticket—is fairly remarkable. Both Diego and Renata grew up modestly, and while there was always enough money to go around, both of their families shunned frivolous or unnecessary spending. Education, however, was a big priority, and it was at the University of Sherbrooke—Diego for engineering, Renata for business administration—that the couple’s relationship morphed from friendship into something much more special. “We discovered that we get along well and generally agree on everything,” says Diego. Three years ago, the couple had a big church wedding and then moved into their present rental apartment, where there’s now a lot of teeth-gnashing over what do with a big chunk of money.

Renata, who is sensitive to Diego’s concerns about his inheritance, has suggested combining the money they’ve already saved together with a smaller portion of her husband’s newfound wealth—just enough to enable them to put a 40% down payment on a house (say $400,000 or so), and then mortgage the rest. “I like the idea of both of us contributing money to the purchase of a home,” says Renata. “I want Diego to always feel his inheritance is his own and whatever he decides is fine with me.”

A different option Diego is considering is to simply keep going with their original plan of saving up for a down payment of 20% with money from their job incomes. In the meantime, the couple would continue to rent, and Diego would invest his $670,000 inheritance on his own, thereby leaving it safely set aside for future use. That option, however, leaves him wondering about the right way to invest the money. “I’ve picked some bank stocks on my own recently,” says Diego, who has been reading up on investing for several months now. “However, I’ve realized that I don’t like a lot of volatility and I’d kick myself if I lost the money in a market crash. So if we decided to invest this money instead of buying a home, I’d probably need an adviser’s help to manage it.” But even that decision makes him anxious because he’s not sure how to pick a qualified professional. “Right now, I think markets are very high so I feel paralyzed. I don’t want to make a mistake with any of our savings and investments.”

Diego’s lack of confidence in managing the money then brings his conundrum full circle: Should he just buy the house outright and be done with it? It’s a simple choice, he says, not to mention a solid investment for their future. “The money will be safely tucked into the equity in my home. I like that,” he says. “The risk, of course, is if Renata and I divorce and I lose half the money. That thought keeps me up at night.” And so the cycle continues.

Thankfully, Renata and Diego have a pleasant diversion from all of this indecision over money: the impending birth of their first child. Whatever Diego decides to do with the money, says Renata, is ultimately not a big concern. “We’re lucky,” she says. “We live very simply and don’t even spend what we earn now. Plus, our daycare bills will be tiny because we have two sets of grandparents a few blocks away anxious to watch the baby when I return to work.”

Thinking about all that he’s blessed to have in his life makes Diego realize it’s now time to make a definitive decision about what to do with his inheritance—for his own peace of mind, as well as his wife’s. “We have a really nice life together now. I’m lucky to have found Renata. I don’t want to mess that up.”

Renata, who is sensitive to Diego’s concerns about his inheritance, has suggested combining the money they’ve already saved together with a smaller portion of her husband’s newfound wealth—just enough to enable them to put a 40% down payment on a house (say $400,000 or so), and then mortgage the rest. “I like the idea of both of us contributing money to the purchase of a home,” says Renata. “I want Diego to always feel his inheritance is his own and whatever he decides is fine with me.”

A different option Diego is considering is to simply keep going with their original plan of saving up for a down payment of 20% with money from their job incomes. In the meantime, the couple would continue to rent, and Diego would invest his $670,000 inheritance on his own, thereby leaving it safely set aside for future use. That option, however, leaves him wondering about the right way to invest the money. “I’ve picked some bank stocks on my own recently,” says Diego, who has been reading up on investing for several months now. “However, I’ve realized that I don’t like a lot of volatility and I’d kick myself if I lost the money in a market crash. So if we decided to invest this money instead of buying a home, I’d probably need an adviser’s help to manage it.” But even that decision makes him anxious because he’s not sure how to pick a qualified professional. “Right now, I think markets are very high so I feel paralyzed. I don’t want to make a mistake with any of our savings and investments.”

Diego’s lack of confidence in managing the money then brings his conundrum full circle: Should he just buy the house outright and be done with it? It’s a simple choice, he says, not to mention a solid investment for their future. “The money will be safely tucked into the equity in my home. I like that,” he says. “The risk, of course, is if Renata and I divorce and I lose half the money. That thought keeps me up at night.” And so the cycle continues.

Thankfully, Renata and Diego have a pleasant diversion from all of this indecision over money: the impending birth of their first child. Whatever Diego decides to do with the money, says Renata, is ultimately not a big concern. “We’re lucky,” she says. “We live very simply and don’t even spend what we earn now. Plus, our daycare bills will be tiny because we have two sets of grandparents a few blocks away anxious to watch the baby when I return to work.”

Thinking about all that he’s blessed to have in his life makes Diego realize it’s now time to make a definitive decision about what to do with his inheritance—for his own peace of mind, as well as his wife’s. “We have a really nice life together now. I’m lucky to have found Renata. I don’t want to mess that up.”

Buy the house sooner. The Padillas were planning to buy a home even before Diego received his inheritance. But they were planning to do it in five to 10 years when they had saved up a 20% down payment. Moving that purchase up and buying the house in two to three years is the right thing to do. “They should continue saving as much as they can together from their own incomes and when they have $200,000 saved up—in two years or so—they should buy the house,” says Terekhova, adding that the additional $200,000 required to make a 40% down payment will come from Diego’s inheritance.

If Diego is hesitant to do this, he needs to appreciate the bigger picture. Putting some of his inheritance toward the purchase of a home will be crucial if he wants to maintain a happy marriage—not to mention diversify his investments. All of our experts believe it’s important that Diego show some generosity to his wife. “If he doesn’t contribute any part of the inheritance to the purchase of the home, it will always be the elephant in the room,” says Terekhova. “That would cause more strife in their marriage than simply sharing some of it.”

However, Diego will need to keep in mind that if they divorce, he could lose some of his inheritance money. In most Canadian provinces, proceeds from the sale of the family home are split 50-50, regardless of where the money came from. In Quebec, inheritance money is protected, but he would have to prove that’s where his down payment contribution came from. “He can get a notarized document stating explicitly that he made a contribution from his inheritance towards the purchase of the matrimonial home that is being registered in both their names,” says Caroline Nalbantoglu, president of CNal Financial Planning in Montreal. Even then, a lawyer could order him to split that money with his wife in certain situations, so there’s no guarantee.

Divorce issues aside, Diego and Renata should feel good about this plan because it ensures they’re sharing the responsibility of the purchase and ongoing mortgage together. “It’s important for the two of them to feel that they are both contributing,” says Terekhova. “Sure, they could buy the house for cash now and be mortgage-free with a $1-million home, but then what do they have to strive for? They’re only in their 30s. It’s working together that will keep their relationship healthy.”

With a $400,000 down payment, the Padillas will be able to carry their $600,000 mortgage comfortably using only their salaries. “Children change your life,” says Nalbantoglu. “Some of the money saved from lower restaurant and vacation costs can be used to offset higher home maintenance expenses.”

Invest the rest. Diego should keep the remaining $470,000 in a self-directed investment account. That way, it will remain his—even if they get divorced. “Just maintain a clear paper trail that this is his inheritance money,” says Forward. Diego should also find an adviser to help him manage his money. “He likes investing, but emotionally, he panics,” says Forward. He can search for a planner at moneysense.ca/planners and interview two or three before deciding who he will hire. “He should pay attention to fees and designations, and have a thorough risk assessment done,” says Forward. Once Diego has found someone he’s comfortable with, he should put the money away for a long-term goal, like retirement. “Even with a low-risk portfolio invested 50% in bonds and 50% in stocks, an average net annual return of 4% is attainable with very little risk,” says Terekhova.

Don’t forget taxes. Interest and dividends from the inheritance will be a tax liability for him. Diego should top up his RRSP and TFSA, if he has any allowable contribution room, to mitigate some of the taxes payable in the years ahead.

Review their wills. The Padillas need to update their wills, name a power of attorney and choose a guardian for their child. They should also pay attention to one other detail. “Diego needs to specify who he’d like to bequeath his inheritance money to in the investment account, because if he doesn’t name Renata specifically in the will, she won’t get it,” says Terekhova. “Or, he may choose to leave it to his child. It’s totally up to him.”

Going forward, Renata can keep investing $900 a month in her own RRSP as she’s been doing all along. This will be her retirement nest egg. As for their $1-million principal residence, it will likely keep going up in value by 2% or 3% a year. “Those gains will be totally tax-free,” says Nalbantoglu. “By their early 60s, they’ll have a house worth $2 million or more, a retirement nest egg for Diego worth $1.2 million and about $650,000 for Renata in her RRSP. If they do all this, they will look back at this time in their lives, and at Diego’s inheritance, as truly a wonderful gift.”

Buy the house sooner. The Padillas were planning to buy a home even before Diego received his inheritance. But they were planning to do it in five to 10 years when they had saved up a 20% down payment. Moving that purchase up and buying the house in two to three years is the right thing to do. “They should continue saving as much as they can together from their own incomes and when they have $200,000 saved up—in two years or so—they should buy the house,” says Terekhova, adding that the additional $200,000 required to make a 40% down payment will come from Diego’s inheritance.

If Diego is hesitant to do this, he needs to appreciate the bigger picture. Putting some of his inheritance toward the purchase of a home will be crucial if he wants to maintain a happy marriage—not to mention diversify his investments. All of our experts believe it’s important that Diego show some generosity to his wife. “If he doesn’t contribute any part of the inheritance to the purchase of the home, it will always be the elephant in the room,” says Terekhova. “That would cause more strife in their marriage than simply sharing some of it.”

However, Diego will need to keep in mind that if they divorce, he could lose some of his inheritance money. In most Canadian provinces, proceeds from the sale of the family home are split 50-50, regardless of where the money came from. In Quebec, inheritance money is protected, but he would have to prove that’s where his down payment contribution came from. “He can get a notarized document stating explicitly that he made a contribution from his inheritance towards the purchase of the matrimonial home that is being registered in both their names,” says Caroline Nalbantoglu, president of CNal Financial Planning in Montreal. Even then, a lawyer could order him to split that money with his wife in certain situations, so there’s no guarantee.

Divorce issues aside, Diego and Renata should feel good about this plan because it ensures they’re sharing the responsibility of the purchase and ongoing mortgage together. “It’s important for the two of them to feel that they are both contributing,” says Terekhova. “Sure, they could buy the house for cash now and be mortgage-free with a $1-million home, but then what do they have to strive for? They’re only in their 30s. It’s working together that will keep their relationship healthy.”

With a $400,000 down payment, the Padillas will be able to carry their $600,000 mortgage comfortably using only their salaries. “Children change your life,” says Nalbantoglu. “Some of the money saved from lower restaurant and vacation costs can be used to offset higher home maintenance expenses.”

Invest the rest. Diego should keep the remaining $470,000 in a self-directed investment account. That way, it will remain his—even if they get divorced. “Just maintain a clear paper trail that this is his inheritance money,” says Forward. Diego should also find an adviser to help him manage his money. “He likes investing, but emotionally, he panics,” says Forward. He can search for a planner at moneysense.ca/planners and interview two or three before deciding who he will hire. “He should pay attention to fees and designations, and have a thorough risk assessment done,” says Forward. Once Diego has found someone he’s comfortable with, he should put the money away for a long-term goal, like retirement. “Even with a low-risk portfolio invested 50% in bonds and 50% in stocks, an average net annual return of 4% is attainable with very little risk,” says Terekhova.

Don’t forget taxes. Interest and dividends from the inheritance will be a tax liability for him. Diego should top up his RRSP and TFSA, if he has any allowable contribution room, to mitigate some of the taxes payable in the years ahead.

Review their wills. The Padillas need to update their wills, name a power of attorney and choose a guardian for their child. They should also pay attention to one other detail. “Diego needs to specify who he’d like to bequeath his inheritance money to in the investment account, because if he doesn’t name Renata specifically in the will, she won’t get it,” says Terekhova. “Or, he may choose to leave it to his child. It’s totally up to him.”

Going forward, Renata can keep investing $900 a month in her own RRSP as she’s been doing all along. This will be her retirement nest egg. As for their $1-million principal residence, it will likely keep going up in value by 2% or 3% a year. “Those gains will be totally tax-free,” says Nalbantoglu. “By their early 60s, they’ll have a house worth $2 million or more, a retirement nest egg for Diego worth $1.2 million and about $650,000 for Renata in her RRSP. If they do all this, they will look back at this time in their lives, and at Diego’s inheritance, as truly a wonderful gift.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Why two people at the same life stage can be years apart financially, and how timing, housing, immigration and...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...

Why do we know we're overpaying and still do nothing about it? A personal look at loyalty, inertia, and...

The biggest financial barrier for newcomers isn't always knowledge, but understanding how familiar words take on new meanings...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

I was told that I am the beneficiary of my girlfriend estate and all assets and company and the inheritance of her died father estate as well I have never had to deal with anything like this in my life and I was told I would have to pay 6000.00dollars fees to have the propertys and ownership transfer into my name on the inheritance of her father’s property and money of the sum of 50 million dollars I am no shore if this is not even a scam or legitimate true will how can I find out I need help with finding out

Ralph, we do not have the capacity to help you, but we did want to let you know that there are several online scams of this nature and you should be very careful. Please find a trusted friend / relative or advisor who can help you.