A low-fee portfolio for DIY investors

He knows keeping a lid on fees will net better returns

Advertisement

He knows keeping a lid on fees will net better returns

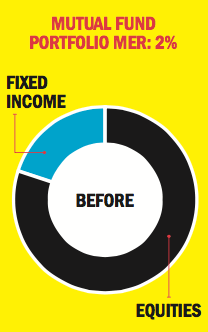

Gino Marcone, 49, is a regional sales manager who has spent the last three years working with an advisor at his local Guelph, Ont. bank to build his retirement nest egg. He recently learned he’s paying 2% annually in management expense ratios (MERs) on his plain vanilla mutual fund portfolio—that’s $5,000 in fees paid each year on his six-figure savings plan. “I tried to negotiate better fees but my advisor wasn’t able to help, so I decided to help myself,” says Marcone. He opened an online trading account and now wants to build a low-fee portfolio using index or exchange-traded funds (ETFs). “I’d like to add $20,000 each year until retirement.”

Gino Marcone, 49, is a regional sales manager who has spent the last three years working with an advisor at his local Guelph, Ont. bank to build his retirement nest egg. He recently learned he’s paying 2% annually in management expense ratios (MERs) on his plain vanilla mutual fund portfolio—that’s $5,000 in fees paid each year on his six-figure savings plan. “I tried to negotiate better fees but my advisor wasn’t able to help, so I decided to help myself,” says Marcone. He opened an online trading account and now wants to build a low-fee portfolio using index or exchange-traded funds (ETFs). “I’d like to add $20,000 each year until retirement.”

Even though Marcone started investing just three years ago he’s done a lot of things right, says Ayana Forward, a certified financial planner with Ryan Lamontagne in Ottawa. “He’s worked hard to maximize his RRSP and TFSA and he’s off to a great start.” But she agrees it’s time to switch out of those high-fee mutual funds

Forward says Marcone can save a lot of money—about $4,600 annually—by switching to a lower-fee, all-ETF portfolio. “But if this plan is to succeed, he needs to be comfortable with rebalancing the portfolio himself,” says Forward. “His risk tolerance, time horizon and goals will all play a key role in building a portfolio that is suitable for his needs.”

Forward recommends Marcone keep it simple with a long-term, passive investment strategy that uses BlackRock’s iShares Core series of ETFs with MERs as low as 0.06%. For the time being, he can keep his current asset allocation of 80% equities and 20% fixed income, since it’s appropriate for Marcone’s risk tolerance. Because his time horizon is 20 years or more, he can afford to be more aggressive with his investments.

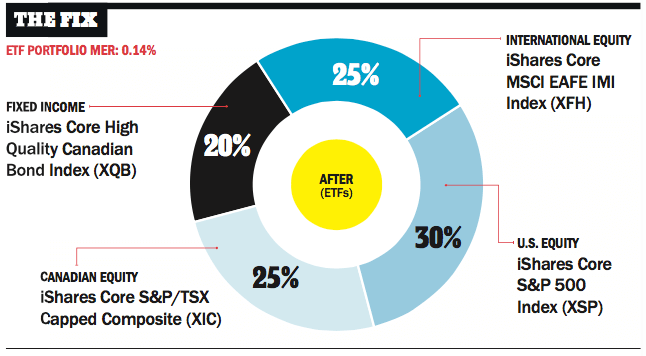

To do this, he should allocate 25% of his portfolio to Canadian equities, 30% to U.S. equities, 25% to international equities and the remaining 20% to fixed-income investments. “Once a year, when Gino makes his $20,000 contribution to his investments, he can use the money to rebalance his portfolio back to this original allocation,” says Forward. “He’s a disciplined saver, so regular savings plus reduced fees will give him the good growth he seeks until retirement at age 65.”

Even though Marcone started investing just three years ago he’s done a lot of things right, says Ayana Forward, a certified financial planner with Ryan Lamontagne in Ottawa. “He’s worked hard to maximize his RRSP and TFSA and he’s off to a great start.” But she agrees it’s time to switch out of those high-fee mutual funds

Forward says Marcone can save a lot of money—about $4,600 annually—by switching to a lower-fee, all-ETF portfolio. “But if this plan is to succeed, he needs to be comfortable with rebalancing the portfolio himself,” says Forward. “His risk tolerance, time horizon and goals will all play a key role in building a portfolio that is suitable for his needs.”

Forward recommends Marcone keep it simple with a long-term, passive investment strategy that uses BlackRock’s iShares Core series of ETFs with MERs as low as 0.06%. For the time being, he can keep his current asset allocation of 80% equities and 20% fixed income, since it’s appropriate for Marcone’s risk tolerance. Because his time horizon is 20 years or more, he can afford to be more aggressive with his investments.

To do this, he should allocate 25% of his portfolio to Canadian equities, 30% to U.S. equities, 25% to international equities and the remaining 20% to fixed-income investments. “Once a year, when Gino makes his $20,000 contribution to his investments, he can use the money to rebalance his portfolio back to this original allocation,” says Forward. “He’s a disciplined saver, so regular savings plus reduced fees will give him the good growth he seeks until retirement at age 65.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

ETFS

Canadian investors should look beyond the border for diversification, given that Canada represents just a small part of the...

ETFs

The MoneySense Best ETFs 2026 panel suggests what to look at for the best exchange-traded funds that own companies...

ETFs

The 2026 MoneySense Best ETFs panel’s picks for the best exchange-traded funds focused on Canadian stocks.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

ETFS

Back for the 14th edition, here are the top exchange-traded funds among Canadian, U.S., international, fixed income, cash alternative,...

ETFs

The MoneySense 2026 Best ETF panellists each pick a fund they’d leave in their portfolios if they were stranded...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Low trading volume does not necessarily mean low liquidity. Here’s what actually determines how easy it is to buy...

Vanguard’s VRIF ETF is tilting toward bonds to provide retirees stable income, balancing caution with a 4% annual payout...