The problem with having too much equity

The Silverbergs want to move their 100% equity portfolio into low-cost ETFs. Is it the right choice for them?

Advertisement

The Silverbergs want to move their 100% equity portfolio into low-cost ETFs. Is it the right choice for them?

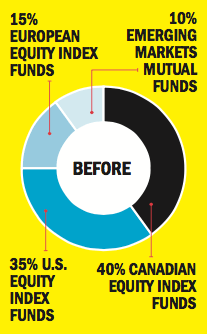

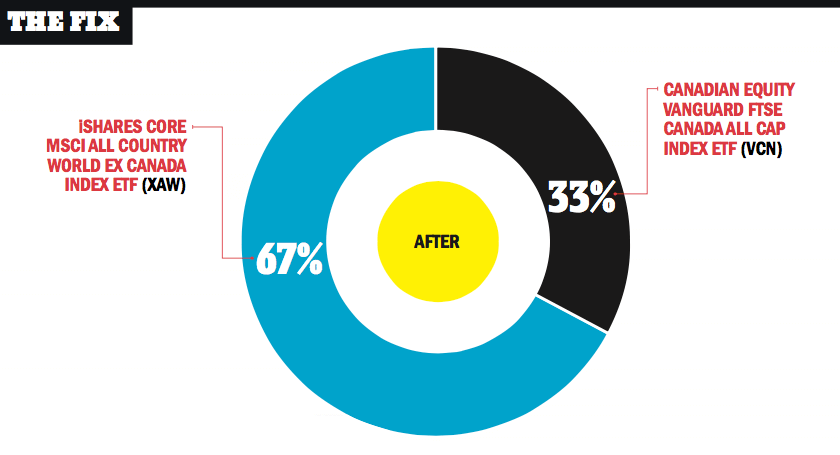

For the past 18 years, Karine and Dave Silverberg of Milton, Ont., have managed their own portfolio of mutual funds. Neither has a company pension so the 38-year-old couple has been very aggressive with asset allocation. “Up to now, we’ve been 100% in equities,” says Karine, who oversees their six-figure portfolio to which they contribute $4,000 a month. All their investments are in index funds with fees of up to 1.1%. The couple now wants to switch to lower-fee exchange-traded funds (ETFs), but is starting to question their 100% equity position. “Is it right for the long term?” asks Karine. “We won’t need the money for years.”

For the past 18 years, Karine and Dave Silverberg of Milton, Ont., have managed their own portfolio of mutual funds. Neither has a company pension so the 38-year-old couple has been very aggressive with asset allocation. “Up to now, we’ve been 100% in equities,” says Karine, who oversees their six-figure portfolio to which they contribute $4,000 a month. All their investments are in index funds with fees of up to 1.1%. The couple now wants to switch to lower-fee exchange-traded funds (ETFs), but is starting to question their 100% equity position. “Is it right for the long term?” asks Karine. “We won’t need the money for years.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

Canadian investors have several options for investing in bitcoin and other cryptocurrencies. Here are the pros and cons of...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

RBC Direct Investing has introduced commission-free trades on 50 exchange-traded funds (ETFs) from partner iShares.

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...