How to avoid a value trap

Here's a strategy that spots cheap stocks that are on the way up

Advertisement

Here's a strategy that spots cheap stocks that are on the way up

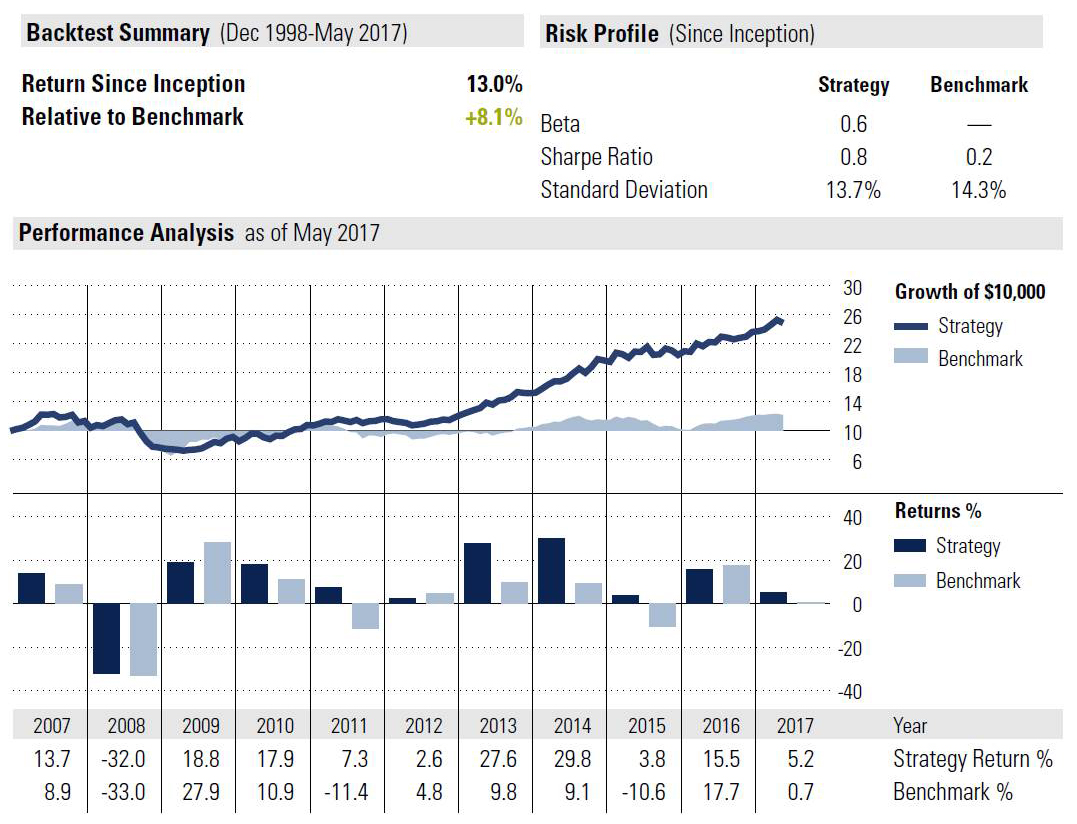

As always, investors are encouraged to conduct their own independent research before purchasing any of the investments listed here:

As always, investors are encouraged to conduct their own independent research before purchasing any of the investments listed here:

| Rank | Company | Forward P/E Relative to Sector Median | P/Book Relative to Sector Median | P/Cashflow Relative to Sector Median | P/Sales Relative to Sector Median | 3M Price Momentum (%) | Quarterly Earnings Momentum (%) | Earnings Surprise (%) | 5Y EPS Growth (%) |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Cdn Tire Corp. Ltd. (CTC.A) | 0.9 | 0.8 | 1.0 | 0.5 | 7.6 | 4.6 | 14.9 | 8.2 |

| 2 | Magna Intl. Inc. (MG) | 0.5 | 0.6 | 0.5 | 0.3 | 1.6 | 5.4 | 7.4 | 30.0 |

| 3 | Manulife Financial Corp (MFC) | 0.9 | 0.7 | 0.3 | 0.4 | 4.2 | 4.5 | 0.0 | 31.6 |

| 4 | Weston Ltd., George (WN) | 1.0 | 0.6 | 0.3 | 0.4 | 4.4 | 2.2 | 2.0 | 12.5 |

| 5 | Loblaw Companies Ltd. (L) | 1.0 | 0.6 | 0.6 | 0.8 | 4.6 | 2.0 | 0.0 | 11.3 |

| 6 | National Bank of Canada (NA) | 0.9 | 1.1 | 1.0 | 1.0 | 4.2 | 3.2 | 0.3 | 6.1 |

| 7 | Metro Inc. (MRU) | 0.9 | 1.0 | 1.0 | 1.0 | 3.4 | 2.0 | 1.8 | 12.3 |

| 8 | Bank of Montreal (BMO) | 1.0 | 0.9 | 1.0 | 1.0 | 3.9 | 2.4 | 0.0 | 6.8 |

| 9 | Fortis Inc. (FTS) | 1.0 | 0.9 | 0.9 | 1.1 | 3.1 | 2.6 | -0.2 | 7.2 |

| 10 | TELUS Corporation (T) | 0.9 | 1.0 | 0.9 | 0.9 | 2.7 | 1.4 | 1.3 | 7.1 |

| 11 | CGI Group Inc., A (GIB.A) | 0.7 | 1.0 | 0.6 | 0.4 | 1.1 | 0.4 | 0.0 | 20.9 |

| 12 | BCE Inc. (BCE) | 1.0 | 1.0 | 1.0 | 1.0 | 1.5 | 0.1 | 0.0 | 3.1 |

| 13 | Emera Inc. (EMA) | 1.0 | 1.1 | 1.1 | 0.9 | 1.8 | -8.4 | 0.0 | 13.1 |

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Cogeco’s Canadian wireless launch arrives amid downgraded outlook, falling U.S. revenue, and analyst concerns.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

Canadian investors have several options for investing in bitcoin and other cryptocurrencies. Here are the pros and cons of...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

These top 10 Canadian momentum stocks all returned more than 40% over the past three months.

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...