Investors see value, but why won’t they act on it?

Investors continue to favour higher-fee active investments when lower-fee passive strategies are clearly better for them

Advertisement

Investors continue to favour higher-fee active investments when lower-fee passive strategies are clearly better for them

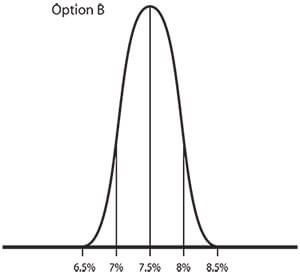

Option B (Beta-replicating) is predicated on mimicking a market.

Option B (Beta-replicating) is predicated on mimicking a market.

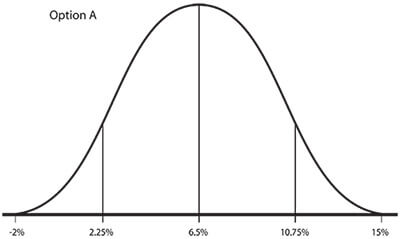

In my examples I’ll use a market return of 8% and then deduct the average cost of the products to determine the expected market return. Let’s assume that traditional active products (for example, F Class mutual funds) cost 1.5% and traditional passive products (for example, market-tracking ETFs) cost 0.5%. Those costs are likely a bit high, but the important thing to note here is that the difference in cost is about 1 percentage point.

In my examples I’ll use a market return of 8% and then deduct the average cost of the products to determine the expected market return. Let’s assume that traditional active products (for example, F Class mutual funds) cost 1.5% and traditional passive products (for example, market-tracking ETFs) cost 0.5%. Those costs are likely a bit high, but the important thing to note here is that the difference in cost is about 1 percentage point.

![]()

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Whether for income or day trading, these ETFs are more complex and potentially risky products than they first appear....

Thinking about selling a property that’s not currently your primary residence? Knowing its value is essential to calculating—and not...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Cogeco’s Canadian wireless launch arrives amid downgraded outlook, falling U.S. revenue, and analyst concerns.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

Canadian investors have several options for investing in bitcoin and other cryptocurrencies. Here are the pros and cons of...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...