Family profile: Pulling up their roots

Pierre and Jackie have worked hard and lived modestly in rural Quebec. Now that Jackie has lost her job, they wonder if it’s time to sell their 117-acre farm so they can enjoy the fruits of an early retirement.

Advertisement

Pierre and Jackie have worked hard and lived modestly in rural Quebec. Now that Jackie has lost her job, they wonder if it’s time to sell their 117-acre farm so they can enjoy the fruits of an early retirement.

Jackie and Pierre realize that withdrawing $40,000 or so from their RRSP would exhaust those savings in less than three years. But taking money out of the RRSP to cover the annual difference seems like the easiest option. “The $13,000 we have in our savings and chequing accounts is earmarked for renovations on the cottage we inherited,” says Pierre. “It’s worth about $115,000 and we can rent it for $8,000 a year when the renovations are done. But I’m not sure we really want to be landlords at this stage of our lives.” In fact, the couple acknowledges they may be better off just selling it.

Jackie, who has always managed the family’s money, has worked hard to pay down the mortgage on their farm, even when Pierre insisted on buying his toys. “Five years ago he bought a boat, and then shortly afterwards he bought a plane so he and our daughter could take flying lessons,” says Jackie. “I made sure we could pay for those in cash.”

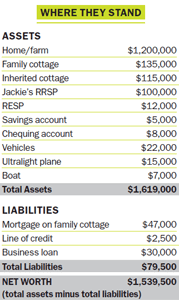

These days, Jackie is taking a much more hands-on approach with their investments. The $100,000 in her RRSP is invested in mutual funds, but she’s in the process of switching to exchange-traded funds to save on costs. The couple would also like to eliminate their $80,000 debt and make a final decision on what to do with the cottage they inherited. “That cottage may be our escape hatch,” says Pierre. “We could rent it out or sell it. It’s tough to know which is really best for our bottom line.”The couple married in 1989 and bought the farm shortly afterwards. Jackie got her job as an estimator and her full-time income over the years has allowed the family to live comfortably. But while she paid down the mortgage, shopped frugally for groceries, clothes and insurance and tried to put some money in savings, she and Pierre seldom took an interest in investing until the last few years. So while selling the farm will be a bonanza, their biggest question is how to invest the proceeds. “Once the kids are gone, we know we could live on $40,000 net a year,” says Pierre, who wonders whether the $1.2 million can generate that kind of income for the rest of their lives.

Jackie and Pierre realize that withdrawing $40,000 or so from their RRSP would exhaust those savings in less than three years. But taking money out of the RRSP to cover the annual difference seems like the easiest option. “The $13,000 we have in our savings and chequing accounts is earmarked for renovations on the cottage we inherited,” says Pierre. “It’s worth about $115,000 and we can rent it for $8,000 a year when the renovations are done. But I’m not sure we really want to be landlords at this stage of our lives.” In fact, the couple acknowledges they may be better off just selling it.

Jackie, who has always managed the family’s money, has worked hard to pay down the mortgage on their farm, even when Pierre insisted on buying his toys. “Five years ago he bought a boat, and then shortly afterwards he bought a plane so he and our daughter could take flying lessons,” says Jackie. “I made sure we could pay for those in cash.”

These days, Jackie is taking a much more hands-on approach with their investments. The $100,000 in her RRSP is invested in mutual funds, but she’s in the process of switching to exchange-traded funds to save on costs. The couple would also like to eliminate their $80,000 debt and make a final decision on what to do with the cottage they inherited. “That cottage may be our escape hatch,” says Pierre. “We could rent it out or sell it. It’s tough to know which is really best for our bottom line.”The couple married in 1989 and bought the farm shortly afterwards. Jackie got her job as an estimator and her full-time income over the years has allowed the family to live comfortably. But while she paid down the mortgage, shopped frugally for groceries, clothes and insurance and tried to put some money in savings, she and Pierre seldom took an interest in investing until the last few years. So while selling the farm will be a bonanza, their biggest question is how to invest the proceeds. “Once the kids are gone, we know we could live on $40,000 net a year,” says Pierre, who wonders whether the $1.2 million can generate that kind of income for the rest of their lives.

When they finally sell the farm, they’d like to make the family cottage their primary residence. But they won’t do that until they feel confident their nest egg from the farm will be invested wisely. “Somehow having $1.2 million in a bank somewhere doesn’t feel very secure to us,” says Pierre. “It’s strange, because we’re farmers for crying out loud, and farming is the riskiest thing you can do. But we can’t afford for the money to run out. So we really need the right income-producing strategy and we need to feel fully comfortable with it. When we do that, we can relax and start enjoying life.”

When they finally sell the farm, they’d like to make the family cottage their primary residence. But they won’t do that until they feel confident their nest egg from the farm will be invested wisely. “Somehow having $1.2 million in a bank somewhere doesn’t feel very secure to us,” says Pierre. “It’s strange, because we’re farmers for crying out loud, and farming is the riskiest thing you can do. But we can’t afford for the money to run out. So we really need the right income-producing strategy and we need to feel fully comfortable with it. When we do that, we can relax and start enjoying life.”

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto.

Would you like MoneySense to consider your financial situation in a future family profile? Drop us a line at [email protected] If we use your story, your name will be changed to protect your privacy.

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto.

Would you like MoneySense to consider your financial situation in a future family profile? Drop us a line at [email protected] If we use your story, your name will be changed to protect your privacy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Now’s the time to help pay for their education

It's time to discuss how they can start saving for larger purchases

Now's the time to toss the piggy bank and open a bank account instead

It's important to start teaching your kids about money early

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...