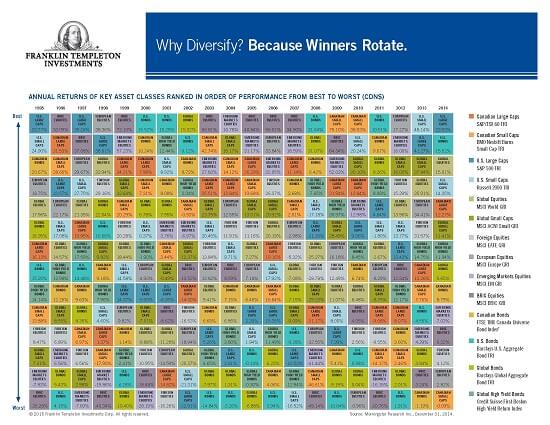

Why diversify? This chart shows you why

Annual returns of key asset classes ranked from best to worst

Advertisement

Annual returns of key asset classes ranked from best to worst

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Young Canadians are building wealth by buying “boring” businesses from Boomers. Here’s why laundromats, trades, and car washes are...

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

The co-founder of online prenuptial agreement startup Jointly talks about leaving Big Law, tracking spending as a system, and...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

What Canadians need to know about stablecoins, possible coins from Amazon and Walmart, and Canada launches three XRP ETFs.

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Created By

Ratehub