Money for the taking

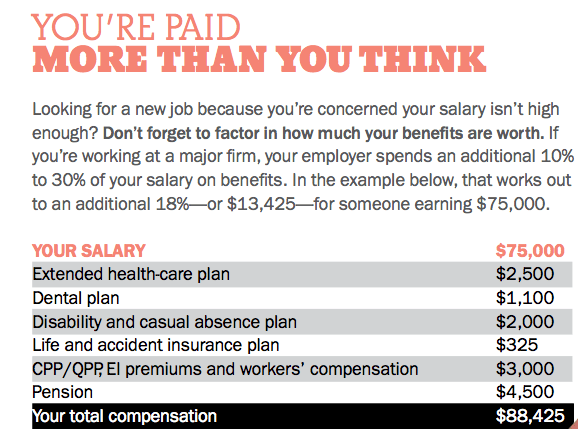

Employee benefits worth thousands of dollars could add 18% to your pay

Advertisement

Employee benefits worth thousands of dollars could add 18% to your pay

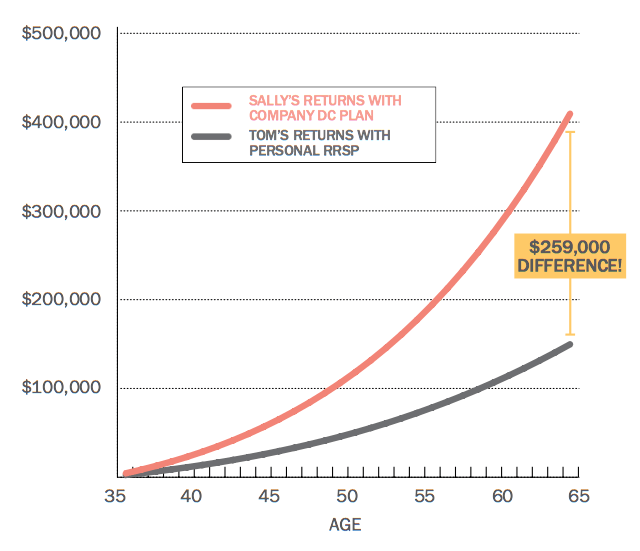

Still, some people are hesitant to opt into any type of workplace program simply because they don’t trust their employer or the pension plan itself. That mistrust is unwarranted. Fred Vettese, chief actuary of Morneau Shepell, explains that defined contributions go into a trust fund that’s protected, even if the employer goes bankrupt. Although the investments reflect the market and will rise and fall like any other investment, poor employer performance won’t affect it. A lot of skeptical employees may also think there’s a catch when it comes to matching contributions in pension plans. (There’s not.)

But here’s some good news for pension procrastinators: If you haven’t previously enrolled in your company’s plan, some employers will allow you to “buy back” contribution room you’re eligible for. In other words, if you worked for one year before signing up, you might be allowed to contribute a set amount based on your salary and age. In some cases, the same applies to other periods when you may not have paid into the plan. These include: unpaid leaves of absence, maternity and parental leaves, or even periods of seasonal and contract employment before you were allowed to buy into the pension plan.

Buying back unused room not only increases the annual pension total, but could even allow you to retire a year or two early. Not sure if your company’s plan allows buybacks? If in doubt, ask.

Still, some people are hesitant to opt into any type of workplace program simply because they don’t trust their employer or the pension plan itself. That mistrust is unwarranted. Fred Vettese, chief actuary of Morneau Shepell, explains that defined contributions go into a trust fund that’s protected, even if the employer goes bankrupt. Although the investments reflect the market and will rise and fall like any other investment, poor employer performance won’t affect it. A lot of skeptical employees may also think there’s a catch when it comes to matching contributions in pension plans. (There’s not.)

But here’s some good news for pension procrastinators: If you haven’t previously enrolled in your company’s plan, some employers will allow you to “buy back” contribution room you’re eligible for. In other words, if you worked for one year before signing up, you might be allowed to contribute a set amount based on your salary and age. In some cases, the same applies to other periods when you may not have paid into the plan. These include: unpaid leaves of absence, maternity and parental leaves, or even periods of seasonal and contract employment before you were allowed to buy into the pension plan.

Buying back unused room not only increases the annual pension total, but could even allow you to retire a year or two early. Not sure if your company’s plan allows buybacks? If in doubt, ask.

WATCH: WTF is an Employe Stock Plan?[bc_video video_id=”6023926376001″ account_id=”6015698167001″ player_id=”lYro6suIR”]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Canada’s proposed Groceries and Essentials Benefit could boost GST credits for millions. Here’s who qualifies, how much you could...

Find out the OTB payment dates for 2026, eligibility rules, and how the Ontario Trillium Benefit works for Ontario...

From rent to hair styling, phone to internet plans, these expenses are surprisingly negotiable. How every young Canadian can...

Direct deposit puts tax refunds, benefits and other government payments into your bank account faster. Here’s how to sign...

You have a lot of financial responsibilities—and you’re managing them all on your own. But how are your investments...

Some Canadian seniors enter retirement without savings or run out of money over time. Here’s how they can stay...

COVID normalized remote work, but is it really here to stay in Canada?

If you’re looking for extra income to keep up with the rising cost of living, look no further than...

A Certified Financial Planner explains how the CPP process works for a non-resident of Canada and if a return...

It's a new year. What financial changes will take effect in Canada in 2025?