Am I on track…

...to retire at age 55?

Advertisement

...to retire at age 55?

The goal

Janice and Michael Dixon want to retire at age 55 with $50,000 a year in after-tax income.

The current situation

Janice Dixon, a 34-year-old recruiter for an engineering firm in Calgary, and her husband Michael, a 35-year-old IT consultant, set two goals for themselves after the birth of their daughter Maya one year ago. They want to pay off their mortgage in 20 years and retire at 55 with a $50,000 after-tax annual income.

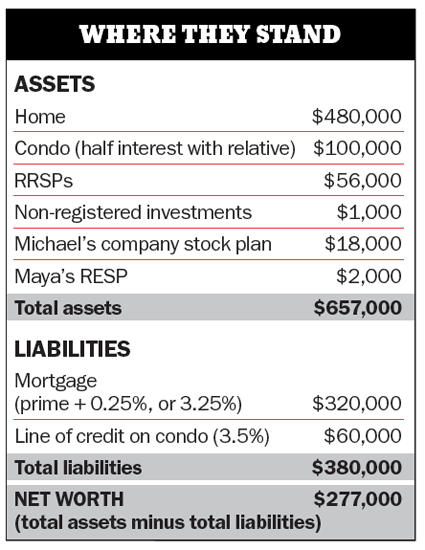

The couple has a current household income of $160,000 and has worked hard over the last five years to accumulate assets. They have $56,000 in mutual funds in their RRSPs and $18,000 in an employer stock plan. They also own a $480,000 home with a $320,000 mortgage on it, and co-own a $200,000 condo.

Their savings plan is simple. Each year Janice contributes $2,000 to an RESP for Maya and $1,200 to her RRSP. Michael puts $12,000 annually into his RRSP and this year he plans to start putting $4,200 into value stocks each year. “Whatever tax refund we get we’ll use it to pay extra on our mortgage,” explains Michael. At 55, the couple hopes to downsize to a condo and spend several months a year travelling. “That’s our dream—to travel the world,” says Janice. “Will we be able to do it?”

The goal

Janice and Michael Dixon want to retire at age 55 with $50,000 a year in after-tax income.

The current situation

Janice Dixon, a 34-year-old recruiter for an engineering firm in Calgary, and her husband Michael, a 35-year-old IT consultant, set two goals for themselves after the birth of their daughter Maya one year ago. They want to pay off their mortgage in 20 years and retire at 55 with a $50,000 after-tax annual income.

The couple has a current household income of $160,000 and has worked hard over the last five years to accumulate assets. They have $56,000 in mutual funds in their RRSPs and $18,000 in an employer stock plan. They also own a $480,000 home with a $320,000 mortgage on it, and co-own a $200,000 condo.

Their savings plan is simple. Each year Janice contributes $2,000 to an RESP for Maya and $1,200 to her RRSP. Michael puts $12,000 annually into his RRSP and this year he plans to start putting $4,200 into value stocks each year. “Whatever tax refund we get we’ll use it to pay extra on our mortgage,” explains Michael. At 55, the couple hopes to downsize to a condo and spend several months a year travelling. “That’s our dream—to travel the world,” says Janice. “Will we be able to do it?”

The verdict

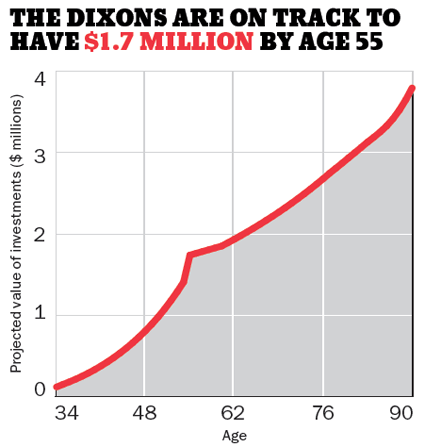

According to Jason Heath, a Certified Financial Planner with E.E.S. Financial in Markham, Ont., yes they will. After running the numbers, Heath projects the couple has enough money to retire by 55—with a healthy surplus of more than $430,000. Overall, the Dixons are doing many things right—they’re still young and they started their savings plan early. Plus they’re investing heavily in their mortgage by making extra payments. “There’s a misconception that you shouldn’t worry about paying down your mortgage when interest rates are low,” says Heath. “But it’s probably the best time to pay down debt, because lump sums go against the principal and reduce the interest you’d incur on future payments at higher rates.” The best news is that even if the Dixons have more children and the $430,000 surplus is whittled away for child-related expenses, the couple would still meet their retirement target. “They have nothing to worry about,” says Heath.

The verdict

According to Jason Heath, a Certified Financial Planner with E.E.S. Financial in Markham, Ont., yes they will. After running the numbers, Heath projects the couple has enough money to retire by 55—with a healthy surplus of more than $430,000. Overall, the Dixons are doing many things right—they’re still young and they started their savings plan early. Plus they’re investing heavily in their mortgage by making extra payments. “There’s a misconception that you shouldn’t worry about paying down your mortgage when interest rates are low,” says Heath. “But it’s probably the best time to pay down debt, because lump sums go against the principal and reduce the interest you’d incur on future payments at higher rates.” The best news is that even if the Dixons have more children and the $430,000 surplus is whittled away for child-related expenses, the couple would still meet their retirement target. “They have nothing to worry about,” says Heath.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Now’s the time to help pay for their education

It's time to discuss how they can start saving for larger purchases

Now's the time to toss the piggy bank and open a bank account instead

It's important to start teaching your kids about money early

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...