Family profile: A tragic development

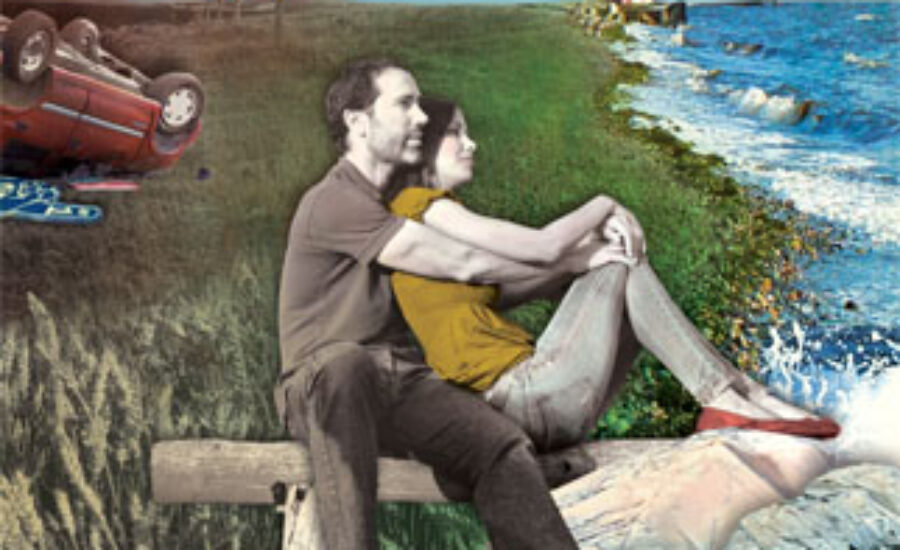

Kurt and Marilyn Brennan dreamed of retiring to Newfoundland. Then Kurt was in an awful truck accident. He may never work again—can they still achieve their dream?

Advertisement

Kurt and Marilyn Brennan dreamed of retiring to Newfoundland. Then Kurt was in an awful truck accident. He may never work again—can they still achieve their dream?

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Now’s the time to help pay for their education

It's time to discuss how they can start saving for larger purchases

Now's the time to toss the piggy bank and open a bank account instead

It's important to start teaching your kids about money early

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...