One family’s strategy for killing debt

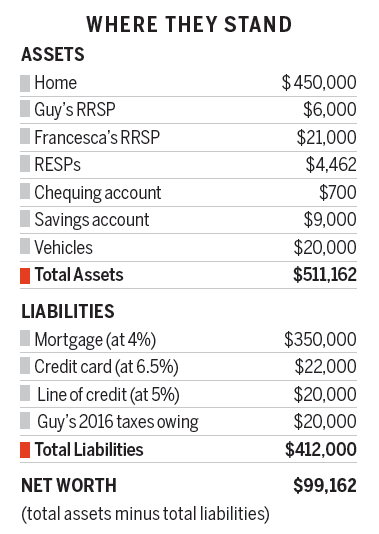

With $42,000 in personal debt plus $20,000 in back taxes to pay, the Nazarios need a plan

Advertisement

With $42,000 in personal debt plus $20,000 in back taxes to pay, the Nazarios need a plan

Toronto financial planner Heather Franklin says the Nazarios have to take action now. “They need to focus on repaying their debt and can’t wait any longer.” Here’s what the Nazarios should do.

Toronto financial planner Heather Franklin says the Nazarios have to take action now. “They need to focus on repaying their debt and can’t wait any longer.” Here’s what the Nazarios should do.

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Navigating student financial aid in Canada? Learn how loans, grants, scholarships, and private options can help pay for post-secondary...

Disabled students in Canada face higher costs for postsecondary education. Here’s a guide to grants, scholarships, and supports that...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Placing a few bets during the World Cup may feel low-stakes, but experts say it’s easy to lose track...

A new study shows that 41% of Canadians believe bankruptcy is a moral failing, at a time when insolvencies...

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

Bank of Canada holds its 2.25% rate for a fourth time amid inflation risks from oil prices, affecting mortgages,...

Most Canadian parents are saving for their child’s education, but few feel confident it will be enough. Here’s why...

Canadians appear to be managing economic pressures overall, but deeper data and lender results reveal growing pockets of credit...