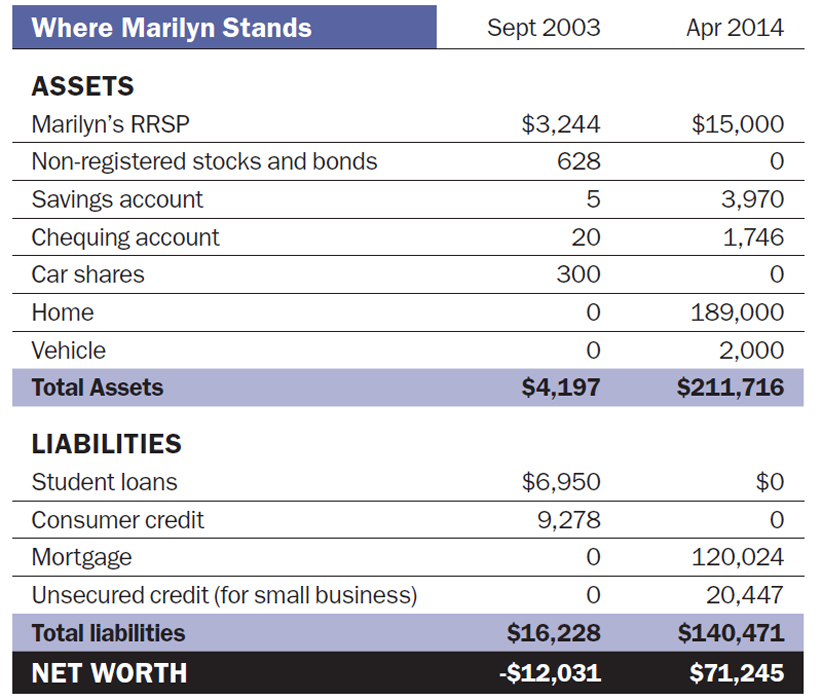

A baby makes two: Marilyn Reynolds now

Debt management made her dreams come true.

Advertisement

Debt management made her dreams come true.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

Canadians may be tired of tipping culture, but newcomers are still trying to figure out the rules.

Financial advisors aren’t always necessary. Learn when you can DIY, when help adds value, and how to decide what’s...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...