Are they on track to retire at 50?

Adam Danyleko, 28, and Justine Oshust, 25, have a big mortgage but want to retire early with $100,000 in net income annually

Advertisement

Adam Danyleko, 28, and Justine Oshust, 25, have a big mortgage but want to retire early with $100,000 in net income annually

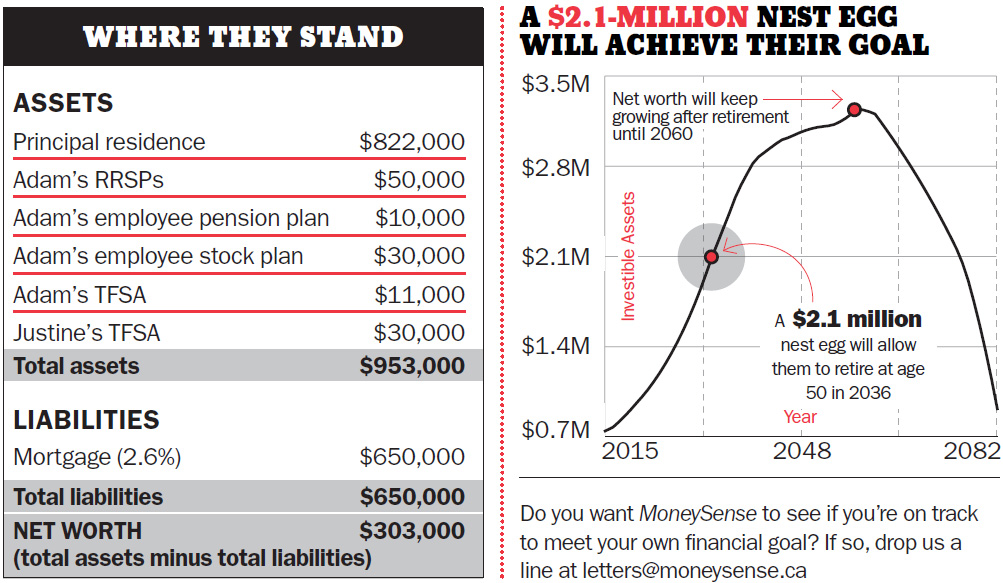

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Why two people at the same life stage can be years apart financially, and how timing, housing, immigration and...

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...

Why do we know we're overpaying and still do nothing about it? A personal look at loyalty, inertia, and...

The biggest financial barrier for newcomers isn't always knowledge, but understanding how familiar words take on new meanings...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...