Coming out of the dark

Lee Crosbie lost his marriage, got cancer and may have to leave his job. Can he rebuild his life?

Advertisement

Lee Crosbie lost his marriage, got cancer and may have to leave his job. Can he rebuild his life?

Before the cancer diagnosis and the divorce proceedings, the Crosbies were a one-income family. Lee and Sandra’s main goal was providing a good family life for their two kids—David, 10, and Tracy, 7. But with the pending divorce there will be big changes. “We are negotiating joint custody of the kids, working on a fair divorce settlement and simply picking up the pieces,” says Lee.

A settlement is expected shortly, and the Crosbies are now in the process of selling their largest asset—the $950,000 family home. “Once the mortgage is paid off, the line of credit is eliminated and the dust has settled, we’ll each be left with $250,000,” says Lee. Sandra will also be entitled to 11.5 years of Lee’s teacher’s pension, which is half the pension accrued during their marriage. There will be no child support or spousal support payments. “I’ll be renting a two-bedroom apartment for at least a couple of years. I’d love to own a home again,” says Lee, “but homes are expensive and I can’t afford it right now.”

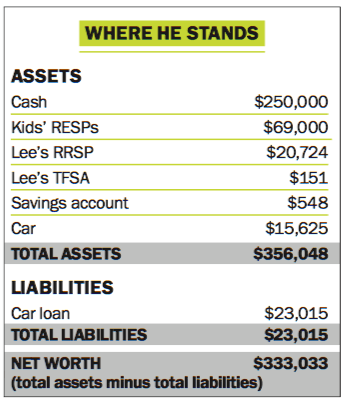

Throughout their marriage, the Crosbies’ financial plan was simple: pay down the mortgage. In fact, the couple had only two other small investments—RESPs for the children and a small RRSP. But if Lee rents, he’d like to know how to invest his $250,000 share of the divorce settlement. He’s also wondering if he should pay off his $23,015 car loan or keep making payments for six more years. “I should probably pay it off but I hate to chip away at my nest egg in case my cancer comes back, or I find myself between teaching contracts.”

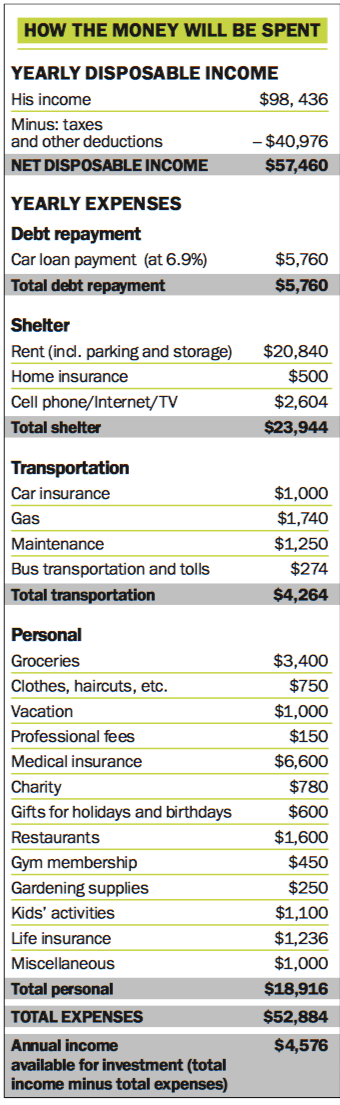

As for the $69,000 in the kids’ RESPs, Lee is unsure whether that amount is enough to fund David and Tracy’s post-secondary education. Should he keep contributing to the RESPs? Or focus on retirement savings? “I’m on leave until next September and collecting $55,000 gross in long-term disability payments.”

After that, Lee intends to go back to work, even if it means working on contract

Before the cancer diagnosis and the divorce proceedings, the Crosbies were a one-income family. Lee and Sandra’s main goal was providing a good family life for their two kids—David, 10, and Tracy, 7. But with the pending divorce there will be big changes. “We are negotiating joint custody of the kids, working on a fair divorce settlement and simply picking up the pieces,” says Lee.

A settlement is expected shortly, and the Crosbies are now in the process of selling their largest asset—the $950,000 family home. “Once the mortgage is paid off, the line of credit is eliminated and the dust has settled, we’ll each be left with $250,000,” says Lee. Sandra will also be entitled to 11.5 years of Lee’s teacher’s pension, which is half the pension accrued during their marriage. There will be no child support or spousal support payments. “I’ll be renting a two-bedroom apartment for at least a couple of years. I’d love to own a home again,” says Lee, “but homes are expensive and I can’t afford it right now.”

Throughout their marriage, the Crosbies’ financial plan was simple: pay down the mortgage. In fact, the couple had only two other small investments—RESPs for the children and a small RRSP. But if Lee rents, he’d like to know how to invest his $250,000 share of the divorce settlement. He’s also wondering if he should pay off his $23,015 car loan or keep making payments for six more years. “I should probably pay it off but I hate to chip away at my nest egg in case my cancer comes back, or I find myself between teaching contracts.”

As for the $69,000 in the kids’ RESPs, Lee is unsure whether that amount is enough to fund David and Tracy’s post-secondary education. Should he keep contributing to the RESPs? Or focus on retirement savings? “I’m on leave until next September and collecting $55,000 gross in long-term disability payments.”

After that, Lee intends to go back to work, even if it means working on contract  closer to home. “Of course, I won’t have job security and that’s a bit scary but in general I know I’ll always be able to get teaching contracts—provided my health holds up.” Teachers’ pension and medical and dental benefits would continue. “What I really need is a plan that will grow my money, a job that I can enjoy without undue stress and a plan for a secure modest retirement on my own. Can you help me?”

Growing up, Lee’s father was a factory worker in a small town in Eastern Ontario and his mother worked part time at a local credit union. “My family lived a Spartan existence,” explains Lee. “We were frugal people who lived well and were very happy.”

In 1989, Lee received a $4,000 scholarship for his university studies and he graduated in 1993 with a teaching degree. He taught in Japan and Colombia for three years and then in 1996, he got his first job—teaching math at a high school in Stouffville, Ont. He met his wife Sandra, an administrative assistant, in 2001, through mutual friends and the two married in 2003. That same year they bought their first home—a detached bungalow in Guelph, Ont., for $269,000. The couple had two kids—David in 2006 and Tracy in 2008—and Sandra gave up her job to stay home and raise the kids. Then, in 2010, the couple sold their starter home and bought a new four-bedroom home in the same Guelph neighbourhood for $425,000. Today, the house is worth $950,000 and they are in the process of selling it before finalizing their divorce. “I think our investment in our home helped us avoid losses in the 2008 market crash crisis because almost all of our equity was tied up in our house,” says Lee. “It paid off for us.”

Right now, Lee’s second biggest asset after his home is his teacher’s pension. He also has $20,724 in his RRSP, $151 in his TFSA and $548 in a savings account. “The little investing I’ve done is in the kids’ RESPs, which we’ve faithfully contributed to over the years, using index funds and replicating the couch potato,” says Lee. “Being a single-income household, we really didn’t have much extra money around to worry about.”

Although Lee loves teaching, his job is very stressful as he’s expected to run several math clubs and enter his students in national and global competitions through the year. “What suffered was my family life and seeing a lot less of my kids than I would have liked, but going forward, I aim to change that,” says Lee. But the job stress, combined with the daily two-hour commute, took its toll on Lee’s marriage. After a few sessions with a marriage counsellor, the couple decided to divorce. “Between couple counseling costs and divorce lawyers, it’s been a very expensive year,” says Lee. “Those one-time costs alone totalled $10,000 for us.”

These days, Lee is looking forward and right now he is apartment hunting. He figures a two-bedroom unit just blocks from his two kids will cost him about $20,000 annually. “I dream of owning a house again but for now preserving my nest egg is my primary consideration.” The truth is Lee never had to manage such a large sum of money and although he’s done a simple couch potato portfolio for his kids’ RESPs, he’s not sure that’s the right strategy for the settlement money. “My brother said he’d manage the money, but I’d like to explore other options before I commit.”

For the next year, Lee will be living on long-term disability payments of $55,000 gross from his employer but he expects to make a full recovery and be earning $95,000 again soon, even if it is on contract. “I should be able to duplicate my salary plus benefits at that time,” says Lee. “I won’t ever have full job security after I leave my full-time job but I’ll always be able to do contract work.”

Once he’s back working full time next fall, Lee will be able to save about $4,576 a year, plus about $6,600 in annual medical expenses that will be gone when benefits with his employer kick in. “I’ll be able to save $10,000 to $15,000 annually,” says Lee. “But where should that money go?—RRSP? TFSA? RESP? It’s hard to know.” One thing’s for sure, Lee plans to keep on teaching in some form or another for years to come. “It’s my life’s passion and I plan to die with my boots on.”

In the spring, once he’s recuperated from surgery, Lee’s planning a bit of fun. “It’s my best chance at being able to take the kids somewhere special. I’m learning the hard way that without some planning, life just happens anyway. I’ve been given a glimpse of mortality and I don’t want to think that this chapter has been wasted on me.”

closer to home. “Of course, I won’t have job security and that’s a bit scary but in general I know I’ll always be able to get teaching contracts—provided my health holds up.” Teachers’ pension and medical and dental benefits would continue. “What I really need is a plan that will grow my money, a job that I can enjoy without undue stress and a plan for a secure modest retirement on my own. Can you help me?”

Growing up, Lee’s father was a factory worker in a small town in Eastern Ontario and his mother worked part time at a local credit union. “My family lived a Spartan existence,” explains Lee. “We were frugal people who lived well and were very happy.”

In 1989, Lee received a $4,000 scholarship for his university studies and he graduated in 1993 with a teaching degree. He taught in Japan and Colombia for three years and then in 1996, he got his first job—teaching math at a high school in Stouffville, Ont. He met his wife Sandra, an administrative assistant, in 2001, through mutual friends and the two married in 2003. That same year they bought their first home—a detached bungalow in Guelph, Ont., for $269,000. The couple had two kids—David in 2006 and Tracy in 2008—and Sandra gave up her job to stay home and raise the kids. Then, in 2010, the couple sold their starter home and bought a new four-bedroom home in the same Guelph neighbourhood for $425,000. Today, the house is worth $950,000 and they are in the process of selling it before finalizing their divorce. “I think our investment in our home helped us avoid losses in the 2008 market crash crisis because almost all of our equity was tied up in our house,” says Lee. “It paid off for us.”

Right now, Lee’s second biggest asset after his home is his teacher’s pension. He also has $20,724 in his RRSP, $151 in his TFSA and $548 in a savings account. “The little investing I’ve done is in the kids’ RESPs, which we’ve faithfully contributed to over the years, using index funds and replicating the couch potato,” says Lee. “Being a single-income household, we really didn’t have much extra money around to worry about.”

Although Lee loves teaching, his job is very stressful as he’s expected to run several math clubs and enter his students in national and global competitions through the year. “What suffered was my family life and seeing a lot less of my kids than I would have liked, but going forward, I aim to change that,” says Lee. But the job stress, combined with the daily two-hour commute, took its toll on Lee’s marriage. After a few sessions with a marriage counsellor, the couple decided to divorce. “Between couple counseling costs and divorce lawyers, it’s been a very expensive year,” says Lee. “Those one-time costs alone totalled $10,000 for us.”

These days, Lee is looking forward and right now he is apartment hunting. He figures a two-bedroom unit just blocks from his two kids will cost him about $20,000 annually. “I dream of owning a house again but for now preserving my nest egg is my primary consideration.” The truth is Lee never had to manage such a large sum of money and although he’s done a simple couch potato portfolio for his kids’ RESPs, he’s not sure that’s the right strategy for the settlement money. “My brother said he’d manage the money, but I’d like to explore other options before I commit.”

For the next year, Lee will be living on long-term disability payments of $55,000 gross from his employer but he expects to make a full recovery and be earning $95,000 again soon, even if it is on contract. “I should be able to duplicate my salary plus benefits at that time,” says Lee. “I won’t ever have full job security after I leave my full-time job but I’ll always be able to do contract work.”

Once he’s back working full time next fall, Lee will be able to save about $4,576 a year, plus about $6,600 in annual medical expenses that will be gone when benefits with his employer kick in. “I’ll be able to save $10,000 to $15,000 annually,” says Lee. “But where should that money go?—RRSP? TFSA? RESP? It’s hard to know.” One thing’s for sure, Lee plans to keep on teaching in some form or another for years to come. “It’s my life’s passion and I plan to die with my boots on.”

In the spring, once he’s recuperated from surgery, Lee’s planning a bit of fun. “It’s my best chance at being able to take the kids somewhere special. I’m learning the hard way that without some planning, life just happens anyway. I’ve been given a glimpse of mortality and I don’t want to think that this chapter has been wasted on me.”

Rent, don’t own. Until Lee has a sense of what the long term holds for his health, work and new family dynamic, he should rent. “It’s simple, stress-free and flexible until the dust settles,” says Heath.

Pay off the car loan. The only debt Lee has now is his $23,015 car loan at a 6.9%. “He should pay off the entire loan with some of the $250,000 he gets from the divorce settlement,” says Kvick. “It’s hard to make a real rate of return (after fees and taxes) of 6.9% from investments,” says Kvick. Paying off the car loan now also means Lee can increase his annual savings by $5,760, lightening his financial load going forward.

Create an emergency fund. Lee needs to set aside about $30,000 in an emergency fund. “This should go into a high-interest savings account so he can access it quickly if the need arises due to health reasons or occasional lower job earnings,” says Kvick.

Nail down RESP contributions. “If Lee plans to pay for all of a four-year, $20,000 annual post-secondary education for each of his two kids, he needs to continue to contribute his half of the maximum, or about $1,250 per child per year for the next six or seven years,” says Heath. But if he only wants to cover half of their post-secondary costs then he has enough right now with the $69,000 invested in RESPs. But there’s a third option. “Lee should ask family members to make future birthday and Christmas gifts to the children’s RESPs,” says Heath. “Family members such as aunts, uncles and grandparents often get a lot of joy by doing this.”

Start a savings program. Each year going forward, Lee will have $10,000 to $15,000 to invest when he returns to work full time next fall. Both Kvick and Heath say Lee should maximize his TFSA contributions, even if the money just goes to a savings account or bond ETF. “The money shouldn’t be invested more aggressively than this until his finances and health are more stable, and he’s made a final decision regarding whether or not to buy a home,” says Kvick. Once he’s back to consistent, full-time work, Lee should “aim to top up his RRSP for the next few years while he’s in a high tax bracket,” says Heath. And only once he decides to rent on a permanent basis should he invest his settlement money for the longer term—50% in equities and 50% in fixed-income securities.

Set aside $2,500 for family fun. Kids are only young once. “Spend a little more on travel or activities with the kids as health permits,” says Kvick. “About $2,500 is a manageable annual amount for his budget going forward.”

Update wills. After a divorce, it’s important to update legal documents such as wills and powers of attorney since a divorce doesn’t nullify legal documents. “It’s also important to update beneficiaries on pension plans, RRSPs and TFSAs,” says Kvick.

Retire at 60 or 65. If Lee continues to max out his teacher’s pension contributions every year with the new school board, he’ll have a comfortable retirement, even though he may not have a house and 11.5 years of his pension will have gone to his wife. “His pension at age 65 will be about $35,000 annually,” says Kvick. With CPP, OAS, and extra savings annually to his RRSP—especially when the kids are grown—Lee will have a very comfortable retirement. “He has a solid base from which to build and that will take him very far,” says Kvick.

Rent, don’t own. Until Lee has a sense of what the long term holds for his health, work and new family dynamic, he should rent. “It’s simple, stress-free and flexible until the dust settles,” says Heath.

Pay off the car loan. The only debt Lee has now is his $23,015 car loan at a 6.9%. “He should pay off the entire loan with some of the $250,000 he gets from the divorce settlement,” says Kvick. “It’s hard to make a real rate of return (after fees and taxes) of 6.9% from investments,” says Kvick. Paying off the car loan now also means Lee can increase his annual savings by $5,760, lightening his financial load going forward.

Create an emergency fund. Lee needs to set aside about $30,000 in an emergency fund. “This should go into a high-interest savings account so he can access it quickly if the need arises due to health reasons or occasional lower job earnings,” says Kvick.

Nail down RESP contributions. “If Lee plans to pay for all of a four-year, $20,000 annual post-secondary education for each of his two kids, he needs to continue to contribute his half of the maximum, or about $1,250 per child per year for the next six or seven years,” says Heath. But if he only wants to cover half of their post-secondary costs then he has enough right now with the $69,000 invested in RESPs. But there’s a third option. “Lee should ask family members to make future birthday and Christmas gifts to the children’s RESPs,” says Heath. “Family members such as aunts, uncles and grandparents often get a lot of joy by doing this.”

Start a savings program. Each year going forward, Lee will have $10,000 to $15,000 to invest when he returns to work full time next fall. Both Kvick and Heath say Lee should maximize his TFSA contributions, even if the money just goes to a savings account or bond ETF. “The money shouldn’t be invested more aggressively than this until his finances and health are more stable, and he’s made a final decision regarding whether or not to buy a home,” says Kvick. Once he’s back to consistent, full-time work, Lee should “aim to top up his RRSP for the next few years while he’s in a high tax bracket,” says Heath. And only once he decides to rent on a permanent basis should he invest his settlement money for the longer term—50% in equities and 50% in fixed-income securities.

Set aside $2,500 for family fun. Kids are only young once. “Spend a little more on travel or activities with the kids as health permits,” says Kvick. “About $2,500 is a manageable annual amount for his budget going forward.”

Update wills. After a divorce, it’s important to update legal documents such as wills and powers of attorney since a divorce doesn’t nullify legal documents. “It’s also important to update beneficiaries on pension plans, RRSPs and TFSAs,” says Kvick.

Retire at 60 or 65. If Lee continues to max out his teacher’s pension contributions every year with the new school board, he’ll have a comfortable retirement, even though he may not have a house and 11.5 years of his pension will have gone to his wife. “His pension at age 65 will be about $35,000 annually,” says Kvick. With CPP, OAS, and extra savings annually to his RRSP—especially when the kids are grown—Lee will have a very comfortable retirement. “He has a solid base from which to build and that will take him very far,” says Kvick.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

More Canadians are turning to ChatGPT and other AI tools for money advice. Here's what to know about trust...

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.