Having a baby? Update your financial plan

Now that baby Emily’s here, the Martins’ priorities have suddenly changed—and they’re concerned about their financial future

Advertisement

Now that baby Emily’s here, the Martins’ priorities have suddenly changed—and they’re concerned about their financial future

But beyond those logistics, several questions remain unanswered for the couple. For starters, they wonder if it’s time to update their life insurance now that they have a dependant. “We have a $250,000, 20-year term life policy that we pay $38 a month for,” says Marie. “We’re sure it’s not enough but aren’t sure what to replace it with.” Also of concern is the fact that Alain has no disability insurance. “These are really questions we’ve just started asking ourselves with Emily’s arrival,” he says. “Kids really do change things.” There’s Emily’s future post-secondary needs to think about, too. “My parents contribute $15 every two weeks and we add another $1,720 for a total of $2,500 annually to her Registered Education Savings Plan (RESP),” says Marie. “Is that enough?”

Baby anxieties aside, the Martins are also worried about themselves—specifically, what savings and investment strategy they should adopt going forward. “Since neither Marie nor I have a company pension plan I don’t think we can reach our retirement goal of having enough income to support an upper-middle-class retirement,” says Alain. “Until now, we haven’t given much thought to our actual investments. We’ll need to do better, but there are so many choices.”

Something working in the couple’s favour that shouldn’t be overlooked are the good financial lessons they received from their families. Both Marie and Alain have fathers who worked for government tax centres, something that helped them to learn the value of a dollar. “When I was growing up, we had a very comfortable middle-class lifestyle,” says Marie. “We want the same for our growing family.”

So far, they’re meeting that goal. After the couple graduated from university in 2007—Marie with a Bachelor of Fine Arts and Alain with a Bachelor of Commerce—they’ve held down steady jobs that pay them annual salaries of $50,000 each. While Marie still works with the same company where she’s now a marketing associate, Alain ran his own office services company until he got a job as an office manager at a doctor’s clinic in 2012. “We’ve lived a very nice life on modest incomes,” he says.

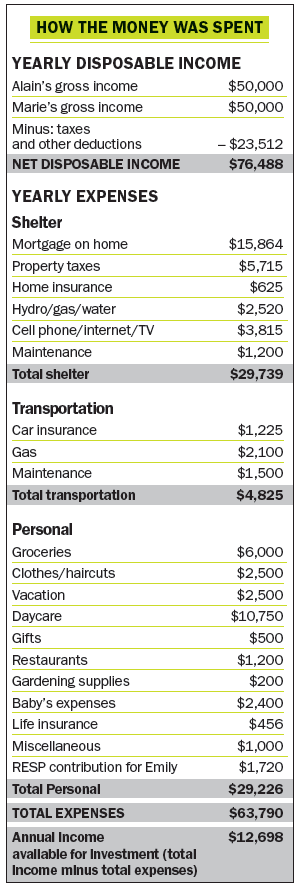

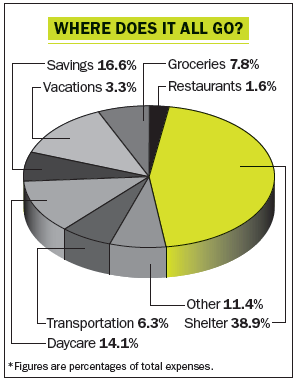

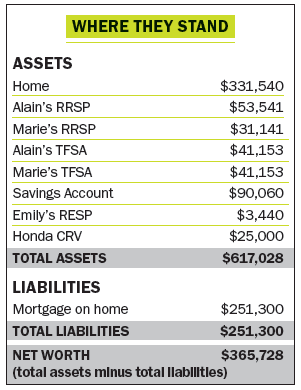

And despite all of their apprehensions, they’ve also been excellent savers. Financially, they’re in a strong position. At just age 30, they’ve already managed to tuck away $257,048 in RRSPs, TFSAs and other savings—and the couple’s only debt is the $251,300 mortgage on their $331,540 home. Until now, their financial strategy has been simple: focus on paying down their home while using extra cash flow to beef up their various savings accounts.

In fact, it’s their success with this strategy that’s partly at the root of their financial soul-searching. With about $90,000 sitting in a bank account (money from the small business Alain ran until he shut it down three years ago), plus another anticipated $80,000 in gains from the sale of their Hamilton home, the Martins are confused about the best way to get their money working.

Their current plans are to live in Marie’s parents’ Ottawa home for a few months until they buy their own house, an expenditure they figure will cost them about $400,000. While they plan to put $80,000 toward a 20% down payment, they’re not sure prioritizing the mortgage—as they’ve been doing up until now—is the right move anymore. “Even though we always read articles extolling the benefits of paying off your mortgage as quickly as possible, we’re beginning to question that strategy because of the low interest rates,” says Marie. “We may be able to get a better return on our money with other investments.”

To date, the couple has invested their money in their RRSPs and TFSAs in mutual funds, with 40% in fixed-income investments and 60% in equities. “We get 4% net annually in returns so nothing too risky for us yet,” says Alain. But he now wants to change that. “I’m tempted to play the stock market and maybe buy some dividend-paying stocks as well. That would require some research but I’d like to try it.”

But beyond those logistics, several questions remain unanswered for the couple. For starters, they wonder if it’s time to update their life insurance now that they have a dependant. “We have a $250,000, 20-year term life policy that we pay $38 a month for,” says Marie. “We’re sure it’s not enough but aren’t sure what to replace it with.” Also of concern is the fact that Alain has no disability insurance. “These are really questions we’ve just started asking ourselves with Emily’s arrival,” he says. “Kids really do change things.” There’s Emily’s future post-secondary needs to think about, too. “My parents contribute $15 every two weeks and we add another $1,720 for a total of $2,500 annually to her Registered Education Savings Plan (RESP),” says Marie. “Is that enough?”

Baby anxieties aside, the Martins are also worried about themselves—specifically, what savings and investment strategy they should adopt going forward. “Since neither Marie nor I have a company pension plan I don’t think we can reach our retirement goal of having enough income to support an upper-middle-class retirement,” says Alain. “Until now, we haven’t given much thought to our actual investments. We’ll need to do better, but there are so many choices.”

Something working in the couple’s favour that shouldn’t be overlooked are the good financial lessons they received from their families. Both Marie and Alain have fathers who worked for government tax centres, something that helped them to learn the value of a dollar. “When I was growing up, we had a very comfortable middle-class lifestyle,” says Marie. “We want the same for our growing family.”

So far, they’re meeting that goal. After the couple graduated from university in 2007—Marie with a Bachelor of Fine Arts and Alain with a Bachelor of Commerce—they’ve held down steady jobs that pay them annual salaries of $50,000 each. While Marie still works with the same company where she’s now a marketing associate, Alain ran his own office services company until he got a job as an office manager at a doctor’s clinic in 2012. “We’ve lived a very nice life on modest incomes,” he says.

And despite all of their apprehensions, they’ve also been excellent savers. Financially, they’re in a strong position. At just age 30, they’ve already managed to tuck away $257,048 in RRSPs, TFSAs and other savings—and the couple’s only debt is the $251,300 mortgage on their $331,540 home. Until now, their financial strategy has been simple: focus on paying down their home while using extra cash flow to beef up their various savings accounts.

In fact, it’s their success with this strategy that’s partly at the root of their financial soul-searching. With about $90,000 sitting in a bank account (money from the small business Alain ran until he shut it down three years ago), plus another anticipated $80,000 in gains from the sale of their Hamilton home, the Martins are confused about the best way to get their money working.

Their current plans are to live in Marie’s parents’ Ottawa home for a few months until they buy their own house, an expenditure they figure will cost them about $400,000. While they plan to put $80,000 toward a 20% down payment, they’re not sure prioritizing the mortgage—as they’ve been doing up until now—is the right move anymore. “Even though we always read articles extolling the benefits of paying off your mortgage as quickly as possible, we’re beginning to question that strategy because of the low interest rates,” says Marie. “We may be able to get a better return on our money with other investments.”

To date, the couple has invested their money in their RRSPs and TFSAs in mutual funds, with 40% in fixed-income investments and 60% in equities. “We get 4% net annually in returns so nothing too risky for us yet,” says Alain. But he now wants to change that. “I’m tempted to play the stock market and maybe buy some dividend-paying stocks as well. That would require some research but I’d like to try it.” However, there’s another option Alain is considering that holds even more allure. “I would like to explore the world of income properties. The idea of having other people pay my mortgage appeals to me.”

For now, however, the couple looks forward to spending more time with family in Ottawa—attending the odd Ottawa Senators hockey game (they’re big fans) and playing a few rounds of golf while the good weather lasts. “Having Emily has made us realize the value of family nearby, as well as the importance of good financial planning,” says Marie. “We want to ensure our growing family always has the security of both.”

However, there’s another option Alain is considering that holds even more allure. “I would like to explore the world of income properties. The idea of having other people pay my mortgage appeals to me.”

For now, however, the couple looks forward to spending more time with family in Ottawa—attending the odd Ottawa Senators hockey game (they’re big fans) and playing a few rounds of golf while the good weather lasts. “Having Emily has made us realize the value of family nearby, as well as the importance of good financial planning,” says Marie. “We want to ensure our growing family always has the security of both.”

Trevor Van Nest, a money coach in St. Catharines, Ont., agrees. “They’re a bit confused because the financial literacy isn’t there—not because they don’t have enough money. What they need is to define their objectives first.” For instance, what annual income do they want to have in retirement? How much exactly do they want to save for post-secondary education for Emily—enough to finance four years of university, or just one or two? Answering those questions is key to building a solid plan that they’ll be happy sticking to.

Here’s what they should do to achieve their retirement goals.

Pay off the mortgage faster. “While it may not make sense to eliminate low-interest rate debt, there’s no time like the present to get rid of debt that one day might be very expensive to service,” says Van Nest. Putting a 20% down payment on their new Ottawa home is a no-brainer—this will save them the thousands of dollars they would have had to pay for Canada Mortgage and Housing Corporation (CMHC) mortgage insurance. But they should also take advantage of mortgage prepayment privileges and focus on eliminating the principal with a disciplined approach, says Forward. “They can do this by applying any tax refund they get annually towards the principal. This way, they can continue using the $12,698 they have available for investments every year and put it towards TFSAs or RRSPs.”

Forget the income property. Owning a home typically means most families are already over-invested in real estate, so other asset classes should be explored, says Van Nest. In fact, Marie and Alain should take lessons from large, successful investors like the Canada Pension Plan. CPP has only 11% of its assets in real estate, while the rest of its portfolio includes larger holdings in equities and fixed-income securities. “The Martins’ own asset allocation should reflect their own risk tolerance,” says Van Nest. “That means less real estate.”

Moreover, he adds, small investors who invest in income properties often make big mistakes that include having high expectations for property appreciation, under-estimating maintenance and renovation costs, as well as getting caught off-guard by the total time commitment involved. “The Martins are modest spenders and very good savers, and the truth is they can reach their retirement goals without the extra real estate,” says Van Nest.

Stick with a balanced fund. Van Nest also advises the Martins avoid individual stock picking and not make investing any more complicated than it has to be. “A couple of simple, low-cost mutual funds or exchange-traded funds (ETFs), split 60% equity and 40% fixed income, would seem appropriate given the Martins long time frames and relatively conservative investor profiles.”

Get ‘non-cancellable’ disability insurance. Alain should aim to replace 60% of his gross income, says Lorne Marr, a certified financial planner in Markham, Ont. But he should opt for a non-cancellable disability plan—meaning he can cancel it but the insurance company can’t, nor can they raise his premiums.” Such a policy would cost Alain about $110 a month, or $1,320 per year. “He should get it now,” says Marr. “He has a young, growing family that needs his income to maintain their lifestyle.” Alain should also keep in mind that payments from private disability insurance plans are tax-free, unlike those from most corporate plans.

Buy more term life insurance. Even though the Martins each have $250,000 term life insurance policies, it isn’t enough. “A good rule of thumb is five to 10 times annual income—five times for parents with children over 10 years old, and 10 times for parents with children under 10 years old,” says Marr. Add to that number the outstanding amount on your mortgage, which in the Martin’s case is about $300,000. That means both Alain and Marie need $800,000 of coverage.

The cost for that protection is reasonable, says Marr. For instance, a 20-year term life policy for Alain will run about $55 a month and a similar one for Marie, $39 a month. That adds up to $1,128 annually. “Life insurance is designed to replace income,” says Marr. “So if either Marie or Alain die, this will allow the other to pay for daycare costs for their child, put money aside for retirement and pay for Emily’s education. It’s an important safety net they shouldn’t ignore.”

If the Martins continue on this path at their current savings rate of $15,000 annually (an amount that should grow 3% annually to keep up with inflation), and they achieve a 5% gross annual rate of return, they will have $1.3 million in total retirement savings at age 65. “With a paid-off house, as well as CPP and Old Age Security payments, the couple will be able to retire with a very healthy income indeed,” says Van Nest. “With continued savings and investing discipline, it will be an easy goal for them to achieve.”

Trevor Van Nest, a money coach in St. Catharines, Ont., agrees. “They’re a bit confused because the financial literacy isn’t there—not because they don’t have enough money. What they need is to define their objectives first.” For instance, what annual income do they want to have in retirement? How much exactly do they want to save for post-secondary education for Emily—enough to finance four years of university, or just one or two? Answering those questions is key to building a solid plan that they’ll be happy sticking to.

Here’s what they should do to achieve their retirement goals.

Pay off the mortgage faster. “While it may not make sense to eliminate low-interest rate debt, there’s no time like the present to get rid of debt that one day might be very expensive to service,” says Van Nest. Putting a 20% down payment on their new Ottawa home is a no-brainer—this will save them the thousands of dollars they would have had to pay for Canada Mortgage and Housing Corporation (CMHC) mortgage insurance. But they should also take advantage of mortgage prepayment privileges and focus on eliminating the principal with a disciplined approach, says Forward. “They can do this by applying any tax refund they get annually towards the principal. This way, they can continue using the $12,698 they have available for investments every year and put it towards TFSAs or RRSPs.”

Forget the income property. Owning a home typically means most families are already over-invested in real estate, so other asset classes should be explored, says Van Nest. In fact, Marie and Alain should take lessons from large, successful investors like the Canada Pension Plan. CPP has only 11% of its assets in real estate, while the rest of its portfolio includes larger holdings in equities and fixed-income securities. “The Martins’ own asset allocation should reflect their own risk tolerance,” says Van Nest. “That means less real estate.”

Moreover, he adds, small investors who invest in income properties often make big mistakes that include having high expectations for property appreciation, under-estimating maintenance and renovation costs, as well as getting caught off-guard by the total time commitment involved. “The Martins are modest spenders and very good savers, and the truth is they can reach their retirement goals without the extra real estate,” says Van Nest.

Stick with a balanced fund. Van Nest also advises the Martins avoid individual stock picking and not make investing any more complicated than it has to be. “A couple of simple, low-cost mutual funds or exchange-traded funds (ETFs), split 60% equity and 40% fixed income, would seem appropriate given the Martins long time frames and relatively conservative investor profiles.”

Get ‘non-cancellable’ disability insurance. Alain should aim to replace 60% of his gross income, says Lorne Marr, a certified financial planner in Markham, Ont. But he should opt for a non-cancellable disability plan—meaning he can cancel it but the insurance company can’t, nor can they raise his premiums.” Such a policy would cost Alain about $110 a month, or $1,320 per year. “He should get it now,” says Marr. “He has a young, growing family that needs his income to maintain their lifestyle.” Alain should also keep in mind that payments from private disability insurance plans are tax-free, unlike those from most corporate plans.

Buy more term life insurance. Even though the Martins each have $250,000 term life insurance policies, it isn’t enough. “A good rule of thumb is five to 10 times annual income—five times for parents with children over 10 years old, and 10 times for parents with children under 10 years old,” says Marr. Add to that number the outstanding amount on your mortgage, which in the Martin’s case is about $300,000. That means both Alain and Marie need $800,000 of coverage.

The cost for that protection is reasonable, says Marr. For instance, a 20-year term life policy for Alain will run about $55 a month and a similar one for Marie, $39 a month. That adds up to $1,128 annually. “Life insurance is designed to replace income,” says Marr. “So if either Marie or Alain die, this will allow the other to pay for daycare costs for their child, put money aside for retirement and pay for Emily’s education. It’s an important safety net they shouldn’t ignore.”

If the Martins continue on this path at their current savings rate of $15,000 annually (an amount that should grow 3% annually to keep up with inflation), and they achieve a 5% gross annual rate of return, they will have $1.3 million in total retirement savings at age 65. “With a paid-off house, as well as CPP and Old Age Security payments, the couple will be able to retire with a very healthy income indeed,” says Van Nest. “With continued savings and investing discipline, it will be an easy goal for them to achieve.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

More Canadians are turning to ChatGPT and other AI tools for money advice. Here's what to know about trust...

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.