How to build an advanced couch potato portfolio

Adding unrepresented (or underrepresented) asset classes to a core portfolio can reduce risk, increase returns, or both. Here are some options to add a little extra to your savings.

Advertisement

Adding unrepresented (or underrepresented) asset classes to a core portfolio can reduce risk, increase returns, or both. Here are some options to add a little extra to your savings.

“Advanced couch potato” anything might sound like an oxymoron, but hear us out. First, couch-potato investing is not just for people who hate investing. Lots of smart investors have recognized that they can get competitive returns at very low cost using index funds and a passive methodology. They might combine it with individual stock holdings, GICs, and bonds.

They recognize, too, that there are more fish in the sea than the stock and bond indices represented in core portfolios. They may seek to spice up returns or further diversify with, say, a high-yield bond or crypto fund. There’s no limit to the add-ons you can apply to a couch portfolio.

Second, there are those who get the hang of managing a core portfolio, like the results, and, upon gaining investment knowledge and experience, feel comfortable raising the complexity of their holdings. Couch potato investing offers a good entry level to more sophisticated investing, by which time your nest egg will likely have grown and gained a momentum all its own.

While the core exposures should always represent a majority of any long-term investment portfolio, here are some asset types available through ETFs that typically aren’t represented in core portfolios:

There may also be segments of the investible universe already embedded within core portfolios that an investor might seek to increase their exposure to:

American investor Ray Dalio famously created an “all-weather portfolio” that he claimed would hold up in almost any market environment. It broke down like this: 30% U.S. stocks, 40% long-term treasury bonds, 15% intermediate bonds, 7.5% commodities, and 7.5% gold. Should you so choose, you could create a reasonable facsimile to the all-weather portfolio using ETFs.

Our MoneySense columnists have likewise illustrated how you can further diversify a core portfolio, reducing the risk of losses.

Here’s one such strategy, augmenting an asset-allocation fund with cash and/or gold bullion that would have held up well through past market downturns. And there’s another that adopts the buzzy 40/30/30 portfolio model that includes exposure to alternative assets along with stocks and bonds.

If you think you might be ready to take the next step beyond investing just in Canadian bonds and the major investible regions for equities, consider one of the advanced portfolios listed below. These are just suggested allocations that we believe won’t lead you too far astray. Feel free to tweak them to better suit your circumstances and build on them over time.

An important note: As your portfolio gets more complex, it will be harder to fill each allocation with index mutual funds and asset-allocation ETFs, which is why index ETFs are the go-to vehicle for building an advanced portfolio. We’ve suggested some funds, but with some 1,500 ETFs trading in Canada, know that there will be comparable competing products out there, possibly with lower fees or other attractive attributes.

Consider our fund picks suggestions only. For up-to-date ETF recommendations from the experts, check out MoneySense’s guide to the best ETFs in Canada, which we update every year in May.

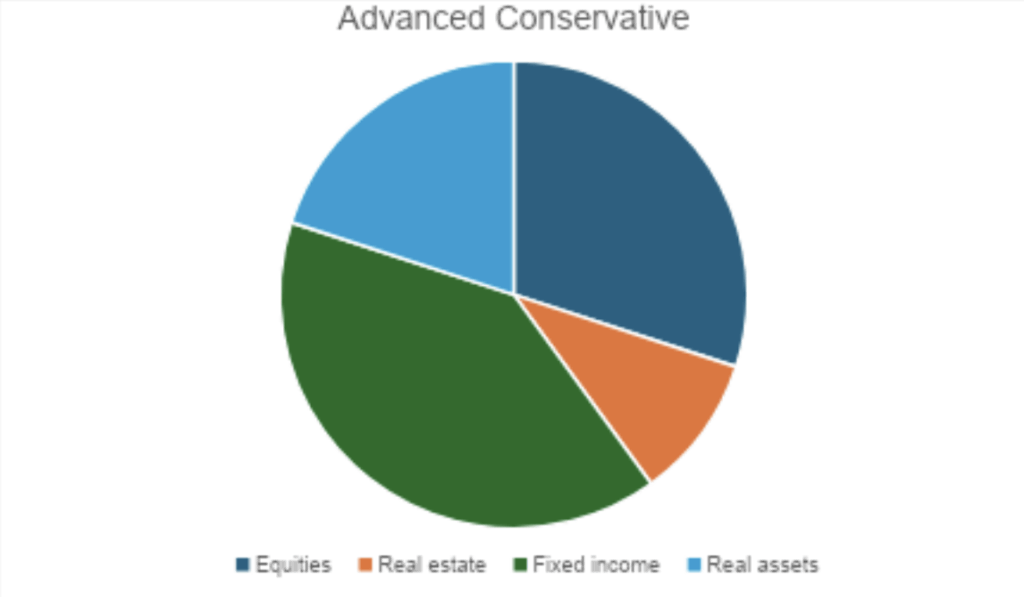

Equities: 30%

Real estate: 10%

Fixed income: 40%

Real assets: 20%

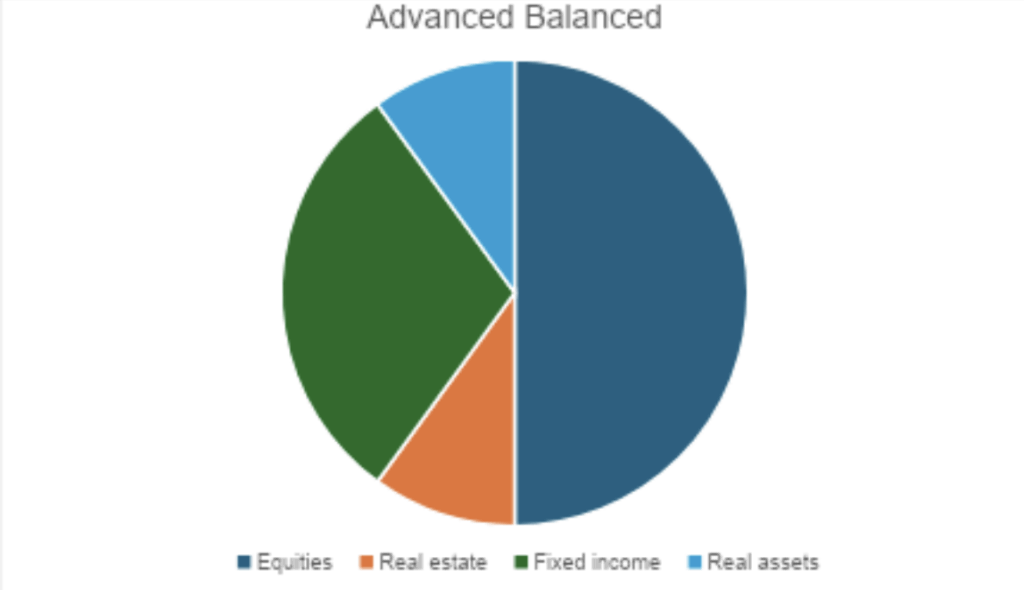

Equities: 50%

Real estate: 10%

Fixed income: 30%

Real assets: 10%

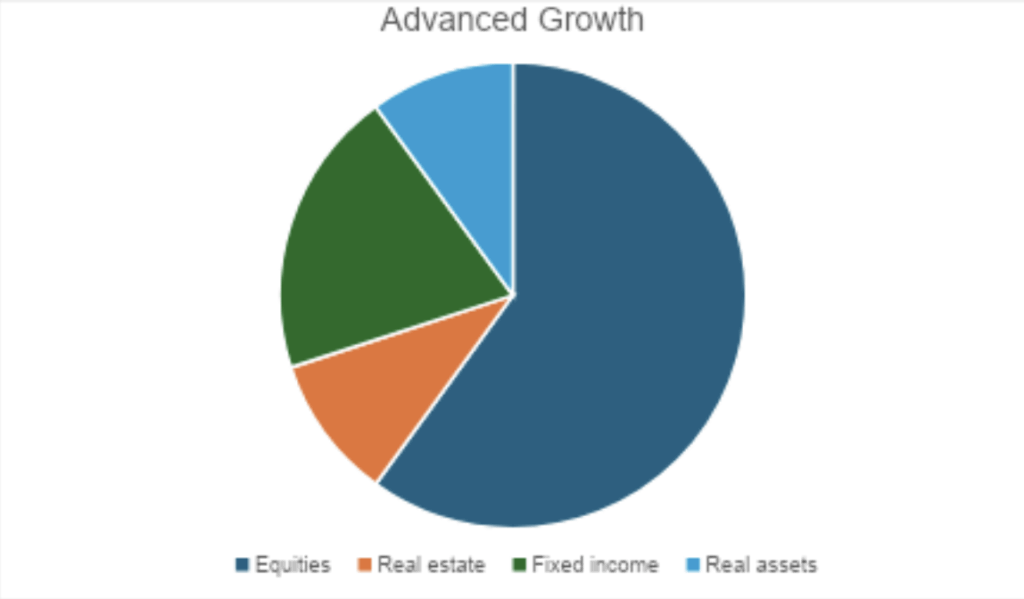

Equities: 60%

Real estate: 10%

Fixed income: 20%

Real assets: 10%

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Bitcoin extends losses, down 47% since October 2025. When will the crypto bear market reverse, and what does the...

Crypto profits aren’t always tax-free. Here’s how the CRA taxes cryptocurrency transactions, mining and staking, and overseas gains.

Low trading volume does not necessarily mean low liquidity. Here’s what actually determines how easy it is to buy...

Vanguard’s VRIF ETF is tilting toward bonds to provide retirees stable income, balancing caution with a 4% annual payout...

Tara Bosch of SmartSweets shares the financial lessons, mindset shifts, and money habits that helped her build and sell...

These relationships have very specific meanings for tax purposes. It’s up to you to get them right.

Retirement planning for couples with a significant age difference calls for realistic projections but also flexibility.

The Knix founder shares her money mindset, including saving for a rainy say, spending wisely, and maintaining a healthy...

Sponsored By

RBC

In maintaining your planned allocations in a portfolio of ETFs, consistency matters more than precision.