Build a portfolio you can ‘set and forget’

Hold too many products and you’ll end up paying a small fortune in fees. The solution? A couple of ETFs

Advertisement

Hold too many products and you’ll end up paying a small fortune in fees. The solution? A couple of ETFs

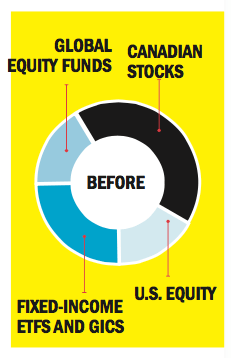

Ian Nelson is a 37-year-old married father of two from Toronto who has spent the last several years paying off the mortgage on his $750,000 home and adding to his retirement savings. Right now, he has a six-figure portfolio invested solely in RRSPs that includes several Canadian stocks as well as three mutual funds, a handful of exchange-traded funds (ETFs), GICs and $16,000 in cash. Now, he’s looking for a well-diversified portfolio that’s low-cost and low-maintenance. “I invest $5,500 quarterly into RRSPs and expect to do this until retirement at age 55. I want to simply buy and hold.”

It’s no small feat to create a low-fee portfolio that doesn’t require annual rebalancing, says Miles Clyne, a portfolio manager with the Tycuda Group at MacDougall Investment Counsel Inc., in Langley, B.C. “But it can be done.”

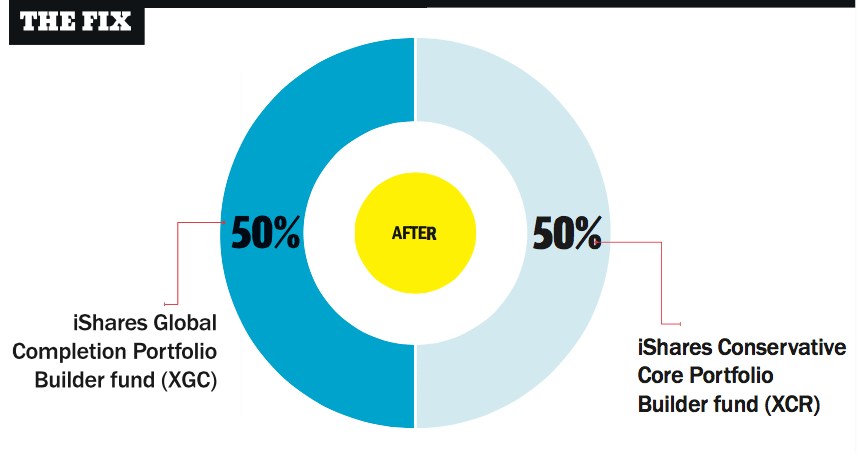

To get the asset allocation and diversification Nelson needs, Clyne recommends that he build his portfolio using two of the four ETFs that make up the iShares Portfolio Builders series of funds: the Conservative Core fund (XCR) and the Global Completion fund (XGC). These funds have low fees—0.6% and 0.72%, respectively—and each includes an entire portfolio of products packed into a single fund, spanning Canadian and international equities, as well as other financial products such as bonds, REITs and commodities. While rebalancing is usually the cornerstone of a well-diversified portfolio strategy, there’s no need to do that with these funds, as they are actively rebalanced from time to time to maintain what iShares considers to be the optimum allocation among these different types of assets. “This bit of active management allows Nelson to remain on the sidelines for years and never have to rebalance the ETFs himself,” says Clyne. “It makes investing very easy and stress-free.”

To get this portfolio, Clyne recommends Nelson split his money 50/50 between them, adding that he could try directing each quarterly RRSP payment to the ETF that fared worse during that period. This way, he can take advantage of the lower purchase price which helps reduce his adjusted cost base for extra tax savings. “It’s a solid strategy for the long haul.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Why and how ETF closures happen, which warning signs to watch for, and what it means if a fund...

Investors seeking cash flow from real assets and inflation resistance should consider these infrastructure ETFs.

Investors may be paying high fees for lower risk-adjusted returns with these concentrated covered-call ETFs, all in the name...

A practical guide to developing-country equity ETFs, covering classification differences, higher volatility, and key tax considerations for Canadian investors.

ETFs

The best all-in-one ETFs in Canada, from XEQT to VBAL. How to choose based on risk, time horizon, and...

ETFs

A guide to the best Canadian fixed-income ETFs in 2026, featuring low-cost aggregate bond funds like VAB, TDB, and...