How to avoid a value trap

Here's a strategy that spots cheap stocks that are on the way up

Advertisement

Here's a strategy that spots cheap stocks that are on the way up

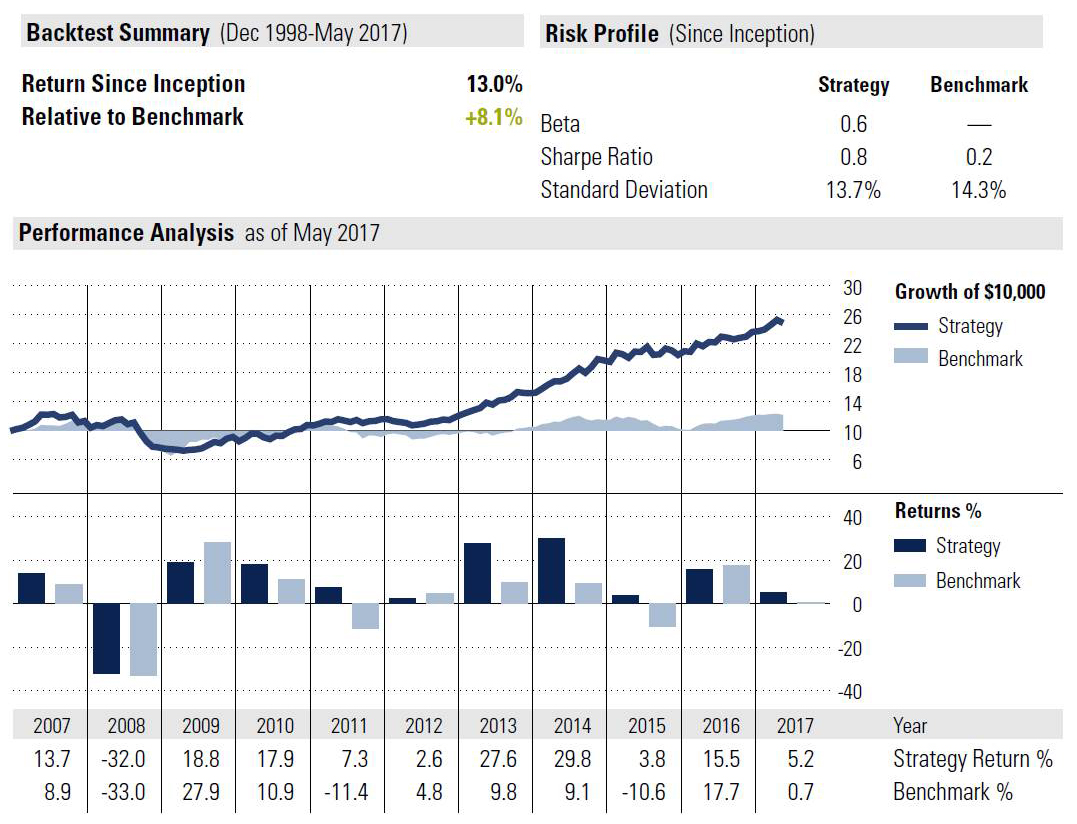

As always, investors are encouraged to conduct their own independent research before purchasing any of the investments listed here:

As always, investors are encouraged to conduct their own independent research before purchasing any of the investments listed here:

| Rank | Company | Forward P/E Relative to Sector Median | P/Book Relative to Sector Median | P/Cashflow Relative to Sector Median | P/Sales Relative to Sector Median | 3M Price Momentum (%) | Quarterly Earnings Momentum (%) | Earnings Surprise (%) | 5Y EPS Growth (%) |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Cdn Tire Corp. Ltd. (CTC.A) | 0.9 | 0.8 | 1.0 | 0.5 | 7.6 | 4.6 | 14.9 | 8.2 |

| 2 | Magna Intl. Inc. (MG) | 0.5 | 0.6 | 0.5 | 0.3 | 1.6 | 5.4 | 7.4 | 30.0 |

| 3 | Manulife Financial Corp (MFC) | 0.9 | 0.7 | 0.3 | 0.4 | 4.2 | 4.5 | 0.0 | 31.6 |

| 4 | Weston Ltd., George (WN) | 1.0 | 0.6 | 0.3 | 0.4 | 4.4 | 2.2 | 2.0 | 12.5 |

| 5 | Loblaw Companies Ltd. (L) | 1.0 | 0.6 | 0.6 | 0.8 | 4.6 | 2.0 | 0.0 | 11.3 |

| 6 | National Bank of Canada (NA) | 0.9 | 1.1 | 1.0 | 1.0 | 4.2 | 3.2 | 0.3 | 6.1 |

| 7 | Metro Inc. (MRU) | 0.9 | 1.0 | 1.0 | 1.0 | 3.4 | 2.0 | 1.8 | 12.3 |

| 8 | Bank of Montreal (BMO) | 1.0 | 0.9 | 1.0 | 1.0 | 3.9 | 2.4 | 0.0 | 6.8 |

| 9 | Fortis Inc. (FTS) | 1.0 | 0.9 | 0.9 | 1.1 | 3.1 | 2.6 | -0.2 | 7.2 |

| 10 | TELUS Corporation (T) | 0.9 | 1.0 | 0.9 | 0.9 | 2.7 | 1.4 | 1.3 | 7.1 |

| 11 | CGI Group Inc., A (GIB.A) | 0.7 | 1.0 | 0.6 | 0.4 | 1.1 | 0.4 | 0.0 | 20.9 |

| 12 | BCE Inc. (BCE) | 1.0 | 1.0 | 1.0 | 1.0 | 1.5 | 0.1 | 0.0 | 3.1 |

| 13 | Emera Inc. (EMA) | 1.0 | 1.1 | 1.1 | 0.9 | 1.8 | -8.4 | 0.0 | 13.1 |

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Crypto is going mainstream in Canada. A new OSC survey finds ownership has more than doubled, while advisor recommendations...

The CRA is cracking down on TFSA overcontributions. Learn how penalties work, how to correct mistakes, and when...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Copper production lifted First Quantum, while Intact faced higher catastrophe claims. Catch up on the latest quarterly results from...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Artificial intelligence is transforming markets, but retirees should approach the AI investing theme with caution and a well-diversified portfolio.