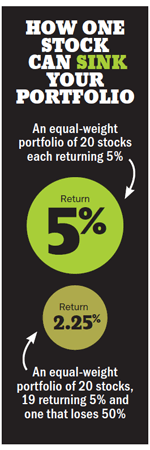

Stocks: The hard sell

Investors love to buy stocks, but selling is much harder. All too often pride, anxiety and neglect keep us hanging onto our losing stocks until it's too late

Advertisement

Investors love to buy stocks, but selling is much harder. All too often pride, anxiety and neglect keep us hanging onto our losing stocks until it's too late

The recent takeover of Nexen by China’s CNOOC is an apt illustration. Its shares soared more than 50% after the offer, to within a dollar of the proposed sale price. Holding out for the merger to close would only have netted you an additional 3.8% while Ottawa mulled over the deal. The risk was what would have happened if the decision went the other way. Had that happened the stock likely would have dropped back to its pre-takeover levels, resulting in a loss of 30%.

Given the time it has taken to close this deal and the political posturing around it, it’s hardly worth the risk of giving up the 50% gain for an extra few percentage points. Unless you were expecting a new offer to come in and drive the price higher, in cases like this it’s probably a good time to sell and move on and let someone else assume the risk.

The recent takeover of Nexen by China’s CNOOC is an apt illustration. Its shares soared more than 50% after the offer, to within a dollar of the proposed sale price. Holding out for the merger to close would only have netted you an additional 3.8% while Ottawa mulled over the deal. The risk was what would have happened if the decision went the other way. Had that happened the stock likely would have dropped back to its pre-takeover levels, resulting in a loss of 30%.

Given the time it has taken to close this deal and the political posturing around it, it’s hardly worth the risk of giving up the 50% gain for an extra few percentage points. Unless you were expecting a new offer to come in and drive the price higher, in cases like this it’s probably a good time to sell and move on and let someone else assume the risk.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Why and how ETF closures happen, which warning signs to watch for, and what it means if a fund...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Bonds are considered safer than stocks, but higher interest rates can still lead to losses. Here's what investors need...

BlackBerry is back, baby, and other standout stories from yet another good quarter for Canadian equities.

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Moving to the U.S. doesn’t automatically mean you should convert your Canadian investments. Here’s why tax rules, currency risk...

Couche-Tard reports higher Q4 profit and revenue, BlackBerry raises full-year outlook after a stronger quarter, and Metro sees earnings...