Best way to invest a large sum of money

The key is to keep it simple

Advertisement

The key is to keep it simple

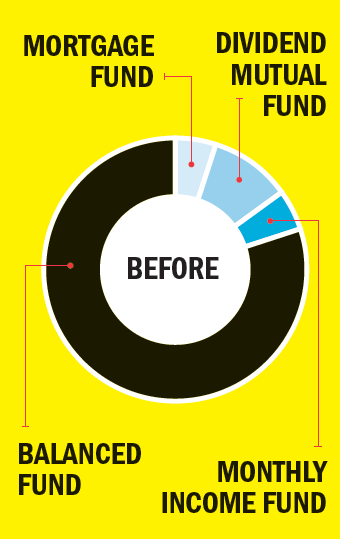

Moyra Thompson, 60, is retired and her $600,000 mortgage-free house is up for sale. “I want to sell before boomers flood the market with homes,” says Moyra, who receives $2,100 a month from two small pensions and will start collecting CPP at age 65. Right now, her $150,000 portfolio is invested in bank mutual funds with an overall management expense ratio (MER) of 1.9%, split evenly between fixed income and equities—but even with an additional $600,000 Moyra is concerned her money won’t last into her 90s. “I’ll need $15,000 net a year from my portfolio. I’m not sure the 50% fixed income and 50% equity split will give me that.”

Certified financial planner Chris Stephenson of Steadyhand Investment Funds in Vancouver says that if Moyra’s goal is to withdraw $15,000 annually from a $750,000 portfolio (an extraction rate of 2%), she’ll have no problems. In fact, this is easily achievable with her current asset mix of 50% stocks and 50% fixed income, and Stephenson sees no reason to change this. “Investors often feel they have to change investment strategy when they get a large sum of money. But if your goals can be met with your present strategy, it makes sense to continue with it.”

Moyra Thompson, 60, is retired and her $600,000 mortgage-free house is up for sale. “I want to sell before boomers flood the market with homes,” says Moyra, who receives $2,100 a month from two small pensions and will start collecting CPP at age 65. Right now, her $150,000 portfolio is invested in bank mutual funds with an overall management expense ratio (MER) of 1.9%, split evenly between fixed income and equities—but even with an additional $600,000 Moyra is concerned her money won’t last into her 90s. “I’ll need $15,000 net a year from my portfolio. I’m not sure the 50% fixed income and 50% equity split will give me that.”

Certified financial planner Chris Stephenson of Steadyhand Investment Funds in Vancouver says that if Moyra’s goal is to withdraw $15,000 annually from a $750,000 portfolio (an extraction rate of 2%), she’ll have no problems. In fact, this is easily achievable with her current asset mix of 50% stocks and 50% fixed income, and Stephenson sees no reason to change this. “Investors often feel they have to change investment strategy when they get a large sum of money. But if your goals can be met with your present strategy, it makes sense to continue with it.”

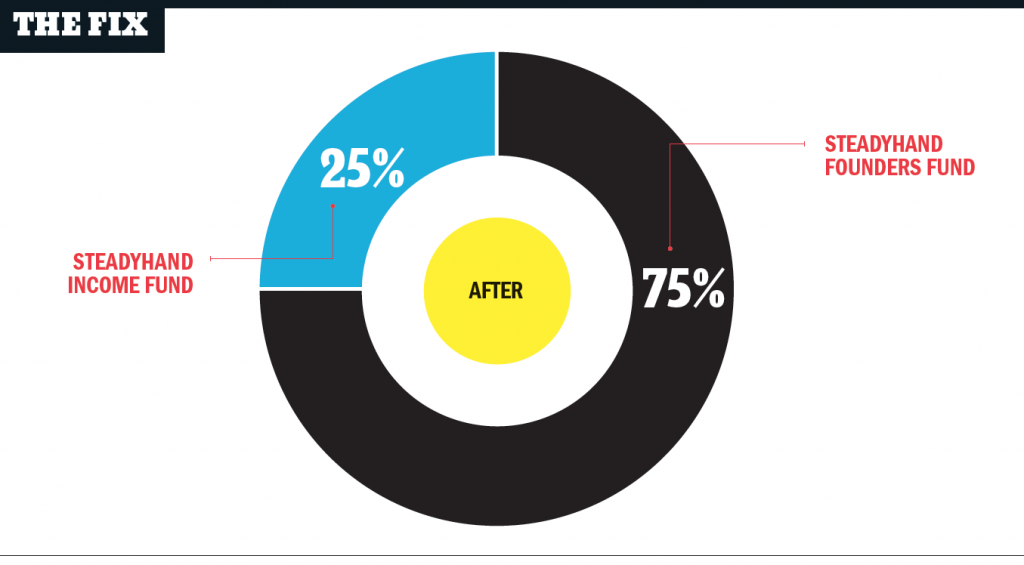

Still, there are a few things Moyra can do to hold onto more of her money, Stephenson adds. Investment costs are important, and Moyra could lower her current portfolio’s 1.9% MER by switching over to no-load, low-fee funds. He recommends a portfolio comprised of Steadyhand’s Founders Fund (75% of holdings) and Income Fund (25%)—which would still give Moyra an asset mix of 50% stocks and 50% fixed income. Her all-in costs? “Assuming a portfolio value of $750,000, Moyra would pay roughly a 0.9% MER—a very affordable amount to pay for a diversified portfolio,” says Stephenson.

Moyra should also set aside two years’ worth of living expenses, or about $30,000, in a savings account. “She should replenish this every 18 months by selling some of her investments in the Founders Fund and Income Fund,” says Stephenson. Finally, Moyra should consider meeting with a fee-for-service planner annually to ensure her financial plan stays on track.

Still, there are a few things Moyra can do to hold onto more of her money, Stephenson adds. Investment costs are important, and Moyra could lower her current portfolio’s 1.9% MER by switching over to no-load, low-fee funds. He recommends a portfolio comprised of Steadyhand’s Founders Fund (75% of holdings) and Income Fund (25%)—which would still give Moyra an asset mix of 50% stocks and 50% fixed income. Her all-in costs? “Assuming a portfolio value of $750,000, Moyra would pay roughly a 0.9% MER—a very affordable amount to pay for a diversified portfolio,” says Stephenson.

Moyra should also set aside two years’ worth of living expenses, or about $30,000, in a savings account. “She should replenish this every 18 months by selling some of her investments in the Founders Fund and Income Fund,” says Stephenson. Finally, Moyra should consider meeting with a fee-for-service planner annually to ensure her financial plan stays on track.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Whether for income or day trading, these ETFs are more complex and potentially risky products than they first appear....

As the cost of living climbs, financial help from family and increased credit use are becoming survival strategies for...

Thinking about selling a property that’s not currently your primary residence? Knowing its value is essential to calculating—and not...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Cogeco’s Canadian wireless launch arrives amid downgraded outlook, falling U.S. revenue, and analyst concerns.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

The co-founder of online prenuptial agreement startup Jointly talks about leaving Big Law, tracking spending as a system, and...