By David Aston on January 17, 2012 Estimated reading time: 10 minutes

Delectable dividends and tax savings

By David Aston on January 17, 2012 Estimated reading time: 10 minutes

The tax man gives Canadian dividends such a delicious treatment, you can pay negative taxes. That means no tax on your dividends, and less tax on your other income. Talk about having your ice cream and eating it too.

This article is 1 year old. Some details may be outdated.

Advertisement

Like most dividend-loving investors, Larry Clark knows that Canadian dividend-paying stocks give you a hefty tax break when you hold them outside of your RRSP. But the Mississauga, Ont., investor (whose name we’ve changed) finds the dividend tax calculations so numbingly complicated he has no idea how much money he actually saves.

Advertisement

Advertisement

“I kind of understand how the dividend tax thing works, but I don’t really know the details,” admits Clark, who is 62 and semi-retired. “I just know it’s better than other types of income.”

Clark isn’t alone in his confusion. Of all the mysteries on your tax return, few are as daunting as the treatment of Canadian dividends. We know that dividend income gets preferential tax treatment, but we don’t know by how much, or why.

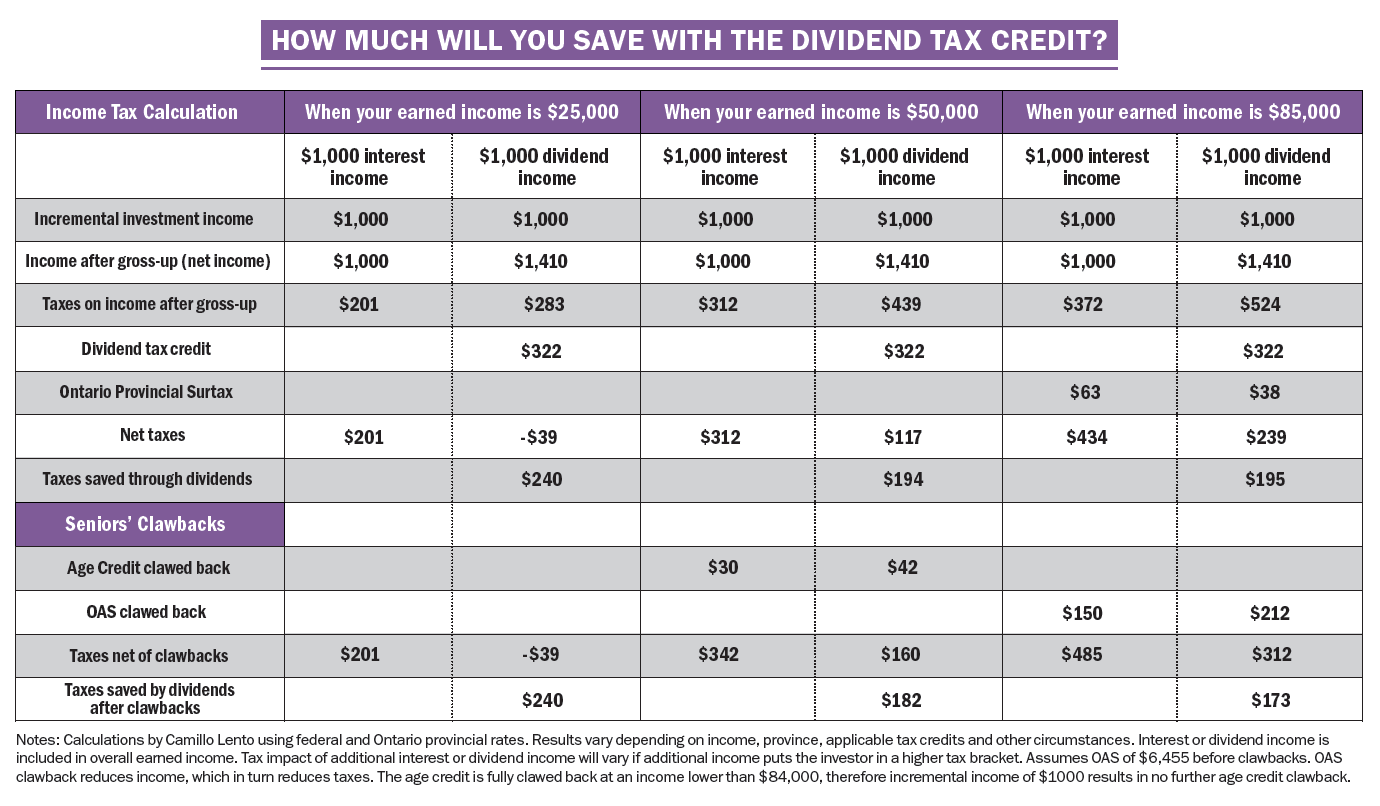

To help you really understand how dividend income saves you money at tax time, we’ve enlisted the help of a couple of tax experts. We asked Camillo Lento, a chartered accountant and lecturer at Lakehead University in Thunder Bay, Ont., to calculate how much tax an investor would pay at three different income levels if he earned $1,000 in Canadian dividend income, compared with the same amount in interest income. We’ve compiled the results in the accompanying table, “How much will you save with the dividend tax credit?” (We crunched the numbers for Ontario specifically, as the benefit in that province falls in middle of the pack.) We also got help from Ross McShane, director of financial planning at McLarty and Co. Wealth Management in Ottawa.

Not surprisingly, the results show that investing in Canadian dividend-payers will save you a bundle. But just how sweet the deal is depends on your income. As with many features of our tax system, the benefits are greatest at moderate income levels, and not as attractive as your income rises.

In what follows, we’ll do our best to explain the calculations and show you how you can get the largest tax benefit possible. Get out your calculators, and we’ll begin. Also, read about how to handle your U.S. dividend stocks.

Click image to enlarge

The sweet taste of taxes saved

If you earn $25,000 a year, the tax benefit you’ll get from Canadian dividend income is enough to make an accountant drool. You not only pay no tax at all on your $1,000 in dividend income, but get this: you actually reduce your taxes on other income. Although the reduction in other taxes is only about $40, that’s still a rare and wonderful thing, what accountants call a “negative marginal tax rate.” All told, after earning $1,000 in dividend income you’re a full $240 ahead of where you’d be after earning the same amount in interest income. That’s about as sweet as it gets.

Article Continues Below Advertisement

At higher income levels, the tax savings on $1,000 in dividends is still very good, but not quite as delectable. When we ran the numbers for people earning a total income of $50,000 and those earning an income of $85,000 for our table, we found that you come out ahead by almost $200 when you earn $1,000 in dividends compared to $1,000 in interest income (assuming that you’re under 65). That’s not as exciting as getting tax money back outright, but your inner accountant will still be pleased.

Unfortunately, there’s a complication if you’re 65 or older and subject to the dreaded Old Age Security (OAS) clawback, which applies to seniors with incomes of $67,700 and above. That’s because dividend income counts for more than regular income in calculating the OAS clawback amount. As a result, a senior earning $85,000 would save only $173 in taxes when he or she earns $1,000 in Canadian dividends, compared to the same amount of interest income. The deal is still sweet for affluent seniors, but it will leave you with a sour aftertaste from the clawback. We’ll come back to this later.

A method behind the madness

Now we’ll reveal the secrets of the dividend tax calculation. It turns out the math is so convoluted for a reason.

The best way to understand how taxes on Canadian dividends are calculated is to take a quick three-step tour. First you take your dividend income and multiply it by 1.41, which is what’s known as the dividend “gross-up.” That means $1,000 in dividends becomes $1,410 in income. (The 1.41 figure is for the 2011 tax year and will change in 2012. The good news is that you don’t actually have to do this on your tax return: the government makes financial institutions gross-up dividends before sending out your T3 and T5 slips.)

Second, you take the grossed-up dividend income and apply your marginal tax rate to figure out your taxes so far. If you live in Ontario and earn $50,000, your marginal tax rate is 31.2%. So that works out to $439 in taxes payable on $1,410 in income.

At this point you’re probably not having much fun, because it feels like you’re set up to pay taxes on the inflated amount. Fortunately, there’s a third step that knocks those nasty taxes back down: you get to apply the dividend tax credit. This is another figure you get from your T3 and T5 slips, and it comes to 22.8% of the grossed-up dividend amount. In this case, that would mean a credit of $322 on your grossed-up $1,410 in income. Now you subtract that credit from the taxes payable, in this case, $439. That leaves you with a final tax bill of just $117. Since the benefit of the tax credit is larger than the impact of the gross-up, you end up ahead.

But why does the tax man make you jump through all these hoops? Why not simply charge a lower rate on dividends from the get-go and make it simpler for everybody?

Advertisement

Advertisement

The reason is that tax authorities have their eye on the big picture. “It’s all about tax integration,” says McShane, the financial planner. Think of it this way: the money you receive as dividends starts off as a company’s earnings, and the company pays corporate taxes on those earnings. After paying those taxes, the company takes a portion of the money that is left and passes it directly to you as a dividend, and you pay tax on it again.

The government recognizes that it’s unfair to tax the same income twice. So they give you a break on dividend taxes to offset the taxes the corporation already paid. As a result, you should pay roughly the same tax as if the income had come straight to you in the first place, without passing through corporate hands.

Now that you know what the tax authorities are trying to do, have another look at the three-step calculation. Step one, where you apply the gross-up, brings your income back to the starting point, as if the corporation had never touched it. Step two applies your marginal tax rate to this income, again as if it had never gone through corporate hands. Then step three applies the dividend tax credit to give you back the taxes the corporation actually paid. In general, if your marginal tax rate is higher than the corporate tax rate, you’ll still pay some tax: roughly the difference between the two rates. If your marginal tax rate is lower than the corporate tax rate, you’ll typically get some money back. However, you won’t ever get a cheque from the Canada Revenue Agency: the dividend tax credit is “non-refundable,” which means it can only be used to offset tax otherwise payable on other income.

Before you count on the dividend tax break too much, you should realize that it has been gradually shrinking. That’s because the federal government has been phasing in reduced corporate income tax rates from 2007 to 2012. Since the dividend taxes you pay are based on the difference between your personal tax rate and the corporate tax rate, this means your share of the taxes paid is getting larger. The consolation prize, as Lento points out, is that (in theory) the reduction in corporate taxes should allow companies to increase their dividends.

The dreaded clawback

For affluent seniors, the real unsavoury morsel is the OAS clawback. Remember our first step in the calculation, which inflates a dollar of dividends to $1.41? Well, it’s that grossed-up income that’s used when determining the clawback. Thanks to this seemingly twisted math, dividends can appear less desirable than interest income in this situation.

As you can see in our table, for the senior with an income of $85,000, an extra $1,000 in interest income reduces OAS by $150, but the same amount of additional dividend income reduces OAS by $212.

The tax authorities use a similar approach to calculate other clawbacks on income-related seniors’ benefits, including the Age Credit, which is shown in the examples laid out in our table. The same principle also works against lower-income seniors who are potentially eligible for the Guaranteed Income Supplement (GIS). The GIS is reduced in proportion to your other income, and it too uses grossed-up dividends when making the calculation.

Advertisement

Advertisement

Most seniors feel a bit cheated when they learn that dividends affect the clawbacks in this way. But remember, when it applies to OAS, you’re still ahead of the game. “Even though they’re giving back some of the OAS, the retiree is still further ahead overall with a dollar of dividends rather than a dollar of interest,” says McShane. So while you may have to scoop out that fly in your ice cream and set it aside, your dividends are still likely to provide a tasty meal.

Should you treat U.S. stocks differently?

By this point you no doubt realize that the tax break on dividends only applies to Canadian stocks, not U.S. stocks. As a result, you need to treat the two differently when fitting them into your portfolio.

The standard advice is to put Canadian stocks in non-registered accounts, and put fixed income investments, such as bonds and GIC rate, inside RRSPs and TFSAs. Tax rates are lower on the Canadian dividend income and capital gains you get from stocks than they are on the interest income you get from bonds and GICs, so keep your stocks outside your RRSP where taxes matter, and then hold your bonds and GICs inside.

U.S. equities are more complicated. Dividends from U.S. stocks are taxed in Canada at regular rates, just like interest income. But capital gains on U.S. stocks—which you trigger when you sell a stock at a profit—are taxed favorably just like capital gains on Canadian stocks. So it makes sense to hold U.S. stocks that pay little or no dividends inside your non-registered accounts alongside Canadian stocks. On the other hand, U.S. stocks that pay handsome dividends probably fit better in your RRSP.

There is an added U.S. tax wrinkle here: the Internal Revenue Service levies a 15% withholding tax on dividends on U.S. stocks held by foreign investors (these are deducted automatically). If a stock pays a 3% dividend, then, the withholding tax would reduce it to 2.55%.

Fortunately, if you hold U.S. stocks in non-registered accounts, you get a credit for the amount withheld that you can apply against Canadian income taxes, so in most cases that leaves you square—providing your Canadian tax rate is at least 15%.

In the case of RRSPs and other retirement accounts, Canada has a tax treaty with the U.S. that exempts you from the withholding tax. But if you hold U.S. stocks in a TFSA or an RESP, you’re dinged the 15% levy and you can’t get it back. As a result, you’re best off holding U.S. stocks that pay hefty dividends inside your RRSPs, and keeping them outside of your TFSAs and RESPs. Who knew?

Advertisement

Advertisement

Keep in mind that dividend withholding tax amounts and treatments vary among other countries, so don’t count on the advice for U.S. stocks applying to stocks from overseas.

So if I have a mixture of high dividend stock and riskier no dividend stock, I should put the riskier stock in a my tax free account and put the high dividend stock in the portfolio outside of the tax free account. After all, I get no benefit of dividend tax credit in my tax free account. Why do I not see my conclusion mentioned anywhere?

Very informative article! Much appreciated!!

“Since the benefit of the tax credit is larger than the impact of the gross-up, you end up ahead.” per the article.

Tax on Gross Up…439.00

Tax Credit on GU..322.00

Extra tax paid…………………..117.00

Unless I am missing something, The benefit of the tax credit is less than the impact of the gross-up and you are not ahead.

So if I have a mixture of high dividend stock and riskier no dividend stock, I should put the riskier stock in a my tax free account and put the high dividend stock in the portfolio outside of the tax free account. After all, I get no benefit of dividend tax credit in my tax free account. Why do I not see my conclusion mentioned anywhere?